For most of the 20th Century, Eastman Kodak Company (often referred to simply as Kodak) was one of the most recognizable brands in the world. Founded in 1888, Kodak dominated the film and camera markets — in 1976, Kodak had 90% of the film market and 85% of the camera market in the United States.[1] The phrase “a Kodak moment” — describing an event in one’s life that needed to be captured on film for posterity — became a common part of the American lexicon.

However, by the mid-2000s, Kodak was reeling. Although it had built a significant market share in digital cameras, its photo film business had evaporated overnight. By the time digital cameras were largely replaced by cameras embedded in smartphones, Kodak’s share price had fallen by nearly 90%, and in 2012, the company filed for bankruptcy.

There is widespread consensus that blockchain is the technology with the most disruptive potential since the Internet itself, with broad-ranging applications that could transform businesses across the spectrum. Companies who ignore the opportunities — and threats — created by this technology may be doomed to live through their own “Kodak moment.”

The World Economic Forum estimated that 10% of global gross domestic product would be stored on blockchain technology by 2027.[2] Goldman Sachs stated: “From Silicon Valley to Wall Street, technologists and investors alike are buzzing about the potential for the Blockchain to revolutionize . . . well everything.”[3] Investor and Web browser pioneer Marc Andreessen described blockchain as “the distributed trust network that the Internet always needed and never had.”[4]

In the same vein, with over 1,000 cryptocurrencies in circulation with a combined market capitalization of over $150 billion[5] (the great majority of which is represented by Bitcoin), it is not surprising that cryptocurrencies have attracted the attention of entrepreneurs, investors, financial institutions, and regulators alike.

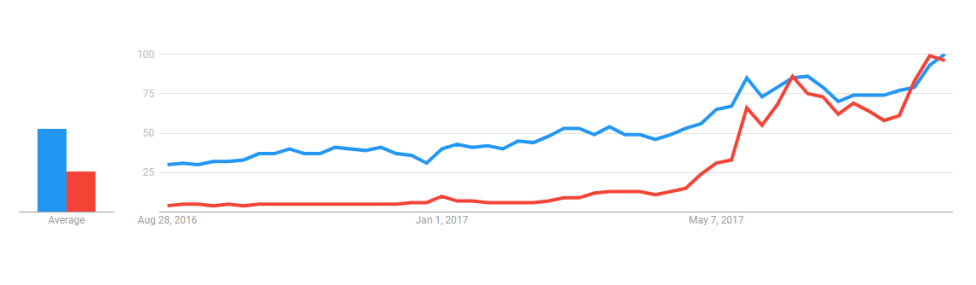

Consistent with a recent and rapid increase in our clients’ interest in blockchain and cryptocurrencies, Google search data (shown below, as of August 30, 2017) reflected the same trend:

• Blockchain

• Cryptocurrencies

The first step to understanding if and how blockchain and cryptocurrencies can drive innovation, add value, reduce costs, delays and inefficiencies while creating new revenue streams for a given business is to grasp the basics of the technology as well as the current legal and regulatory frameworks.

Part I of this article – Understanding Blockchain – addresses (1) how blockchain works, (2) recent case law calling for the use of blockchain, and (3) potential benefits from Delaware’s recently enacted blockchain legislation, an interesting example of real world blockchain applications.

Part II of this article – Understanding Cryptocurrencies – addresses (1) how cryptocurrencies work, (2) recent regulations relating to cryptocurrencies, and (3) key takeaways from the recent SEC pronouncements on token sales and related considerations.

Part I – Understanding Blockchain

1.1 How Blockchain Works

While there is no definition of what constitutes the constantly evolving blockchain technology, there are some fundamental characteristics that unite most blockchains. At a high level, blockchain can be described as a new form of information technology that, using a simple analogy, may be thought of as a shared spreadsheet, i.e., an immutable (write once and read only) ledger of time‑stamped transactions that is operated (i) in a decentralized manner by a peer-to-peer network of unaffiliated parties, (ii) through pre-defined consensus mechanisms in lieu of a central authority, and (iii) employing military-grade cryptography in order to prevent the ability to edit or tamper with the information recorded in it.

Depending on the objectives of a given project, blockchains can be structured so that they are:

- Public. Public blockchains are large distributed networks based on open-source code that is developed and maintained by their respective communities. Anyone can participate in a public blockchain at any level, i.e., anyone can read a transaction record as well as write data and validate the transactions (also referred to as “mining”) in exchange for a given cryptocurrency, without needing any permission or providing any identification. Examples of public blockchains include Bitcoin and Ethereum.

- Permissioned. Permissioned blockchains are also large distributed networks; however, they may or may not be based on open-source code. They operate under the leadership of a known entity that determines the role that individuals can play within the network. They may or may not use cryptocurrencies as the incentive mechanism for participants to serve the network. Examples of permissioned blockchains include Ripple and Corda.

- Private. Private blockchains are smaller and centralized networks. Their membership is limited and closely operated and controlled by one entity. As a result, the use of cryptocurrencies is not currently warranted. Examples of private blockchains include MONAX and Multichain.

Most importantly, the use of blockchain is not limited to cryptocurrencies. Blockchain can be used, in virtually any industry, to (i) create a shared, immutable record of any asset, including (a) tangible assets, such as real estate, and (b) intangible assets, such as intellectual property; and (ii) provide a tamper-proof audit trail of the transfer of any such asset without having to rely on a traditional trusted third party.

Not surprisingly, some of the most well-known applications of blockchain technology are in financial services (i.e., Abra, BitPesa and Circle, with respect to the remittance space; Blockstream, Chain and Digital Asset Holdings, with respect to trade finance and financial assets); however, “the practical applications for blockchain technology go way beyond financial assets. … Experiments in this space tend to be in early stages, but they range from medical records (MedRec, Pokitdok) to digital rights and micropayments (the Brave browser, Ascribe, Open Music Initiative), identity (Uport), and supply chain (Everledger, Hyperledger)”[6].

1.2 Recent Case Law Calling for the Use of Blockchain

Earlier this year, class action litigation resulting from the acquisition of Dole Food Company (“Dole”) forcefully demonstrated the potential failings of centralized ledger systems and provided an excellent example of one of the many applications of blockchain technology.

In November 2013, Dole consummated a merger pursuant to which Dole’s chairman, CEO and largest stockholder took the company private for $13.50 per share. In December 2015, as a result of a class action on behalf of Dole’s other shareholders, the parties settled for additional consideration of $2.74 per share plus interest.

However, as described in the Memorandum Opinion by Vice Chancellor J. Travis Laster of the Delaware Court of Chancery:[7] “The stipulation provided for the settlement proceeds to be distributed to class members through a traditional claims process. There were 36,793,758 shares in the class. At the conclusion of the claims process, however, claimants had submitted facially valid claims for 49,164,415 shares.” Somehow, shareholders owned 33.6% more Dole shares than there were Dole shares. This conundrum reflects a systemic issue affecting transactions where a centralized ledger held by DTC proves unable to determine ownership of registered shares at a specific point.[8]

Most of the inconsistency was caused by the unsettled trades during the final three days preceding Dole’s buyout. In other words, over 32 million shares traded in those last three days; however, as a result of our current system for clearing trades (known as “T+3”), DTC, the largest direct security holder of Dole, did not reflect all of the trades in Dole common stock on the day of the merger and during the two days preceding it. As far as DTC was concerned, whoever owned shares as of the close of the third day preceding the merger owned the shares at the time the merger closed.

Consequently, as Vice Chancellor Laster explained: “multiple owners could submit claims for shares involved in trades that had not cleared. A DTC participant who continued to hold the shares as reflected on DTC’s records could submit a claim, but so could the beneficial owner who was a client of the DTC participant that acquired the shares and therefore owned them as of closing.”

The rest of the inconsistency was caused by short sales. As Vice Chancellor Laster wrote: “The shorting resulted in additional beneficial owners who received the merger consideration, who fell within the technical language of the class definition, and who could claim the settlement consideration. Meanwhile, the lenders of the shares, not knowing that the shares were lent, also could claim the settlement consideration. This is another means by which two different claimants could submit facially valid claims for the same underlying shares.”

Notably, in a footnote to the Memorandum Opinion, Vice Chancellor Laster stated that “Distributed ledger technology offers a potential technological solution by maintaining multiple, current copies of a single and comprehensive stock ownership ledger.” In other words, systemic issues could be prevented by using a decentralized ledger, where every broker-dealer could instantly record trades that would be visible to all participants, clarifying ownership rights for every share within the system in real time.

1.3 Practical Benefits from Delaware’s Recently Enacted Blockchain Legislation

On August 1, 2017, following Vice Chancellor Travis Laster’s keynote address to the Council of Institutional Investors, where he called blockchain “a plunger that you can use to clean up the plumbing” of our capital markets, [9] Delaware became the first state to allow corporations to use blockchain technology for (i) the creation and maintenance of corporate records, including the stock ledger, and (ii) the electronic transmission of stockholder communications.[10]

The recently enacted legislation may benefit Delaware corporations for a host of reasons since corporations are now able to:

- Issue and track shares electronically on a real-time basis; delays, inconsistencies, and ensuing uncertainty caused by manually recording an issuance or a transfer of shares could be drastically reduced or eliminated;

- Eradicate the distinction between record holder and beneficial owner; complexities, confusion, and ensuing inefficiencies caused by the nominee system denounced by Vice Chancellor Laster in the Dole case could be eliminated;

- Settle transactions instantaneously; transaction costs and latency in transaction settlement could be drastically reduced or eliminated; and

- Directly communicate with investors; by allowing both shareholders and issuers to interact directly with each other, the need for third-party intermediaries like brokers, custodians, and clearinghouses and the related costs could be drastically reduced or eliminated.

Part II – Understanding Cryptocurrencies

2.1 How Cryptocurrencies Work

A cryptocurrency is generally understood to be a digital representation of value (which value is largely determined by the willingness of users to accept it) that is: (i) issued and managed through the use of blockchain technology; (ii) secured by cryptography; (iii) designed to work as a medium of exchange that can be transferred, stored, and traded electronically; (iv) not denominated in a fiat currency (although some cryptocurrencies are convertible into fiat currency); (v) not a liability of any entity nor backed by any central bank or government (and therefore lacking legal tender status); and (vi) supplied in limited amounts (i.e., Bitcoin has a 21 million bitcoin[11] cap), or predictable amounts (i.e., there are over 110 billion dogecoins, with approximately 5 billion dogecoins added every year).

As Bitcoin represents the most noteworthy cryptocurrency predicated on blockchain, understanding how Bitcoin works may also help in understanding how blockchain and other cryptocurrencies work. Using a simplified sequence of events and simplified terms, here is how blockchain works with respect to Bitcoin:

- Party “A” desires to transfer a certain number of bitcoins to party “B” (the “Transaction”). It is worth noting that party A and party B are known only by their cryptographically generated addresses (known as “public keys”), and not by their real identities. Using a simple analogy, a public key can be thought of like a bank account number.

- Using a randomly generated string of alphanumeric characters known as “private key,” party A digitally signs off on the Transaction. Using a simple analogy, a private key can be thought of like a PIN number (except that if one loses a private key, there is essentially no way to recover it).

- The Transaction is then broadcast to the Bitcoin network for verification. Participants in the Bitcoin network who verify whether party A has a sufficient number of bitcoins to complete the Transaction are known as “miners.”

- Miners verify the Transaction based on a pre-determined verification process. The verification process generally involves confirmation that party A is the rightful owner of the bitcoins it seeks to exchange, based on the transaction history recorded on the blockchain, which eliminates the double-spend problem. Miners are then compensated through the issuance of newly minted units of bitcoin.

- The settlement of the transaction may be contemporaneous with the verification process, whereby the information relating to the new ownership of the bitcoin is “cryptographically hashed” and permanently recorded on the blockchain.

- Once a transaction is verified, the records are time stamped and “chained,” so that party A’s and party B’s updated ownership of their respective bitcoins is displayed in a sequential manner to all parties on the network.

2.2 Recent Regulations Relating to Cryptocurrencies

Over the past few years, regulators have attempted to create a legal framework for cryptocurrencies. However, given that cryptocurrencies share some characteristics of securities, commodities, currencies, and payment systems, regulators have been struggling to come up with a consistent regulatory framework.

At the federal level, (i) the Financial Crimes Enforcement Network (FinCEN) treated “convertible” virtual currencies as “value” for purposes of anti-money laundering (AML) / combating the financing of terrorism (CFT) regulations, and stated: “The definition of a money transmitter does not differentiate between real currencies and convertible virtual currencies. Accepting and transmitting anything of value that substitutes for currency makes a person a money transmitter under the regulations implementing the Bank Secrecy Act”;[12] (ii) the Internal Revenue Service determined that, for purposes of federal taxation, virtual currency is property;[13] and (iii) the Commodities Futures Trading Commission defined virtual currencies as “commodities” under the Commodity Exchange Act[14].

Interestingly, on July 26, 2017, FinCEN, working in coordination with the U.S. Attorney’s Office for the Northern District of California, found that BTC-e a/k/a Canton Business Corporation (“BTC-e”), an internet-based, Russian‑located money transmitter that facilitates the purchase and sale of fiat currency and convertible virtual currency, willfully violated U.S. AML laws. [15] As a result, FinCEN assessed (i) a $110,003,314 civil money penalty against BTC-e, and (ii) a $12 million civil monetary penalty against BTC-e’s owner and operator, Alexander Vinnik, a Russian national, who was arrested in Greece on July 25, 2017. It is worth noting that this is the first time FinCEN has conducted an action against a foreign money transmitter that is doing business in the United States. FinCEN asserted jurisdiction over BTC-e because (i) a substantial part of its business is with customers in the United States, and (ii) some of the servers that participate in the processing of BTC-e’s transactions are located in the United States.

At the state level, approaches to, and definitions of, virtual currency vary considerably. While some states have enacted legislation defining virtual currency and requiring persons that provide virtual currency services to comply with a number of ongoing regulatory requirements (including New York State, which also requires such persons to obtain the so-called “BitLicense”), other states are taking generally less intrusive approaches and regulate virtual currency activities as a form of money services business under existing regulations.

It is worth noting that on July 19, 2017, the Uniform Law Commission (a private body of judges, professors, lawyers and legislative drafting attorneys, also known as the National Conference of Commissioners on Uniform State Laws), finalized and approved the Uniform Regulation of Virtual Currency Business Act (the “Virtual Currency Business Act”),[16] in an attempt to provide a template for state legislatures and create a consistent regulatory framework for virtual currencies across all states. Among other things, the Virtual Currency Business Act provides that any business that has the “power to execute unilaterally or prevent indefinitely a virtual currency transaction” must (i) obtain a license and (ii) create and maintain policies and procedures to prevent, among other things, fraud, money laundering and funding of terrorist activity.

2.3 Key Takeaways from the Recent SEC Pronouncements on Token Sales and Related Considerations

There are several ways in which cryptocurrencies can be acquired. In addition to the acquisition from another holder, or as compensation through the “mining” process described above, cryptocurrencies can be purchased through a cryptocurrency exchange or trading platform. Most interestingly, cryptocurrencies can be purchased in the context of so-called “token sales,” a capital-raising method that a significant number of emerging and established companies offering blockchain-based services have been pursuing as an alternative to traditional forms of fundraising. As of August 25, 2017, it is estimated that nearly $1.8 billion has been raised via token sales.[17]

The U.S. Securities and Exchange Commission (“SEC”) has not yet offered a comprehensive framework as to the criteria for determining which tokens should be deemed securities under existing laws. Indeed, on July 25, 2017, the SEC merely reiterated that “Whether a particular investment transaction involves the offer or sale of a security – regardless of the terminology or technology used – will depend on the facts and circumstances, including the economic realities of the transaction.[18]”

Nevertheless, in light of the recent SEC pronouncements,[19] companies contemplating a token sale should be aware that, depending on how tokens are structured, a token sale may need to comply with the registration requirements of the U.S. federal securities laws, or rely on an exemption therefrom.

Given the significant risks – both known and unknown – the token sales may pose, token issuers should consider the following items when structuring a token sale:

- Facts and Circumstances. Tokens can be structured with a wide-ranging spectrum of characteristics. The SEC reiterated the importance of a “facts and circumstances and economic realities of the transaction” analysis of each token sale to determine if the sale was a securities offering. Whether a token is a security will depend upon how the token is structured, and should be analyzed under the traditional tests for determining whether an instrument is a security.

- The Howey Test. The SEC will apply the investment contract test set forth in the septuagenarian SEC v. W.J. Howey Co. case[20] (the “Howey Test”). The core factors of the Howey Test – as evolved over the years – are: (i) whether purchasers of the instrument contributed money or valuable goods or services;[21] (ii) whether purchasers were investing in a common enterprise and reasonably expected to earn profits through that enterprise;[22] and (iii) whether the expected profits are to be derived from the efforts of others.[23] Therefore, while token sales are not necessarily, in all cases, securities offerings, issuers of tokens must carefully review the expectations of the potential token holders as well as the rights they are afforded in light of the Howey test.

- The Securities Act. If a token is structured so that it entitles its holder to a share of profits, revenues, dividends, or voting rights, or provides an expectation of profits based on the projected utility that such token may have in the future, then, such token is likely to be deemed a security. Offerings of tokens deemed as securities that have a U.S. nexus need to comply with the registration requirements of the U.S. federal securities laws, or rely on an exemption therefrom, such as Regulation D or Regulation S. Offerings of tokens deemed as securities would also be subject to limitations on resales or transfers, and general solicitation may be prohibited. In addition, given that the anti-fraud provisions of the U.S. securities laws apply with respect to the issuance, sale, and trading of tokens deemed as securities, regardless of whether the offering is registered or exempt, careful consideration should be given to ensure that prospective investors receive satisfactory disclosure about the offering, the associated tokens, the use of proceeds, and the related risks of the project.

- Broker-Dealer Considerations. If the tokens are deemed securities, anyone engaging in the business of trading such tokens should consider whether they need to register as a broker‑dealer with the SEC and with the Financial Industry Regulatory Authority (FINRA). In addition, a person or entity that receives a portion of the tokens or other compensation in connection with the token sale may need to register as a broker-dealer, and a person or entity that provides any advice regarding the purchase of the tokens may need to register as an investment adviser.

- The Investment Company Act. If the tokens are deemed securities, the Investment Company Act of 1940 could apply and require “investment companies” to register with the SEC, unless they qualify for one of several exclusions from the definition. “Generally, an investment company is an issuer that is engaged or proposes to engage in the business of investing, reinvesting, owning, holding, or trading in securities, and owns or proposes to acquire “investment securities” having a value exceeding 40 percent of the value of its total assets (exclusive of government securities and cash items) on an unconsolidated basis. For this purpose, “securities” and “investment securities” are broadly defined, and in some cases include instruments that may not be securities under the Howey test”.[24]

- Tokens Not Deemed As Securities? If a token is structured so that it (a) can be currently used to purchase goods or services from its issuer, or operate a website or an application of its issuer (rather than offering the right to access a future service that has not yet been built), as in the case of the so called “access tokens,” “app tokens,” or “utility tokens”, and (b) does not have traditional characteristics of securities, including an expectation of profits derived from the efforts of others, then the token may not be deemed a security. However, issuers should analyze this scenario on a case-by-case basis, keeping in mind that the value of a token may be influenced by the increased demand for services or goods of a token’s issuer, and therefore cause the token to take on securities-like characteristics.

- Commodity Futures Trading Commission. The Commodity Futures Trading Commission (“CFTC”) stated that “Bitcoin and other virtual currencies are encompassed in the definition and properly defined as commodities.”[25] Therefore, the CFTC may exercise jurisdiction over a token sale under the theory that a token sale constitutes an offering of a commodity futures contract, commodity interest, or commodity subject to the jurisdiction of the CFTC.

- Money Transmission. Token sales may also subject an issuer to regulation as a money services business, which could mean that the issuer may need to comply with a wide range of federal and state regulations, including money transmitter laws and anti-money laundering and “know-your-customer” provisions.

*******

Financial institutions, global corporations, venture capitalists, emerging companies and major players in virtually every industry are embracing blockchain’s and cryptocurrencies’ capabilities and applications, while navigating the complex worlds of regulation and legal oversight. The opportunities are exciting, and the changes are expected to be disruptive. While nobody wants to be first, but rather a fast follower, failure to understand blockchain’s and cryptocurrencies’ technologies may trigger a Kodak moment, and put successful companies at the mercy of those that quickly pivoted.

ENDNOTES

[1] See “The last Kodak moment?” available at http://www.economist.com/node/21542796.

[2] See “Deep Shift Technology Tipping Points and Societal Impact” (Survey Report, September 2015), available at http://www3.weforum.org/docs/WEF_GAC15_Technological_Tipping_Points_report_2015.pdf.

[3] See “Emerging Theme Radar” (December 2, 2015), available at http://www.goldmansachs.com/our-thinking/pages/macroeconomic-insights-folder/what-if-i-told-you/report.pdf.

[4] See “Marc Andreessen: In 20 years, we’ll talk about Bitcoin like we talk about the Internet today” (May 21, 2014), available at https://www.washingtonpost.com/news/the-switch/wp/2014/05/21/marc-andreessen-in-20-years-well-talk-about-bitcoin-like-we-talk-about-the-internet-today/?utm_term=.35e4352e5ea5.

[5] See CoinMarketCap (August 25, 2017), https://coinmarketcap.com/currencies/views/all/, and https://coinmarketcap.com/charts/.

[6] See “How Blockchain Applications Will Move Beyond Finance” (March 2, 2017) available at https://hbr.org/2017/03/how-blockchain-applications-will-move-beyond-finance.

[7] See “Memorandum Opinion in re Dole Food Company, Inc. Stockholder Litigation” (February 15, 2017) available at http://courts.delaware.gov/Opinions/Download.aspx?id=252690.

[8] There is other case law demonstrating similar issues with proxy voting and merger consideration payouts. See, among others, In re Appraisal of Dell Inc. (Dell Continuous Ownership), 2015 WL 4313206 (Del. Ch. July 30, 2015).

[9] See J. Travis Laster, Vice Chancellor, Del. Chancery Court, “The Block Chain Plunger: Using Technology to Clean Up Proxy Plumbing and Take Back the Vote”, Keynote Speech at Fall 2016 meeting of Council of Institutional Investors (Sept. 29, 2016), available at http://www.cii.org/files/09_29_16_laster_remarks.pdf.

[10] For a granular analysis of the recently enacted blockchain-related amendments to the Delaware General Corporation Law, see “Delaware Governor Signs Groundbreaking Blockchain Legislation into Law” (July 27, 2017), available at https://www.mofo.com/resources/publications/170727-delaware-blockchain-legislation.html.

[11] The unit of currency within the Bitcoin network is called “bitcoin” (i.e., not capitalized), or BTC.

[12] See “Application of FinCEN’s regulations to persons administering, exchanging or using virtual currencies,” Guidance, Department of the Treasury Financial Crimes Enforcement Network, FIN-2013-G001, 18 (March 18, 2013) available at https://www.fincen.gov/sites/default/files/shared/FIN-2013-G001.pdf.

[13] See Notice 2014-21, Internal Revenue Services, March 2014 – available at https://www.irs.gov/pub/irsdrop/n-14-21.pdf.

[14] See “CFTC Orders Bitcoin Options Trading Platform Operator and its CEO to Cease Illegally Offering Bitcoin Options and to Cease Operating a Facility for Trading or Processing of Swaps without Registering” (September 17, 2016), available at http://www.cftc.gov/PressRoom/PressReleases/pr7231-15

[15] See “FinCEN Assessment of Civil Money Penalty in the Matter of BTC-E a/k/a Canton Business Corporation and Alexander Vinnik” (July 26, 2017), available at https://www.fincen.gov/sites/default/files/enforcement_action/2017-07-26/Assessment%20for%20BTCeVinnik%20FINAL%20SignDate%2007.26.17.pdf.

[16] See “Uniform Regulation of Virtual Currency Business Act” (July 19, 2017) available at http://www.uniformlaws.org/shared/docs/regulation%20of%20virtual%20currencies/2017AM_URVCBA_AsApproved.pdf.

[17] See “All-Time Cumulative ICO Funding” (August 25, 2017) available at https://www.coindesk.com/ico-tracker.

[18] See “SEC Issues Investigative Report Concluding DAO Tokens, a Digital Asset, Were Securities” (July 25, 2017) available at https://www.sec.gov/news/press-release/2017-131.

[19] See “Report of Investigation Pursuant to Section 21(a) of the Securities Exchange Act of 1934: The DAO” (July 25, 2017) available at http://www.sec.gov/litigation/investreport/34-81207.pdf, and “Investor Bulletin: Initial Coin Offerings” (July 25, 2017) available at https://www.investor.gov/additional-resources/news-alerts/alerts-bulletins/investor-bulletin-initial-coin-offerings.

[20] See SEC v. W.J. Howey Co., 328 U.S. 293 (1946).

[21] See Howey, 328 U.S. at 301; see also Uselton v. Comm. Lovelace Motor Freight, Inc., 940 F.2d 564, 574 (10th Cir. 1991).

[22] See SEC v. Edwards, 540 U.S. 389, 394 (2004).

[23] See Howey, 328 U.S. at 299.

[24] See “Howey Got Here: SEC Issues Guidance on Token Offerings” (July 26, 2017)

https://www.mofo.com/resources/publications/170726-howey-got-here-sec-token-offerings.html#_ftn1.

[25] See “Order Instituting Proceedings Pursuant to Sections 6(C) and 6(D) of the Commodity Exchange Act, Making Findings and Imposing Remedial Sanctions” (September 17, 2015), available at http://www.cftc.gov/idc/groups/public/@lrenforcementactions/documents/legalpleading/enfcoinfliprorder09172015.pdf.

This post comes to us from Morrison & Foerster LLP. It is based on the firm’s client alert, “Don’t Want To Be The Next Kodak? Embrace Blockchain,” dated August 30, 2017, and available at Law 360, here.