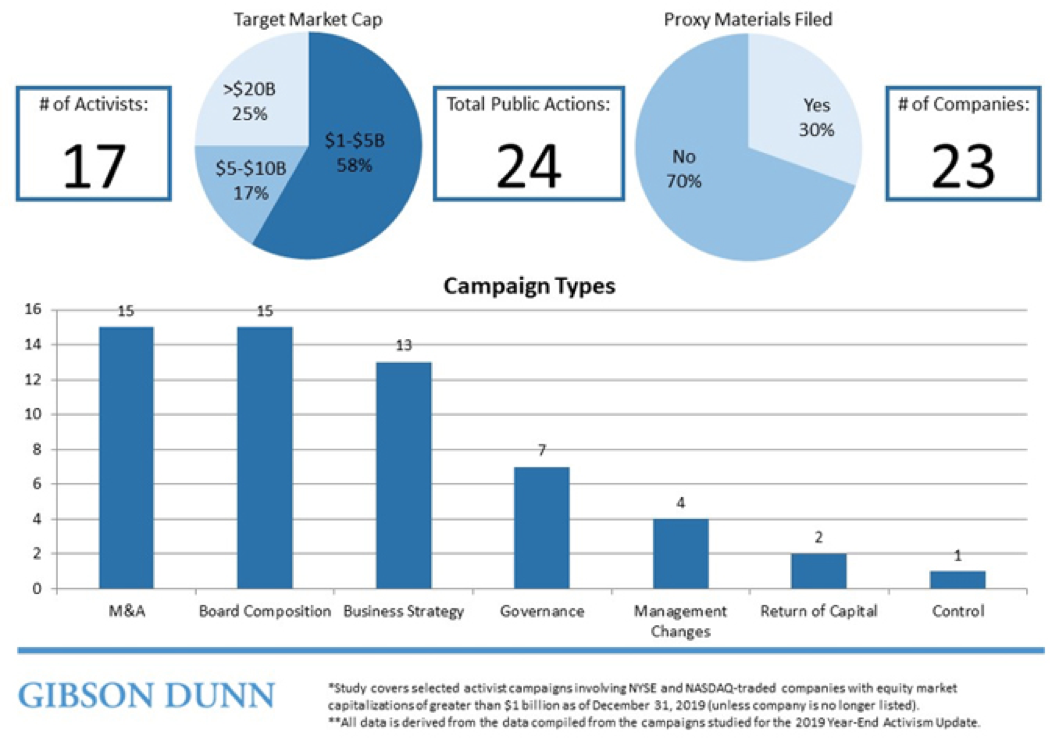

This Client Alert provides an update on shareholder activism activity involving NYSE- and Nasdaq-listed companies with equity market capitalizations in excess of $1 billion and below $100 billion (as of the last date of trading in 2019) during the second half of 2019. Announced shareholder activist activity declined relative to the second half of 2018. The number of public activist actions (24 vs. 40), activist investors taking actions (17 vs. 29) and companies targeted by such actions (23 vs. 34) each decreased substantially. The slowdown was in contrast to the first half of 2019, during which period shareholder activism activity was robust. On a full-year basis, however, 2019 represented a slowdown in activism versus 2018, as reflected in the number of public activist actions (75 vs. 98), activist investors taking actions (49 vs. 65) and companies targeted by such actions (64 vs. 82).

Despite the overall decline in shareholder activism activity, certain trends continued unabated. During the period spanning July 1, 2019 to December 31, 2019, two of the 23 companies targeted by activists—Instructure, Inc. and Occidental Petroleum Corporation—were the subject of multiple campaigns. The activism campaign launched by activist Carl Icahn against Occidental Petroleum Corporation was supported by activist Krupa Global Investments. In addition, certain activists launched multiple campaigns during the second half of 2019: Carl Icahn, Elliott Management, Land & Buildings, Sachem Head Capital Management and Starboard Value. These five activists represented 42% of the total public activist actions that began during the second half of 2019.

By the Numbers – H2 2019 Public Activism Trends

The rationales for activist campaigns during the second half of 2019 remained consistent with those in the first half of 2019. Over both periods, M&A, board composition and business strategy represented the most frequent rationales animating shareholder activism campaigns. These three rationales collectively reflected approximately 75% of activism campaigns during each time period (noting that many campaigns have multiple rationales), with other rationales (governance, management changes, return of capital and change of control) representing the minority. M&A (which includes advocacy for or against spin-offs, acquisitions and sales) and board composition were each a motivator for activist activity in the case of 63% of campaigns (as compared to 55% and 67%, respectively, in the first half of 2019). M&A and board composition were followed by business strategy (54% of campaigns, as compared to 51% in the first half of 2019). On the other hand, advocacy for changes in governance (29% of campaigns in the second half of 2019), managerial changes (17% of campaigns), return of capital (8% of campaigns) and attempts to take corporate control (4% of campaigns) represented less frequently cited rationales for activist campaigns. Proxy solicitation occurred in 29% of the campaigns, representing a significant increase relative to the first half of 2019, in which 15% of campaigns featured activists filing proxy materials. (Note that the above-referenced percentages total over 100%, as certain activist campaigns had multiple rationales.)

The diminution in shareholder activism activity brought with it a decline in publicly filed settlement agreements. Only five such settlements were filed during the review period, which is the lowest number observed for a half-year-period since 2014. Those settlement agreements that were filed had many of the same features noted in prior reviews, however, including voting agreements and standstill periods as well as non-disparagement covenants and minimum and/or maximum share ownership covenants. Expense reimbursement provisions were included in approximately half of those agreements reviewed, which is consistent with historical trends. We delve further into the data and the details in the latter half of this Client Alert.

Though not covered in this Client Alert, we note that early indications suggest that the COVID-19 pandemic has caused a decline in shareholder activism activity during the first half of 2020. However, some activists may see opportunities in market dislocation to increase pressure on certain targets and/or to increase their positions in certain companies opportunistically. These trends may be borne out in both the types of targets on which activists focus as well as in the rationales for the campaigns that activists launch. We will analyze these trends in detail during our next shareholder activism update.

This post comes to us from Gibson, Dunn & Crutcher LLP. It is based on the firm’s memorandum, “M&A Report – 2019 Year-End Activism Update,” dated May 11. 2020, and available here.