Companies tell us they buy back stock because it is undervalued. The data, however, tells a different story.

Buybacks peaked in 2007 at $589 billion—the best time to sell. And then fell to $138 billion in 2009—the best time to buy.

More than 460 of the 500 companies that make up the S&P index bought back stock over the past decade. It is hard to believe that public companies are systemically undervalued. Much less 92% of the S&P 500.

If companies aren’t undervalued, why do they buy back stock? Taxes.

Buybacks and dividends accomplish the same goal. Both distribute cash to shareholders. The difference lies in their tax treatment. Dividends face the dividend tax. Buybacks do not.

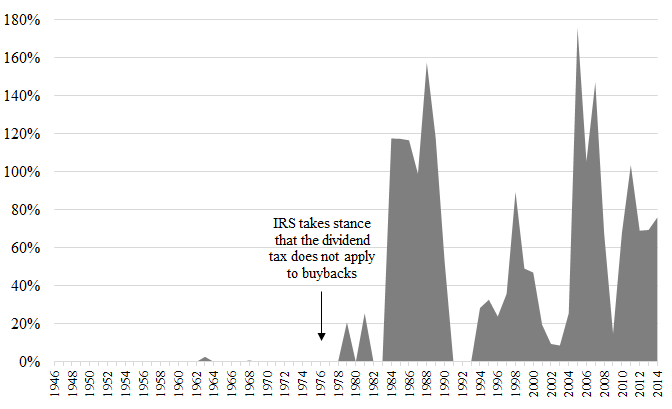

This divergence in tax treatment stems from an IRS stance taken in 1976. Buybacks were virtually nonexistent before then. Companies have since substituted buybacks for dividends to avoid tax. Federal Reserve data, shown below, charts this evolution.

Stock Buybacks as a % of Dividends

This IRS stance has been taken for granted by both scholars and the tax bar. In a recent article, I argue that the IRS has misinterpreted the Tax Code. Buybacks should actually be taxed as dividends.

Sadly, the IRS’s mistaken stance incentivizes companies to gamble their earnings in exchange for a tax break. Dividends and buybacks are close, but not perfect, substitutes. Dividends are paid in cash. Buybacks, on the other hand, offer shareholders a choice—cash or company stock. The cash is taxable. The company stock is not, as long as it is held.

Imagine yourself as a RadioShack customer. You can choose to receive 100% money back as a store credit or only 85% money back as a cash refund, since RadioShack deducts a 15% processing fee. Store credit requires you to shop at RadioShack again. A cash refund can be spent at any store.

RadioShack management faced a similar dilemma in deciding whether to distribute its earnings to shareholders as a buyback or a dividend. A buyback offers shareholders 100% money back. A buyback, however, requires that shareholders reinvest in RadioShack stock. A cash dividend gives shareholders the freedom to invest in any company, but results in a dividend tax.

Management generally opted for store credit. From 1995 to 2011, RadioShack bought back $4.9 billion of its own stock. Yet the company generated only $3.9 billion in earnings over that period. RadioShack spent all its earnings on buybacks and then borrowed another $1 billion from future earnings to buy back even more stock.

On February 5, 2015, RadioShack filed for Chapter 11 bankruptcy protection. Long-term shareholders were wiped out, losing two decades of earnings.

At least they avoided the dividend tax.

The preceding post comes to us from Wanling Su, Visiting Fellow at Yale Law School. The post is based on her recent article, “How the IRS Wrongly Allows Stock Buybacks to Evade the Dividend Tax,” which is available here.