The Federal Reserve and FDIC took actions last week designed to facilitate crypto-related activities. The Federal Reserve rescinded its anti-crypto 2023 policy statement and replaced it with a more permissive stance designed to facilitate innovation, and requested information on a potential payments-focused alternative to a master account. The FDIC issued the first proposal for a permitted payment stablecoin issuer application process under the GENIUS Act.

Federal Reserve’s new policy statement signals a more permissive stance towards state member bank crypto activities

The Federal Reserve rescinded its 2023 policy statement (covered in our client update), which among other things set forth a presumption against the safety and soundness of certain crypto asset activities that it described as “novel and unprecedented.” The Federal Reserve has replaced the 2023 policy statement with a new policy statement that signals a more innovation-friendly approach, especially with respect to activities conducted by uninsured state member banks.

Section 9(13) of the Federal Reserve Act (FRA) authorizes the Federal Reserve to limit the activities as principal of state banks that are members of the Federal Reserve System in a manner consistent with section 24 of the Federal Deposit Insurance Act (FDIA), which in turn generally limits the activities as principal of state banks insured by the FDIC to the same activities as principal permitted for national banks unless specially authorized by the FDIC. In its 2023 policy statement interpreting this authority, the Federal Reserve stated its strong presumption that requests from both insured and uninsured state member banks to engage in novel and unprecedented activities that have not been previously deemed permissible for insured state banks or national banks would be denied. The 2023 policy statement singled out certain crypto activities—holding crypto-assets as principal and issuing crypto tokens (other than “dollar tokens”)—as of particular concern and presumptively impermissible.

Citing an “evolving understanding of the crypto-asset sector” and a desire to facilitate innovation, the Federal Reserve has rescinded the 2023 policy statement and replaced it with a new policy statement. The rescission occurs against the backdrop of the Federal Reserve’s (and FDIC and OCC’s) repeal of other 2022 and 2023 statements and guidance that took a skeptical view of crypto activities.

Key highlights of the replacement policy statement are as follows:

- The 2025 policy statement incorporates the principle of “different activity, different risks, different regulation” and a commitment to facilitating innovation. Governor Michael S. Barr dissented from the recission of the 2023 policy statement because of the replacement statement’s embrace of this principle; he characterized the principle as new and likely to encourage regulatory arbitrage.

- The 2025 policy statement removes from the record the discussion in the 2023 policy statement that singled out specific crypto activities. Among other things, the preamble to the 2023 policy statement said: “The Board [of Governors of the Federal Reserve System] generally believes that issuing tokens on open, public, and/or decentralized networks, or similar systems is highly likely to be inconsistent with safe and sound banking practices.” Thus, this position is no longer the official policy of the Federal Reserve.

- The 2025 policy statement distinguishes between uninsured and insured state member banks and states that the Federal Reserve may authorize uninsured state banks that are either member banks or applying to become member banks to engage in certain activities that may not be permissible for national banks or insured state banks.

- When considering such activities, the Federal Reserve will consider whether an uninsured state member bank could manage safety and soundness risks through a financial profile “at least as effective as deposit insurance”, such as sufficient total loss-absorbing capacity or high-quality liquid assets equal to 100% of the bank’s demand deposits and short-term liabilities.

- The Federal Reserve will also consider whether the uninsured state member bank “has a resolution plan that demonstrates how the bank could be recapitalized or wound down in an orderly manner if it fails to remain a viable going concern.”

- Certain special purpose uninsured state-chartered institutions are required to observe similar financial safeguards and, thus, may be well-positioned candidates to become members of the Federal Reserve System under the new policy statement.

Federal Reserve requests input on payment account alternative to a master account

Separately, the Federal Reserve released a request for information (RFI) on a contemplated prototype for a special purpose “payment account” to be held at regional Federal Reserve Banks. The prototype payment account would be dedicated to payment activity and could provide an alternative to a full master account. A master account is an account held by an eligible financial institution at its regional Federal Reserve Bank through which the account holder can receive various payment and other services and earn interest on reserve balances. The RFI builds off of Governor Waller’s “skinny master account” proposal and is being considered in response to feedback from entities with nontraditional business models that see the process for applying for master account access as too long and uncertain. Governor Barr dissented from the issuance of the RFI because of its lack of specificity as to anti-money laundering safeguards, but his dissent articulated general support for a payment account prototype.

The key features of a payment account, as described in the RFI, are as follows:

Similarity to master accounts

- Eligibility: The same institutions that are eligible for a Federal Reserve master account and related services would be eligible for a payment account. The payment account proposal would not expand or otherwise change legal eligibility for access to Federal Reserve accounts and services.

Differences from master accounts

- Focus on payment activity: Use of a payment account would be limited to the express purpose of clearing and settling the institution’s payment activity.

- No correspondent relationships: Account holders would only be permitted settle their own payments and hold their own reserves—i.e., they would not be permitted to settle transactions for respondent institutions.

- Limits on balances:

- Overnight balance limit: The Federal Reserve is considering setting the limit at the lesser of $500 million or 10% of the holder’s assets, though Federal Reserve Banks could have the ability to adjust the balance limit on a case-by-case basis.

- Intraday balance: The RFI does not include a proposed limit for intraday balances.

- No interest on balances: Balances held in a reserve account would not be eligible to earn interest.

- No intraday credit: Account holders would not be permitted to receive intraday credit from a Federal Reserve Bank (also known as daylight overdrafts). As a result, payments would need to be prefunded. Neither master accounts nor payment accounts may incur overnight overdrafts.

- Narrower service offerings: Payment accounts would only receive a subset of Federal Reserve services, and all provided services would need to have automated controls to prevent daylight overdrafts.

- Permitted services would include: Fedwire Funds Service, National Settlement Service, FedNow Service and Fedwire Securities Service for Free Transfers.

- Any services not listed above would be excluded, such as: FedACH Services, Check Services, FedCash and Fedwire Securities Service for Transfer Against Payment (i.e., delivery-versus-payment).

- No discount window access: Payment accounts would not have access to discount window lending.

- Shorter approval timeframe: While no binding timeline is specified, the Federal Reserve expects that account access decisions would be made within 90 days of the relevant regional Federal Reserve Bank receiving all materials.

The RFI contemplates that an interested and eligible institution would apply to its regional Federal Reserve Bank for access. The RFI states that the relevant Federal Reserve Bank would have discretion to approve or deny the request and to impose additional restrictions and risk controls on a case-by-case basis.

FDIC proposed rule sets out PPSI application process for FDIC-supervised institutions

The FDIC proposed a rule that would establish a process and review framework for applications to the FDIC for an insured depository institution (IDI) subsidiary to become a permitted payment stablecoin issuer (PPSI) under the GENIUS Act. The proposal closely tracks the provisions of the GENIUS Act and would apply only to FDIC-supervised institutions, namely state banks that are not members of the Federal Reserve System and state savings associations, that seek to license a subsidiary as a PPSI. The Federal Reserve, OCC and NCUA are also required to issue their own rules but have not yet done so.

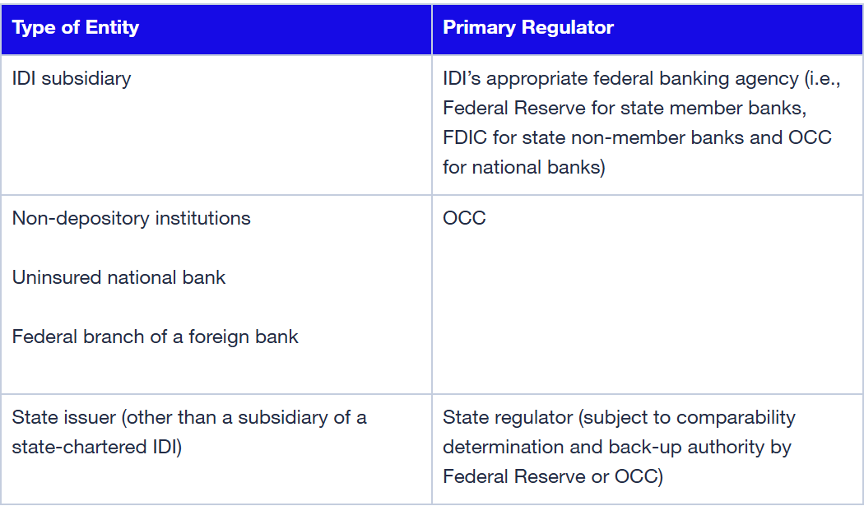

The FDIC’s action marks the first proposed rule under the GENIUS Act, which was enacted on July 18, 2025 and sets out a federal statutory framework for the regulation of payment stablecoins. For an overview of the GENIUS Act please see our client update. As relevant here, the GENIUS Act authorizes various types of entities to become licensed as a PPSI upon applying to and receiving approval from the relevant regulator, as described in the chart below. On the federal level, the FDIC will be the primary regulator and licensor for subsidiaries of FDIC-supervised institutions.

PPSI Entity Types and Primary Regulators

Proposed application process

The application process for a subsidiary of an FDIC-supervised institution to become a PPSI is similar to existing FDIC application processes in many respects. Indeed, the proposed regulations would be appended to 12 C.F.R. Part 303, the FDIC’s existing regulations governing most applications. The proposed application process would be structured as follows:

- Prepare letter application: An FDIC-supervised institution would prepare a “letter application” providing the required informational components (discussed below) and requesting approval from the FDIC for its subsidiary to become a PPSI. The FDIC has proposed a letter format as opposed to a standard template under the theory a letter would be more flexible and, thus, less burdensome to applicants.

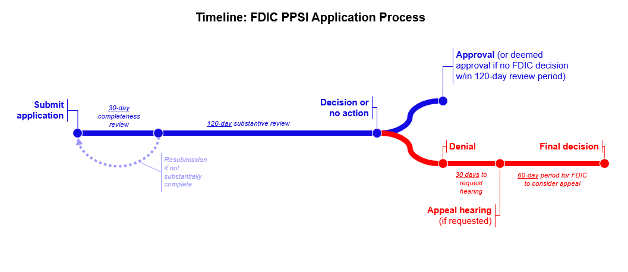

- Submit the application for substantial completeness review: The application would be submitted to the FDIC regional office covering the region where the applicant is located. At that point the FDIC would have 30 days to determine whether the application is substantially complete.

- This review timeline is mandated by the GENIUS Act and, consistent with the Act, the FDIC has defined substantially complete to mean the application provides the FDIC with sufficient information to evaluate whether a license should be granted based on the five statutory factors provided in the GENIUS Act (discussed below). If the application is not considered substantially complete, the FDIC shall specify the additional information the applicant shall provide in order for the application to be considered substantially complete.

- If a material change in circumstances occurs following an application being deemed complete, e.g., a change in the applicant’s financial condition, the applicant must notify the FDIC and the application will be treated as a new application.

- If substantially complete, FDIC review and decision: Following receipt of a substantially complete application, the FDIC has 120 days to approve or deny the application based on the five statutory factors in the GENIUS Act. If no decision is rendered within that period, the application is deemed automatically approved. The FDIC may approve an application with conditions; the preamble to the proposal states the FDIC expects to impose only standard conditions, e.g., providing final documents if drafts were submitted.

- Appeal of denial: As required by the GENIUS Act, the proposal contains an appeal process for a denied application. The appeal would use the procedures for appeals of material supervisory determinations but within the timelines provided under the GENIUS Act. Among other things, a denied applicant would have a right to a hearing if requested within 30 days of the denial where they could present evidence in favor of a contrary decision. The FDIC must then render a decision on appeal within 60 days and provide a statement of the basis for its determination.

The below timeline provides a visual summary of the key steps in the application process.

Process for consortiums

The preamble to the proposal contemplates that certain applicants may pursue a consortium structured as a subsidiary of an FDIC-supervised institution. It further notes that the FDIC would anticipate accepting and processing a single application on behalf of all other FDIC-supervised members of the consortium if the consortium is considered a subsidiary of each member. The proposal would define subsidiary by reference to section 3 of the FDIA, which in turn defines subsidiary as “any company which is owned or controlled directly or indirectly by another company” and incorporates the Bank Holding Company Act’s three-pronged definition of control.

Process for GENIUS Act safe harbor waiver

Upon the effective date of the GENIUS Act, only a PPSI may issue a payment stablecoin in the United States. However, the federal payment stablecoin regulators—and the FDIC in the case of a subsidiary of an FDIC-supervised institution—may waive this requirement for up to 12 months after the effective date of the Act with respect to an applicant with a pending PPSI application received prior to the effective date. Although not explicit, it appears that the FDIC will require a pending application to be considered substantially complete to be eligible for this safe harbor.

What will the FDIC evaluate in reviewing applications?

Review factors

The GENIUS Act specifies five factors to be used by the federal payment stablecoin regulators in evaluating a PPSI application. An application can only be denied if the activities of the applicant would be unsafe or unsound based on those factors. The FDIC proposal discusses these factors in a way that closely tracks the GENIUS Act text:

- Factor 1: Ability to meet GENIUS Act requirements. An applicant must show the issuer would be able to meet the requirements under section 4 of the GENIUS Act for issuing a payment stablecoin. Among other things, the FDIC may consider the potential issuer’s financial condition and resources, planned activities and ability to maintain and manage reserves. The FDIC will also consider whether the proposed issuer will limit its activities to permissible activities, which are to “issue and redeem payment stablecoins, manage related reserves, provide certain payment stablecoin and reserve custodial and safekeeping services, undertake other activities that directly support those activities, and engage in digital asset service provider activities.”

- Factors 2 and 3: Quality of management. An applicant must show the issuer has management that are fit and competent. Among other things, the FDIC may consider whether a director or officer has been convicted of certain felonies and whether the proposed management has sufficient experience and qualifications.

- Factor 4: Redemption policy. An applicant must demonstrate that its proposed redemption policy satisfies the GENIUS Act requirements. Among other things, the FDIC will consider whether the applicant has established clear and conspicuous procedures for timely redemption of outstanding payment stablecoins.

- Factor 5: Other factors. The GENIUS Act permits regulators to consider any other factors that are necessary to ensure the safety and soundness of the PPSI. The FDIC’s proposal would not establish any additional factors.

Contents of the application

The proposal would adopt the following informational requirements for an application:

- Description of activities: An applicant must describe the proposed payment stablecoin activities, including the characteristics and features of the proposed payment stablecoin as well as the identities, roles and responsibilities of the entities involved in the proposed payment stablecoin activities, including by the proposed issuer’s affiliates. The applicant should also describe how the issuer plans to maintain the payment stablecoin’s value, including if the applicant plans to serve as a source of strength or provide guarantees to the proposed issuer. Any incidental activities to stablecoin issuance should also be described, presumably to allow the FDIC to determine whether such incidental activities are permissible or pose a safety or soundness risk.

- Financial projections: An applicant must submit pro forma financial projections covering the issuer’s first three years of operations. The application should also discuss the planned capital and liquidity structure and any financial commitments from directors, officers or shareholders. Any consortium commitments would be relevant as well. This section should also discuss how reserve assets will be managed, including whether any reserves will be tokenized and what circumstances could prompt reserve asset composition to change. Of course, any reserve asset management plan will need to be consistent with to-be-issued rules implementing the GENIUS Act’s reserve asset requirements.

- Corporate information: An applicant must submit a description of the potential issuer’s corporate details, including ownership and control structure, organizing documents (which may be in draft form) and a list of proposed directors, officers and shareholders. The application should state whether any of the proposed directors, officers or shareholders have been convicted of certain felonies.

- Policies and Procedures: Copies of key policies and procedures should be provided, including those concerning anti-money laundering compliance, custody and safekeeping of reserve assets, books and records, transaction processing and redemption.

- Accountant engagement letter: An engagement letter with a public accounting firm must be provided to demonstrate the issuer would be ready to meet the GENIUS Act’s requirements, which include monthly disclosures of reserves on each PPSI’s website. Such reports of reserves must be examined by a public accountant.

The proposal notes that, where possible, the FDIC will seek information necessary to evaluate the above factors from its examination staff and existing examination materials. The use of information collected from other sources is intended to ease the burden on applicants.

Remaining open questions about the application process

While the proposal provides additional clarity on a number of issues, certain key questions remain:

- Confidentiality of applications: Presumably, by virtue of their inclusion in 12 CFR Part 303, the FDIC’s proposed regulations would be subject to its standard confidentiality procedures for applications covered by Part 303. The confidentiality regulations of Part 303 state only that applications requiring public comment will by default be made available for public disclosure (application materials are, of course, still potentially subject to a request under the Freedom of Information Act to the extent the content is not exempt and confidential treatment has not been requested). As there is no public comment period provided for in the GENIUS Act or the proposal, PPSI applications should not be made public by default, but the proposal does not explicitly state as much.

- Other agency rulemakings: The OCC and Federal Reserve are also required to issue rulemakings setting out their application processes, and the GENIUS Act requires the agencies to coordinate. The other agencies have not yet released their proposals, so it remains to be seen whether there will be material differences. Acting Comptroller Gould, as an FDIC Board member, voted for the FDIC’s proposed rule, suggesting potential alignment between at least the FDIC and OCC’s processes.

This post is based on the Davis, Polk & Wardwell LLP memorandum, “Federal Reserve and FDIC Take Crypto-Friendly Steps,” dated December 22, 2025, and available here.