On March 25, 2015, the Securities and Exchange Commission voted unanimously to adopt final rules to implement the rulemaking mandate of Title IV of the JOBS Act by adopting amendments to Regulation A. In December 2013, the SEC had released a proposed rule that essentially retained the current framework of Regulation A and expanded it for larger exempt offerings. The proposed rules were generally well-received. The final rules addresses a number of issues raised by commenters, while retaining substantially the same approach outlined in the proposed rule.

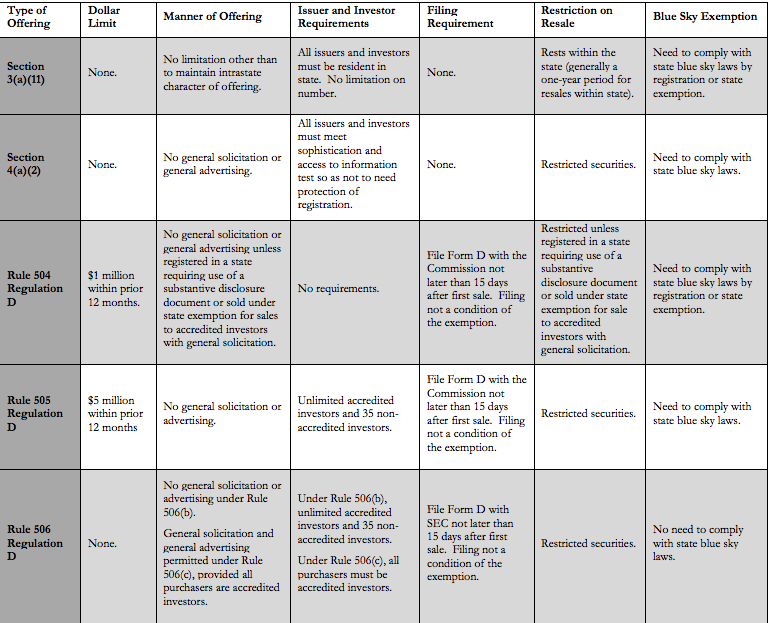

Briefly, by way of background, existing Regulation A provides an exemption from the registration requirements of Section 5 for certain smaller securities offerings by private (non-SEC-reporting) companies. The securities sold in a Regulation A offering are not considered “restricted securities” and are freely transferable. However, the low dollar threshold, the disclosure requirements, and the requirement to comply with state blue sky laws had limited the utility of Regulation A. Other exemptions, such as Rule 506 under Regulation D, which have no dollar threshold, became more popular. Prior to the JOBS Act, a number of market participants advocated amending Regulation A to raise the dollar threshold and legislation to amend and to modernize Regulation A was proposed and considered prior to the emergence of the JOBS Act. In large measure, Title IV of the JOBS Act incorporated many of the provisions that had been addressed in those standalone bills. Section 401 of the JOBS Act amended Section 3(b) of the Securities Act by renumbering it as Section 3(b)(1) and adopting new sections (b)(2) through (b)(5). Pursuant to the JOBS Act additions to Section 3(b), the SEC is authorized to promulgate rules or regulations creating an exemption that is substantially similar to the existing Regulation A for offerings of up to $50 million.

The New Regulation A

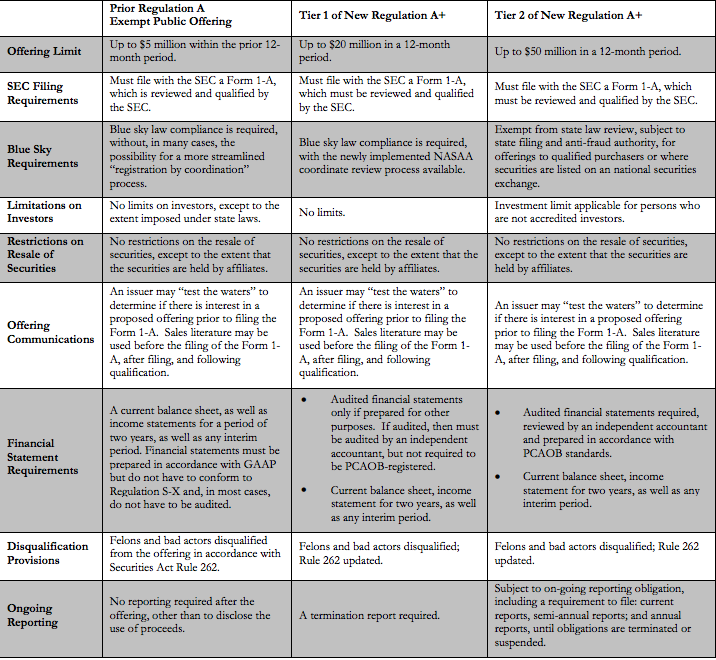

As discussed in more detail below, the final rules provide an exemption for U.S. and Canadian companies that are not required to file reports under the Exchange Act to raise up to $50 million in a 12-month period. The final rules create two tiers: Tier 1 for smaller offerings raising up to $20 million in any 12-month period, and Tier 2 for offerings raising up to $50 million. The new rules also make the exemption available, subject to limitations on the amount, for the sale of securities by existing stockholders. The new rules modernize the existing framework under Regulation A by, among other things, requiring that disclosure documents be filed on EDGAR, allowing an issuer to make a confidential submission with the SEC, permitting certain test-the-waters communications, and disqualifying bad actors. The final rules impose different disclosure requirements for Tier 1 and Tier 2 offerings, with more disclosure required for Tier 2 offerings, including audited financial statements. Tier 1 offerings will be subject to both SEC and state blue sky pre-sale review. Tier 2 offerings will be subject to SEC, but not state blue sky, pre-sale review; however, investors in a Tier 2 offering will be subject to investment limits (except when securities are sold to accredited investors or are listed on a national securities exchange) and Tier 2 issuers will be required to comply with periodic filing requirements, which include a requirement to file current reports upon the occurrence of certain events, semi-annual reports and annual reports. The final rules provide a means for an issuer in a Tier 2 offering to concurrently list a class of securities on a national exchange through a short-form Form 8-A, without requiring the filing of a separate registration statement on Form 10.

Eligible Issuers

The new Regulation A exemption, both Tier 1 and Tier 2, will be available to issuers organized in and having their principal place of business in the United States or Canada. The following issuers will be “ineligible” to offer or sell securities under Regulation A:

- an issuer that is an SEC-reporting company;

- a blank check company;

- any investment company registered or required to be registered under the Investment Company Act of 1940 (this includes business development companies); and

- any entity issuing fractional undivided interests in oil or gas rights, or similar interests in other mineral rights.

The exemption also is not available to: issuers that have not filed with the SEC the ongoing reports required by Regulation A during the two years immediately preceding the filing of a new offering statement, issuers that have had their registration revoked pursuant to an Exchange Act Section 12(j) order that was entered into within five years before the filing of the offering statement and certain bad actors.

Eligible Securities

The securities that may be offered under Regulation A are limited to equity securities, including warrants, debt securities and debt securities convertible into or exchangeable into equity interests, including any guarantees of such securities. The final rule excludes asset-backed securities.

Offering Limitations

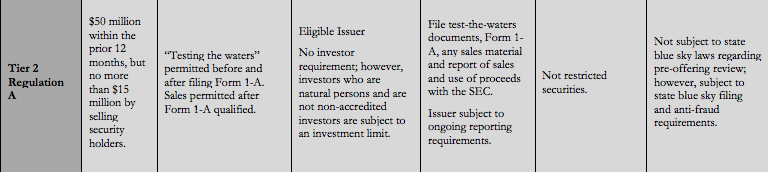

As noted above, an issuer can choose a Tier 1 or a Tier 2 offering. Under Tier 1, an issuer may offer and sell up to $20 million in a 12-month period, of which up to $6 million may constitute secondary sales (except as noted below). Under Tier 2, an issuer may offer and sell up to $50 million in a 12-month period, of which up to $15 million may constitute secondary sales (except as noted below). The final rules set out an approach for calculating the offering limit in the case of convertible or exchangeable securities.

In the issuer’s initial Regulation A offering and any Regulation A-exempt offering in the 12 months following that offering price of the particular offering, the selling securityholder component cannot exceed 30% of the aggregate offering. In addition, the final rules distinguish between sales by affiliates and sales by non-affiliates. Following the expiration of the first year following an issuer’s initial qualification of a Regulation A offering statement, the limit on secondary sales falls away for non-affiliates only. Notably, the final rule eliminates the current prohibition on resales by affiliates in reliance on the exemption unless the issuer had net income from continuing operations in at least one of the last two years.

Investment Limitation

Prior to the amendments, Regulation A did not contain a limit on the amount of securities that may be purchased by an investor. However, to address potential investor protection concerns, the final rules impose an investment limit for Tier 2 offerings. The investment limit will not apply to accredited investors and will not apply if the securities are to be listed on a national securities exchange at the consummation of the offering; otherwise a non-accredited natural person is subject to an investment limit and must limit purchases to no more than 10% of the greater of the investor’s annual income and net worth, determined as provided in Rule 501 of Regulation D (for non-accredited, non-natural persons, the 10% limit is based on annual revenues and net assets).

Investors must be notified of the investment limitations, and may rely on a representation of compliance with the investment limitation from the investor, unless the issuer knew at the time of sale that any such representation is untrue.

Integration of Offerings

A Regulation A offering will not be integrated with:

- prior offers or sales of securities; or

- subsequent offers or sales of securities that are:

- registered under the Securities Act, except as provided in Rule 255(e);

- made in reliance on Rule 701;

- made pursuant to an employee benefit plan;

- made in reliance on Regulation S;

- made pursuant to Section 4(a)(6) of the Securities Act [crowdfunded offerings]; or

- made more than six months after the completion of the Regulation A offering.

As a result, one could envision an issuer making a private offering under Section 4(a)(2) or Regulation D prior to commencing a Regulation A offering without risking integration of the private offering with the Regulation A offering. An offering made under Regulation A should not be integrated with another exempt offering, provided that each exempt offering complies with the requirements for the exemption that is being relied upon for that particular offering. The final rule also addresses abandoned offerings in much the same way that these are handled by Rule 155, with a 30-day cooling off period.

The SEC reaffirmed guidance that was included in the proposing release which is consistent with the guidance regarding integration provided in Release 33-8828.

Exchange Act Threshold

The proposed rule did not exempt securities sold pursuant to Regulation A from the calculation of “holder of record” for purposes of the Section 12(g) Exchange Act threshold. The final rule, however, provides a limited exemption for securities issued in a Tier 2 offering from the Section 12(g) “holder of record” threshold where the issuer is subject to, and current in its, Regulation A periodic reporting obligations. In order to benefit from this conditional exemption, an issuer must: retain the services of a transfer agent and meet requirements similar to those in the “smaller reporting company” definition (public float of less than $75 million or, in the absence of a float, revenues of less than $50 million, in the most recently completed fiscal year). An issuer that exceeds the Section 12(g) threshold will have a two-year transition period.

Filing and Delivery Requirements

Regulation A offering statements must be filed on EDGAR. The Form 1-A has been amended to consist of three parts: Part I, which will be an XML-based fillable form with basic issuer information; Part II, which will be a text file that will contain the disclosure document and financial statements; and Part III, which will be a text file that will contain exhibits and related materials. Periodic reports and any other documents required to be submitted to the SEC in connection with a Regulation A offering must be filed on EDGAR.

As proposed, the final rules adopts an access equals delivery model for Regulation A final offering circulars. In the case where a preliminary offering circular is used to offer securities to potential investors and the issuer is not already subject to the Tier 2 periodic reporting requirements, an issuer and participating broker-dealer will be required to deliver the preliminary offering circular to prospective purchasers at least 48 hours in advance of sales.

Non-Public Review

An issuer may submit an offering statement for non-public review by the SEC. As with EGCs, should an issuer opt for confidential review, the offering statement must be filed publicly not less than 21 calendar days before qualification of the offering statement. The timing, in the case of a Regulation A offering, is not tied to an issuer’s road show, but rather to the qualification of the offering statement. The SEC noted specifically that the 21-day public filing period will provide state securities regulators an opportunity to assure filing of offering materials at the state level in advance of an offering under Regulation A.

Form 1-A

An issuer that seeks to rely on Regulation A must file and qualify an offering statement. The offering statement is intended to be a disclosure document that provides potential investors with information that will form the basis for their investment decision. A notice of “qualification” is similar to a notice of effectiveness in an SEC-registered offering.

Part I

As noted above, Part I requires certain basic information regarding the issuer, its eligibility, the offering details, the jurisdictions where the securities will be offered, and sales of unregistered securities.

Part II

Part II contains the narrative portion of the Offering Circular and requires disclosures of basic information about the issuer; material risks; use of proceeds; an overview of the issuer’s business; an MD&A type discussion; disclosures about executive officers and directors and compensation; beneficial ownership information; related party transactions; and a description of the offered securities. This is similar to Part I of Form S-1, and an issuer can choose to comply with Part I of Form S-1 in connection with its Offering Circular. The disclosure requirements will be scaled.

Tier 1 and Tier 2 issuers must file balance sheets and other required financial statements as of the two most recently completed fiscal year ends (or for such shorter time as they have been in existence). U.S. issuers are required to prepare financial statements in accordance with U.S. GAAP. Canadian issuers may use U.S. GAAP or IFRS as adopted by the IASB. As with EGCs, an issuer may elect to delay implementation of new accounting standards to the extent such standard permit delayed implementation by non-public business entities. The election is a one-time election and must be disclosed.

The financial statements for an issuer in a Tier 1 offering are not required to be disclosed; however, if a Tier 1 issuer already obtained an audit of its financial statement for other purposes and such audit was performed in accordance with U.S. GAAS or the PCAOB standards and the auditors meet the independence standards, then the audited financial statements must be filed.

The financial statements for an issuer in a Tier 2 offering are required to be audited. The audit firm must satisfy the independence standard but need not be PCAOB-registered. The financial statements may be audited in accordance with either U.S. GAAS or PCAOB standards. An issuer in a Tier 2 offering that seeks to have a class of securities listed on a national securities exchange concurrent with the Regulation A offering must include financial statements prepared in accordance with PCAOB standards by a PCAOB-registered firm.

The final rule addresses technical matters, such as the age of the financial statements. Issuers in Tier II offerings are not required to provide financial statements in an interactive data format using XBRL.

Part III

The exhibit requirements in Part III of Form 1-A are maintained, however, the final rule allows for incorporation by reference of exhibits that were previously filed on EDGAR.

Continuous Offerings

The final rule would continue to permit continuous or delayed offerings in certain instances, such as for offerings offered or sold on behalf of selling security holders, securities offered under employee benefit plans; securities pledged as collateral; securities issued upon conversion of other outstanding securities or upon the exercise of options, warrants, or rights, etc.; or securities that are part of an offering which commences within two calendar days after the qualification date, will be offered on an continuous basis, may continue to be offered for a period in excess of 30 days from the date of initial qualification, and will be offered in an amount that, at the time the offering statement is qualified, is reasonably expected to be offered and sold within a period of two years from the initial qualification date. The offerings permitted under Regulation A would be limited in the same manner as under Rule 415; as such, delayed offerings would not be permitted under Regulation A.

Offering Communications

An issuer engaged in a Regulation A offering has substantial flexibility regarding offering communications. An issuer must file solicitation materials with the SEC. Solicitation materials used after an offering circular is filed must be accompanied by the offering circular or include a link to the offering circular. Solicitation materials will be subject to certain legends.

The SEC also confirmed that regularly released factual business communications will not constitute solicitation materials, consistent with the guidance of Rule 169.

Ongoing Reporting Requirements

Currently, Regulation A does not require that issuers file ongoing reports with the SEC, other than a Form 2-A to report sales or termination of sales made under Regulation A. While the final rules rescind Form 2-A, they impose new on-going reporting obligations for certain offerings.

Tier 1 issuers will be required to provide certain information about their Regulation A offerings on a new form, Form 1-Z.

Issuers in Tier 2 offerings will be subject to an ongoing reporting regime. Similar to the ongoing reporting regime that the SEC proposed in connection with issuers that conduct crowdfunded offerings, Tier 2 issuers would be required to file:

- annual reports on Form 1-K;

- semi-annual reports on Form 1-SA;

- current reports on Form 1-U;

- special financial reports on Form 1-K and Form 1-SA; and

- exit reports on Form 1-Z.

The Form 1-K would require disclosures relating to the issuer’s business and operations for the preceding three fiscal years (or since inception if in existence for less than three years); related party transactions; beneficial ownership; executive officers and directors; executive compensation; MD&A; and two years of audited financial statements. The form is required to be filed within 120 calendar days of the issuer’s fiscal year-end.

The semi-annual report would be similar to a Form 10-Q, although it would be subject to scaled disclosure requirements. The semi-annual report is required to be filed within 90 days after the end of the first six months of the issuer’s fiscal year end, commencing immediately following the most recent fiscal year for which full financial statements were included in the offering circular or, if the offering circular included six-month interim financial statements for the most recent full fiscal year, then for the first six months of the following fiscal year.

A current report on Form 1-U will be required to announce fundamental changes in the issuer’s business; entry into bankruptcy or receivership proceedings; material modifications to the rights of securityholders; changes in accountants; non-reliance on audited financial statements; changes in control; changes in key executive officers; and sales of 10 percent or more of outstanding equity securities in exempt offerings. The form must be filed within four business days of the triggering event.

An exit report on Form 1-Z would be required to be filed within 30 days after the termination or completion of a Regulation A-exempt offering.

Rule 15c2-11, Rule 144 and Rule 144A

A Tier 2 issuer’s periodic reports will satisfy Exchange Act Rule 15c2-11 broker-dealer requirements relating to the obligation to review information about an issuer in connection with publishing quotations on any facility other than a national securities exchange. However, contrary to commenters’ requests, the final rule does not establish that these reports would constitute “current information” for Rule 144 and Rule 144A purposes. A Tier 2 issuer that voluntarily submits quarterly information in a form consistent with that required for semi-annual information would be able to satisfy the “reasonably current information” and “adequate current public information” requirements.

Tier 2 Offering with Concurrent Exchange Act Registration

The final rules facilitate the ability of a Tier 2 issuer to voluntarily register a class of Regulation A securities under the Exchange Act. In the absence of the relief provided in the final rules, an issuer that completed a Regulation A offering and sought to list a class of securities on a national securities exchange would have had to incur the costs and the timing delays associated with preparing and filing a separate registration statement on Form 10. The final rule permits a Tier 2 issuer that has provided disclosure in Part II of Form 1-A that follows Part 1 of Form S-1 (or for REITs, Form S-11) to file a Form 8-A to list its securities on a national securities exchange. Of course, thereafter, the issuer would be subject to Exchange Act reporting requirements. An issuer that enters the Exchange Act reporting regime in this manner will be an EGC.

Termination or Suspension of Tier 2 Disclosure Obligations

Tier 2 issuers would be permitted to terminate or suspend their ongoing reporting obligations on a basis similar to the provisions for suspension or termination of reporting requirements for Exchange Act filers. A Tier 2 issuer that has filed all required ongoing reports for the shorter of: (1) the period since the issuer became subject to such reporting obligations, or (2) its most recent three fiscal years and the portion of the current year preceding the date of filing Form 1-Z (termination or exit form) will be permitted to suspend its reporting obligations at any time after completing reporting for the fiscal year in which the offering statement was qualified. This suspension will be permitted if the securities of each class to which the offering statement relates are held of record by fewer than 300 persons and offers or sales made in reliance on a qualified offering statement are not ongoing. Further, the Regulation A on-going reporting requirements would be automatically suspended if an issuer registers a class of securities under Section 12 of the Exchange Act.

Bad Actor Disqualification Provisions

The final rule includes bad actor disqualification provisions that are largely consistent with those included in Rule 506(d).

State Securities Law Requirements

As discussed above, one of the most significant concerns regarding the use of the Regulation A exemption has been the requirement to comply with state securities laws. At the time the new rules were proposed, there was no coordinated review process by the states for Regulation A offerings. Although NASAA has now introduced a coordinated review process for Regulation A offerings since the new rules were proposed, the SEC noted that the coordinated review process is relatively new and it remains largely untested.

The final rules provide that Tier 1 offerings will remain subject to state securities law requirements. Consistent with the proposed rules, Tier 2 offerings will not be subject to state review if the securities are sold to “qualified purchasers” or, as provided by statute in the JOBS Act, listed on a national securities exchange. The final rule defines the term “qualified purchaser” in a Regulation A offering to include: all offerees and purchasers in a Tier 2 offering. States will, of course, continue to have authority to require filing of offering materials and enforce anti-fraud provisions in connection with a Tier 2 offering.

Securities Act Liability

Sellers of Regulation A securities would have Section 12(a)(2) liability in respect of offers or sales made by means of an offering circular or oral communications that include a material misleading statement or omission. While an exempt offering pursuant to Regulation A is excluded from the operation of Section 11 of the Securities Act, those offerings are subject to the antifraud provisions under the federal securities laws.

Character of the Securities Sold in a Regulation A Offering

The securities sold in a Regulation A offering are not considered “restricted securities” under Securities Act Rule 144. As a result, sales of the securities by persons who are not affiliates of the issuer would not be subject to any transfer restrictions under Rule 144. Affiliates, of course, would continue to be subject to the limitations of Rule 144, other than the holding period requirement. This is important to an issuer that would like an active trading market to develop for its securities following completion of a Regulation A offering. However, the issuer’s securities may not be listed or quoted on a securities exchange without registration under Section 12 of the Exchange Act, and, as a result, there may not be a liquid market for the securities.

Effective Date

The final rules will be effective 60 days following publication in the Federal Register.

FINRA Review

For any public offering of securities, FINRA Rule 5110 prohibits FINRA members and their associated persons from participating in any manner unless they comply with the filing requirements of the rule[1]. Rule 5110 also contains rules regarding underwriting compensation. Rule 5110(b) requires that certain documents and information be filed with and reviewed by FINRA, and these filing and review requirements apply to securities offered under Regulation A.[2]

Additional Information

We will be supplementing this alert with additional materials, as well as offering various client briefings.

Summary Charts

Below we provide two charts. The first chart summarizes the provisions of current Regulation A, the final rules governing Tier 1 Offerings under the final rule and the final rules governing Tier 2 Offerings. The second chart provides a summary comparison of various securities exemptions.

Tier 1 Offerings

Tier 2 Offerings

ENDNOTES

[1] See FINRA Rule 5110.

[2] See NASD Notice to Members 92-28 (May 1992); see also NASD Notice to Members 86-27 (Apr. 1986).

The full and original memorandum was published by Morrison & Foerster on March 26, 2015 and is available here.