Difficulties in valuing the assets and liabilities of the largest banking organizations aggravated the 2007-08 financial crisis. Regulation under the Dodd-Frank Act sought to increase transparency and reduce complexity among these institutions. With the benefit of significant hindsight, it is informative to explore how the complexity of the largest banking organizations’ balance sheets has changed since the crisis. It turns out that: (1) balance sheets have been substantially simplified, with the portion of complex instruments falling approximately eight times, (2) complex derivatives specifically have declined, but not as quickly as other complex instruments, so that now derivatives contribute proportionately more to balance sheet complexity, and (3) much of the decline occurred before the arrival of post-crisis laws, raising new questions about supervisory efforts and self-regulation following the financial crisis. The decline in complex instruments means that fluctuations in these instruments’ values pose far less risk to capital cushions.

A significant portion of financial instruments that banking organizations hold in their trading book or on an available for-sale basis is subject to recurring fair value accounting. Under Accounting Standards Codification (ASC) 820, this periodic re-valuation of financial instruments requires the firm to divide the instruments among three categories. As JPMorgan’s financial statements explain:

A three-level fair value hierarchy has been established under U.S. GAAP for disclosure of fair value measurements. The fair value hierarchy is based on the observability of inputs to the valuation of an asset or liability as of the measurement date[:]

-

- Level 1 – inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets.

- Level 2 – inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument.

- Level 3 – one or more inputs to the valuation methodology are unobservable and significant to the fair value measurement.[1]

Banking regulation and my own research relies on this categorization. The importance of Level 3 instruments to a banking organization’s balance sheet serves as a proxy for complexity.

The remainder of this post presents and discusses the importance of Level 3 instruments between 2007 and 2024 to the balance sheets of the six largest U.S. banking organizations: Bank of America, Citibank, Goldman Sachs, JP Morgan, Morgan Stanley, and Wells Fargo. These institutions are of central importance to discussions of systemic risk as they represent firms (a) that are too big to fail, and (b) with the greatest sophistication and hence expected involvement with complex instruments.

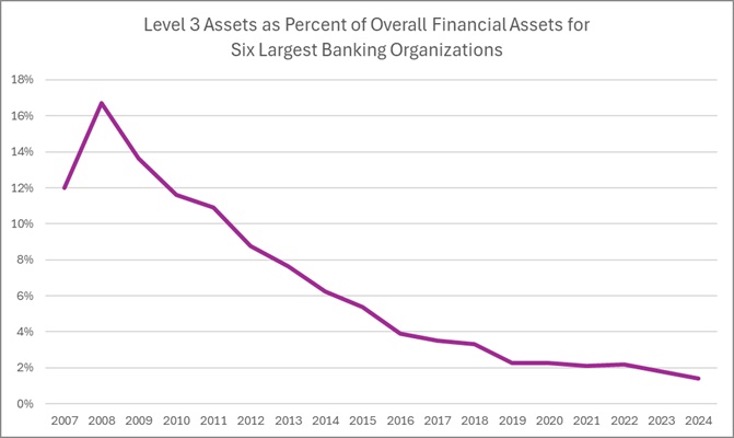

Figure 1

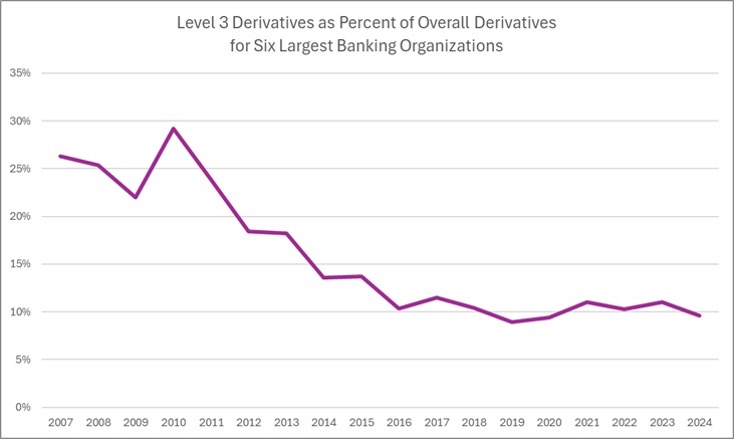

Figure 1 shows the substantial decline of Level 3 assets among assets subject to recurring fair valuation over the time period in question. As reflected in Figure 2, a similar pattern of decline in complexity is observed if focusing exclusively on derivatives. Although figures 1 and 2 aggregate data across the six institutions, individual institutions exhibit consistent trends. As explored in the underlying paper, financial instruments subject to recurring fair valuation (i.e., the denominator) have increased in this period, while Level 3 instruments (i.e., the numerator) have declined.

Figure 2

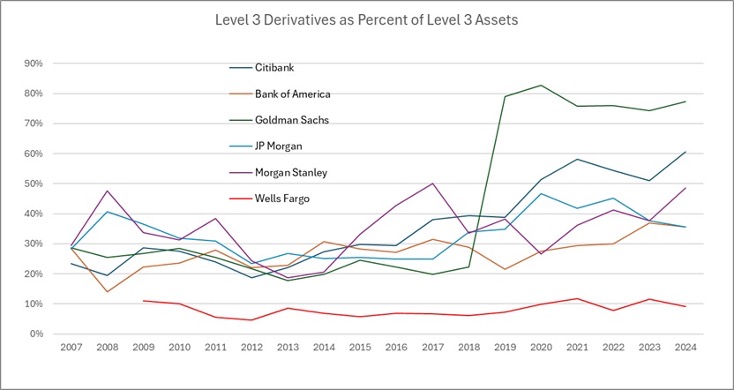

Over the period, derivatives have become an increasing component of overall Level 3 assets as reflected in Figure 3.

Figure 3

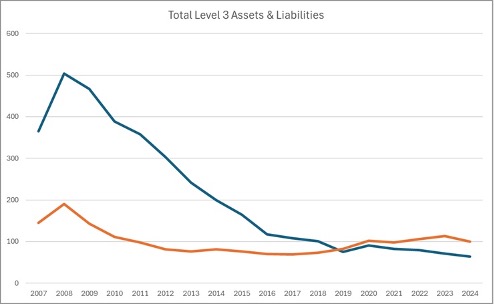

The preceding observations answer some questions and raise others. The valuation of major banking institutions’ balance sheets calls for less judgment during ordinary course operations now than it did during the crisis. A number of post-Dodd Frank Act initiatives sought to reduce complexity. These range from capital standards, to increased regulation of securitization, to comprehensive swap market regulation, to the Volcker Rule. A potentially important component of these interventions is a G-SIB surcharge that, in part, bases higher capital requirements on a measure of complexity tied to the amount of Level 3 assets. The focus on Level 3 assets in calculating extra capital requirements may explain why those assets have fallen more than Level 3 liabilities among the six institutions, as reflected in Figure 4. Figure 4 presents assets in blue and liabilities in orange, with the y axis in billions USD.

Figure 4

If focusing on just Level 3 derivatives, the trends are similar, albeit liabilities come to exceed assets earlier, around 2013.[2]

As already noted, there has been growth in Level 1 and Level 2 instruments while use of Level 3 instruments shrunk. This may be due to genuine changes in operations or due to reclassification of Level 3 instruments to lower levels. Any reclassification would be due to either exploitation of accounting methodology (e.g., chicanery) or the emergence of new data sources that permit valuation of previously Level 3 instruments based on more observable inputs. For example, some of the derivative-market reform provides for public dissemination of swap data including pricing data; this can provide more objective grounds for valuation of instruments, moving them from Level 3 to lower levels. Beyond reclassification, some of the changes may be due to persistent changes in the values of various instruments. It may be that over the period, some substantial subset of Level 3 instruments has declined in value.

Other explanations for the decline relate to genuine decreases in Level 3 instrument-related activity. Banking organizations may no longer provide the services that generate Level 3 instruments. This may reflect shrinking markets or a shift in the provision of those services to non-banking organizations (i.e., shadow banks). If there is an absolute decline in activity, that is not necessarily concerning. Only if the Level 3 instruments were socially useful should the decline raise concerns. On the other hand, a shift in the activities to the shadow-banking sector may be troubling if those activities benefit from regulation. For example, some Level 3 loans may have transitioned from banking organizations to private lenders where they implicate insurance company reserves.[3]

A major puzzle the trends pose is why the decline in Level 3 assets began well before the onset of regulatory interventions. As far as I have been able to determine, no relevant Dodd-Frank Act regulatory changes took effect earlier than the end of 2012. And yet significant declines in Level 3 assets preceded that period. Several non-exclusive hypotheses may explain the decline in the pre-regulation period.

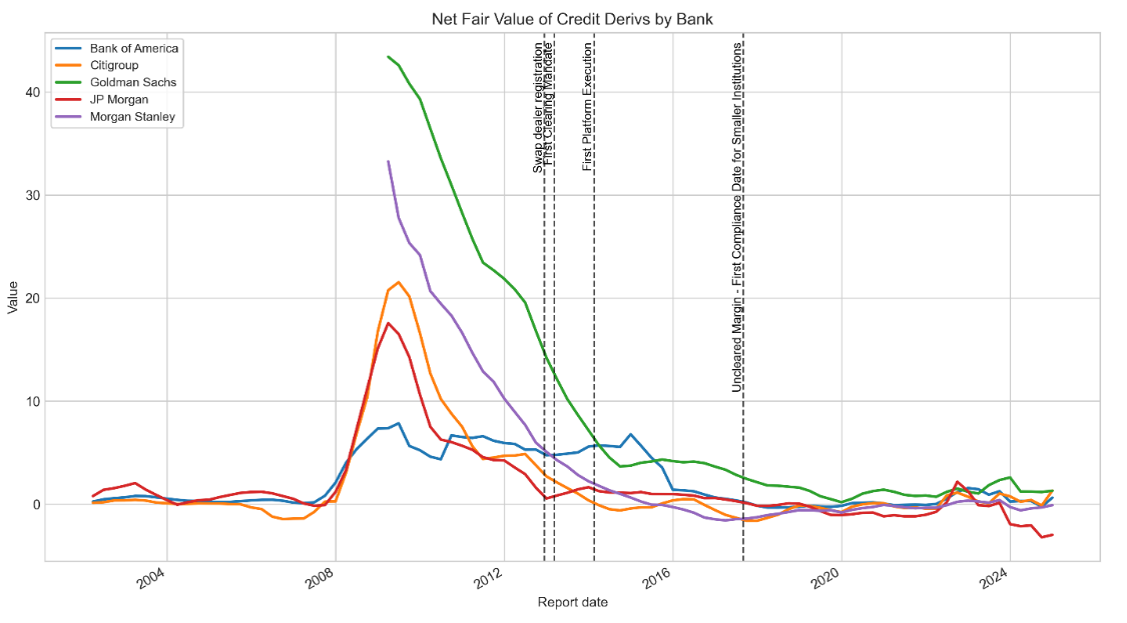

First, the banking regulators may have had substantial authority under preexisting law to encourage simplification. Through supervisory efforts starting around 2008, banking regulators may have pressured financial institutions to shed complex assets and operations. There is an important gap in our understanding of the financial crisis when it comes to understanding what financial regulators could have done ex ante and what they did do ex post as supervisors rather than as providers of financing and as resolution authorities. These efforts may explain, among other things, the precipitous drop in the value of credit derivatives held by the top five banking organizations well before the onset of derivatives regulation, as reflected in Figure 5.[4]

Figure 5

Second, financial institutions themselves may have initiated efforts to simplify. Pressure could have come internally or from shareholders. The crisis forced high level executives to take responsibility for operations involving hard to value instruments such as re-securitizations and certain credit default swaps, potentially prompting a rethink and lower tolerance for complexity. As an example of activity that was likely related to changing risk tolerance within institutions, some banking organizations sold off illiquid interests in hedge funds and other private funds before the Dodd-Frank Act passed and others sold off after enactment but before the multi-agency promulgation of the Volcker Rule.

Third, certain financial markets (e.g., asset backed securities) significantly declined after the financial crisis. As overall market supply (or demand) for instruments declined, banking organizations came to hold less of them.

* * *

The Dodd Frank Act was drafted against the backdrop of a banking industry that was already being reshaped by efforts to simplify. This implicates longstanding questions about the public-private dialectics of regulation and resistance to regulation. Supervisory or private efforts prepared the ground for a number of Dodd-Frank Act interventions, potentially both softening industry resistance and signaling industry receptivity to limitations on banking activity. I am deeply interested in the question of where law comes from, and the simplification of balance sheets before the onset of new regulation may illuminate how industry helps shape regulation rather than having regulation simply be imposed on it.

ENDNOTES

[1] JPMorgan Annual Report for 2024 at 182.

[2] Notably, this is not cause for alarm. First, non-Level 3 assets can support Level 3 liabilities. Second, Level 3 liabilities could come to exceed Level 3 assets if the latter are subject to heightened collateralization, reducing the value of Level 3 exposure. The posting of collateral to major banking institutions reduces both their credit exposure to counterparties and their Level 3 asset values.

[3] James Politi, Eric Platt and Sujeet Indap, US Treasury Calls in Regulators for Talks on Private Credit Risks, Financial Times (April 1, 2026).

[4] Goldman Sachs and Morgan Stanley became bank holding companies in response to the crisis, so their data (drawn from Fed FRY9 repots) start later.

Ilya Beylin is an associate professor at Seton Hall Law School. This post is based on his recent paper, “How Banking Institutions Have Become More Transparent After the Financial Crisis,” forthcoming in the Review of Banking and Financial Law and available here.