A recent OECD report explores key issues and trends in sustainable bond markets, including green bonds and sustainability-linked bonds. It aims to inform policy discussions on investors’ goals when acquiring sustainable bonds, how these instruments may influence corporate and official sector issuers’ decisions, and what can be done to develop the market for sustainable bonds further.

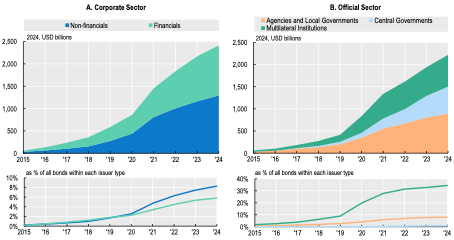

Over the past five years, sustainable bonds have emerged as an increasingly significant source of capital market financing for both corporate issuers and the official sector. As of 2024, the outstanding amount of sustainable bonds in the corporate sector reached $2.4 trillion, accounting for 7% of all outstanding corporate bonds. In the official sector, outstanding sustainable bonds totalled $2.2 trillion, representing 3% of all official sector bonds (Figure 1). Green bonds have been the predominant form of sustainable bond issuance across both sectors throughout the past decade. From 2015 to 2024, Europe played a leading role in this market, accounting for half of all sustainable bond issuance by corporate and official sectors.

Figure 1 Global outstanding sustainable bonds by issuer

Multilateral institutions are the most active issuers of sustainable bonds, with 34% of all outstanding bonds

Source: OECD (2025), Sustainable Bonds: Trends and Policy Recommendations, OECD Publishing, Paris, https://doi.org/10.1787/26726c68-en.

The development of sustainable bond markets to date has been broadly successful. Looking ahead, if the proceeds raised through sustainable bonds are allocated to projects that deliver meaningful environmental and social benefits at relatively low economic cost, both investors and society at large stand to benefit. Realising these benefits, however, depends critically on regulatory frameworks and institutional arrangements that ensure markets function efficiently and that investor interests are adequately protected.

Against this background, the following recommendations aim to inform discussions among policymakers, regulators, and academics to safeguard investor interests while supporting the continued development of the sustainable bond market.

- Regulatory authorities should encourage the interoperability of sustainable bond standards and taxonomies for sustainable activities, with a focus on international comparability and harmonisation between markets.

Sustainable bonds are a recent innovation in debt market, yet their growth has been accompanied by the development of standards and taxonomies. Standards provide rules or guidelines that foster consistency against a benchmark, while taxonomies classify economic activities by providing a common definition of what constitutes a “sustainable” activity.

Regulatory authorities should work with relevant standard-setters to improve the comparability of national, regional and international standards and taxonomies. This should be informed by scientific evidence and broader public policy objectives, while recognising that taxonomies designed primarily for official sector activities may not be readily applicable to corporate issuers, and vice versa. Any regulatory intervention should be guided by a careful assessment of costs and benefits and should prioritise alignment with established international frameworks. In addition, differences in issuer capacity and levels of economic development across jurisdictions should be taken into account. Allowing for flexibility could facilitate broader access to sustainable and transition finance.

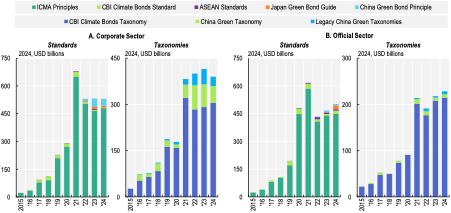

Although the majority of issuers align their bonds with principles developed by the International Capital Market Association (ICMA), a growing number of regional and national standards have emerged recently. Similarly, various taxonomies are used to classify bonds as sustainable (Figure 2).

Figure 2 Sustainable bond issuance following different standards and taxonomies

The ICMA Principles are the most used standard, but local standards have emerged recently

Source: OECD (2025), Sustainable Bonds: Trends and Policy Recommendations, OECD Publishing, Paris, https://doi.org/10.1787/26726c68-en.

- The disclosure of sustainability-related metrics relevant to holders of sustainable bonds should be reliable, consistent, and comparable.

Issuers of sustainable bonds should be required to disclose reliable, consistent and comparable metrics to ensure bondholders can assess whether proceeds have been used in accordance with the bond contract, for use-of-proceeds bonds, and how issuers are performing against sustainability-related targets, for sustainability-linked bonds.

Whenever possible, such disclosure should be prepared in accordance with internationally recognised accounting and disclosure standards, and should be assured by an independent, competent, and qualified attestation service provider.

For use-of-proceeds bonds, investors should have access to transparent information about the environmental or social projects financed by their investments, rather than broader and non-project-driven purposes. Information should be provided on an annual basis. However, less frequent disclosure may be appropriate whenever the costs of data collection and disclosure are excessively high.

Between 2015 and 2024, “clean energy” and “green buildings” represented the primary destinations for the use of proceeds of corporate sustainable bonds, while agencies and local governments and multilateral institutions predominantly directed proceeds toward social expenditures. OECD analysis reveals that, on average, 4% of corporate sustainable issuance and 5% of official sector sustainable issuance allocate proceeds to a “general purpose” category, considering a flat allocation of the disclosed eligible projects. This effectively results in an open investment scope and, thus, implies the absence of a clearly defined sustainability-specific purpose.

- Standard-setters and regulatory authorities may consider the extent to which refinancing concluded projects using the proceeds of green, social and sustainability bonds should be allowed, and if so, what the appropriate disclosure practices should be.

Allowing the proceeds of sustainable bonds to refinance concluded projects creates a distinction between the capital raised through use-of-proceeds bond issuances and the amount the issuer invests in new eligible projects. This distinction may not be evident to many investors, and it may reduce the potential of the sustainable bond market to improve the environmental and social impact of corporate and official sector issuers. One possible mitigation measure could be to recommend that issuers disclose the planned allocation of proceeds between financing of new projects and refinancing of existing projects in the offering documents.

An analysis of a sample of 145 sustainable bonds issued between 2017 and 2024 shows that, among 88 use-of proceeds bonds, three-fourths state in their legal documentation that the refinancing of existing eligible projects with the proceeds is allowed. Nevertheless, the documentation does not estimate the share of financing and refinancing, notwithstanding the recommendations set out in the ICMA Principles. Specifically, no prospectus in the sample mentions explicitly that the proceeds would not be used for refinancing.

- Key service providers, such as second party opinion providers, may warrant treatment comparable to that of external auditors and credit rating agencies.

Requiring a second party opinion on whether the bond is aligned with a specific sustainable bond standard and/or a taxonomy has become a common practice in the sustainable bond market. Independent assessments can improve investors’ ability to compare sustainability-related information and assess the potential sustainable impact of their investments. This can further enhance market transparency and credibility. In 2024, sustainable bonds assured by a second party opinion accounted for 81% of corporate sustainable issuance and 69% of official sector sustainable issuance, a growing trend relative to the past decade (Figure 3).

These service providers play a similar role to external auditors and credit rating agencies and potentially face comparable conflicts of interest. They provide services relevant to the public interest but are hired by the issuers they are meant to provide assurance to, potentially creating a conflict of interest. Specific codes of conduct, regulation or supervision for providers of second party opinions and other forms of assurance for sustainable bonds may be needed.

Figure 3 Sustainable bond issuance with (without) the use of a second party opinion provider

Second party opinions are playing a growing role in assuring sustainable bonds

Source: OECD (2025), Sustainable Bonds: Trends and Policy Recommendations, OECD Publishing, Paris, https://doi.org/10.1787/26726c68-en.

- Institutions setting stewardship codes may consider adopting guidance on institutional investors acquiring sustainability-linked bonds, including the importance of analysing whether they have ambitious sustainability-related performance targets.

Sustainability-linked bonds can serve as an effective instrument to align investors’ sustainability-related preferences with the environmental and societal impact of investee entities.

Analysing the legal documentation of 57 sustainability-linked bonds, all but three issuers in the sample face the same consequence if they do not meet the sustainability performance target(s) set, namely an increase in the annual coupon rate following the predetermined target date. In half of the cases, the step-up in the coupon rate amounts to 25 basis points.

Sustainability-linked bonds with insufficient ambitious targets function de facto as conventional bonds, as they do not influence the issuer’s decision-making process and its consideration of sustainability-related impacts. Therefore, institutional investors may need to undertake their own assessment. In this context, stewardship codes serve as an important complement to regulatory requirements, encouraging institutional investors to monitor and engage with their investee companies.

Caio de Oliveira is the head of the Sustainable Finance and Corporate Governance Team, and Valentina Cociancich is a policy analyst in the Capital Markets and Financial Institutions Division, within the Directorate for Financial and Enterprise Affairs of the Organisation for Economic Co-operation and Development (OECD). This post is based on an OECD report, “The Sustainable Bonds: Trends and Policy Recommendations,” dated November 17, 2025, and available here. The opinions expressed and the arguments employed are those of the authors.