In the market for corporate control, regulation has long been viewed as a tax on activity, a hurdle to overcome, or a cost to be priced in. The conventional wisdom is straightforward: More regulation equals less activity. However, in a new study, we challenge this view, suggesting that the volume of regulation matters less than its structure.

In the study, we investigate the role of regulatory fragmentation, where a single corporate activity is overseen by multiple, often uncoordinated federal agencies. We argue that this form of bureaucratic complexity does not merely dampen deal flow; it significantly reshapes the market. It serves as a powerful deterrent, killing marginal deal, while paradoxically acting as a screening mechanism that ensures only the most strategically superior transactions survive.

About Regulatory Fragmentation

Our study first distinguishes between regulatory burden and regulatory fragmentation. Regulatory burden is typically measured by the number of rules a firm must follow, while fragmentation refers to the incoherence of oversight. It occurs when jurisdiction over a specific issue is divided among agencies with differing mandates, timelines, and enforcement priorities.

A classic example is the acquisition of a healthcare or tech firm, where data privacy is a central asset. The target firm may simultaneously answer to the Federal Trade Commission (FTC) regarding consumer protection, the Securities and Exchange Commission (SEC) regarding material disclosures, and possibly industry-specific bodies such as the FDA or FCC. The friction does not arise from the strictness of the rules, but from their dissonance. One agency may demand transparency (SEC), while another mandates confidentiality (FDA under HIPAA). One may operate on a swift timeline, while another drags its feet. This juggling act creates a unique form of friction that makes a firm significantly harder to value and integrate into the new company.

The Deterrence Effect: Why Fragmentation Kills Deals

We document that regulatory fragmentation serves as a deterrent to M&A. A one-standard-deviation increase in a firm’s regulatory fragmentation score reduces its likelihood of becoming an acquisition target by approximately 21.7%.

There are two ways that this structural burden scares off acquirers.

-

The Information Uncertainty Channel

In M&A, information is the currency of the realm; acquirers need to know what they are buying. Fragmentation degrades the quality of information available to the market. We find that firms subject to high regulatory fragmentation exhibit higher idiosyncratic stock volatility, greater net income volatility, and significantly wider dispersion in analyst earnings forecasts. When multiple agencies pull a firm in different directions, its financial reporting and performance outlook become opaque. For a potential acquirer, this opacity translates into risk. Due diligence becomes a nightmare of what-ifs. If an acquirer cannot accurately price the target due to regulatory fog, it is more likely to walk away.

-

The Organizational Frictions Channel

Beyond the fog of information, fragmentation imposes costs. The study finds a positive correlation between fragmentation and higher selling, general, and administrative (SG&A) expenses, as well as cost of goods sold (COGS). These are the direct costs incurred by compliance departments trying to serve multiple masters. Furthermore, fragmentation forces target firms into a defensive posture. To navigate regulatory minefields, these firms tend to adopt conservative financial policies, including paying lower dividends, repurchasing fewer shares, and slowing asset growth. While this conservatism is a rational survival strategy for the target, it signals low growth potential to the market. Acquirers looking for dynamic, scalable platforms are often repelled by firms that have been forced into timidity by regulators.

The deterrent effect is not uniform. It is most pronounced in cash-financed deals, where the acquirer bears the full risk of the asset after -closing, and in cross-state transactions, where federal fragmentation is compounded by the need to coordinate across various states.

The Screening Paradox: Survival of the Fittest

While fragmentation reduces the quantity of deals, it appears to increase the quality of the deals that actually get done. The study analyzes the cumulative abnormal returns (CARs) for the targets that are acquired despite high fragmentation. The results are striking: Targets in highly fragmented environments experience more favorable stock market reactions than do their peers. How can a friction that deters buyers also drive value?

Because the barriers to entry are so high, casual or marginal bidders are weeded out early. The only acquirers willing to pay the regulatory tax and navigate the chaos are those who have identified massive, undeniable synergies. They are not buying the target for a quick flip or a modest bolt-on, they are buying it because the strategic fit is so compelling that it outweighs the bureaucratic complexities. The data support this. The fragmentation premium is most pronounced in deals involving targets that rely heavily on R&D and in industries where the merging firms share similar products. In essence, regulatory fragmentation raises the bar for deal logic. Only the best deals clear the hurdle.

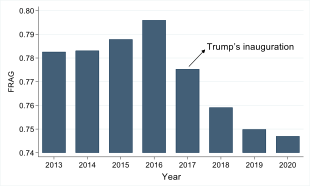

The Trump Shock

We use the 2016 election of Donald Trump as an exogenous shock. The Trump administration entered office promising deregulation, with a particular emphasis on reducing administrative redundancy. Following the inauguration, the data show a sharp decline in aggregate regulatory fragmentation scores (see below).

Using a difference-in-differences (DID) estimation model, we demonstrate that firms that were highly fragmented prior to 2017 experienced a significant increase in their likelihood of becoming acquisition targets relative to their peers after the administration’s policy shift took effect. This provides evidence that red tape was the bottleneck holding back market activity.

Implications for Policy and Practice

For policymakers and government officials, the takeaway is nuanced. The damage done to the corporate-control market does not come solely from the strictness of rules, but from the lack of coordination among the rule-makers. A goal of efficient government should focus less on removing necessary protections and more on harmonizing the mandates of overlapping agencies. Streamlining oversight could unlock significant value in the M&A market without necessarily deregulating the underlying activity.

For lawyers and investment bankers, the study validates the compliance discount often seen in complex sectors. It suggests that in fragmented industries (such as biotech, fintech, and energy), the role of the adviser is not just to identify value, but to construct a narrative that helps the acquirer pierce the fog of regulatory uncertainty.

Regulatory fragmentation acts as a double-edged sword. It imposes a substantial tax on market liquidity, suppressing deal volume and forcing firms into defensive conservatism. Yet, by making acquisitions difficult, it ensures that the capital that does flow is directed toward transactions with the highest conviction and greatest potential for value creation. In the messy reality of the administrative state, red tape doesn’t just bind – it selects.

Iftekhar Hasan is a professor at Fordham University’s Gabelli School of Business, and Ming Gu, Dongxu Li, and Hui Hu are professors at Xiamen University. This post is based on their recent paper, “Juggling Red Tape: The Effects of Regulatory Fragmentation on Takeover Targets,” available here.