Capital markets work is among the most profitable areas of transactional legal practice, and it is typically awarded to lawyers within a tight network. Perhaps the most elite of those lawyers advise securities issuers and underwriters on IPOs. They are usually repeat players who earn substantial fees while developing deep expertise, high-profile reputations, and professional relationships that grow over the course of their careers. Women have long reported that they have limited access to these professional relationships and, as a result, miss out on opportunities to develop business and advance their own careers – even though they make up about half of all associates, and a quarter of equity partners at large law firms.

In a new article, we present the first empirical study of the gender gap within the network of lawyers who lead IPO advisory work (the “IPO Attorney Network). Analyzing thousands of lawyers across 8,358 IPOs from 2000-2021, we document the persistent and systemic exclusion of women from one of the most lucrative and influential corners of legal practice.

We analyze the IPO Attorney Network from the perspective of social network analysis—a method long established in the social sciences but still novel in legal scholarship. Drawing on prior work by two of us, we argue that the number and quality of an attorney’s connections offer a concrete measure of access to information, mentorship, and influence; a deficit of links reflects a deficit of opportunity. Network analysis allows us to capture not merely how many women participate, but where they sit within the web of relationships that drives the field.

Data and Methods

We built a dataset of every IPO in the United States from January 2000 through December 2021 and hand-collected information from the Forms S-1 filed in the SEC’s EDGAR system—capturing the issuing company, the law firms and individual lawyers advising issuers and underwriters, in-house general counsel, and office locations. The result is a corpus of 8,358 filings and 5,905 distinct attorneys. We inferred a professional relationship between any two individuals who appeared together on the same S-1, and estimated gender using an established gender-inference tool, reporting all results in anonymous form. Alongside simple participation counts, we measured each attorney’s position with standard network metrics. The study is deliberatively descriptive: It maps the gap and its contours, leaving causal inference to later work.

Findings

Our study finds a persistent gender gap in the IPO Attorney Network and suggests that the network itself helps reproduce women’s exclusion from positions of influence at elite firms.

First, the gender gap is large and strikingly persistent. Across the full network, just 18.56% of attorneys are women. The average proportion of women advising on IPOs hovered around 19% over the same period and, remarkably, was essentially the same in 2021 as in 2000. The high-water mark came early, in 2002, at roughly 20%; by 2021, women were only about 15% of the network. That stagnation is notable given that the share of women partners at law firms rose nearly 10 percentage points over the same years. The centrality data tells the same story: Over time, far more men than women become the highly connected lawyers at the network’s core.

Second, the gap differs by the type of IPO. IPOs of Special Purpose Acquisition Companies (SPACs)—a form of legal innovation that boomed in 2020-21 and received heavy criticism over conflicts of interest, inflated valuations, and weak investor protection—drew even fewer women. In 2021, women were just 11% of the lawyers advising on SPAC transactions, compared with 20% on traditional IPOs. The underrepresentation of women in a higher-risk and arguably less salutary form of innovation echoes prior research on gender and risk-taking.

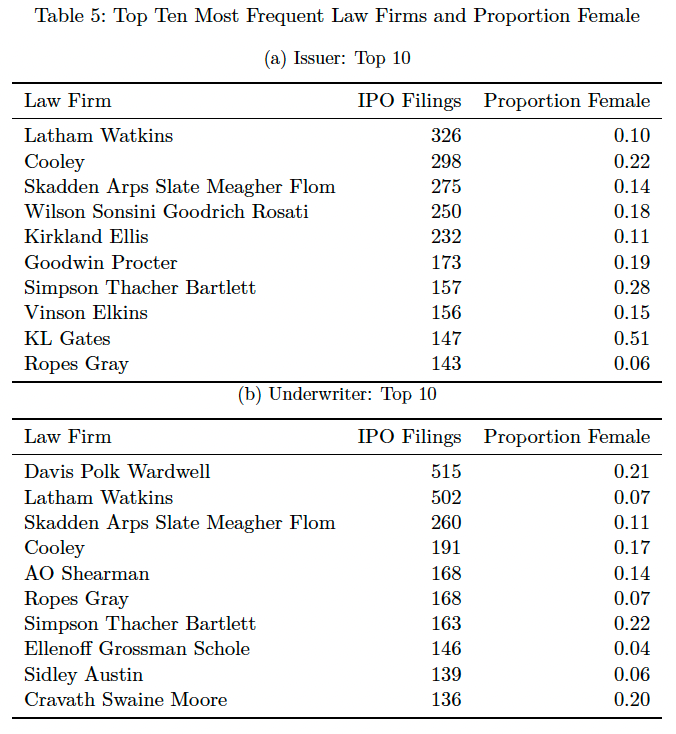

Third, representation differs sharply by law firm and by side of the deal that the law firm represents. Firms advising issuers had a female proportion of 16%; those advising underwriters, 12%. The variation among elite firms is striking. Among the top issuer-side firms, K&L Gates’ IPO teams were 51% women, Simpson Thacher’s 28%, and Cooley’s 22%, while Ropes & Gray stood at just 6%. Among top underwriter-side firms, Simpson Thacher (22%), Davis Polk (21%), and Cravath (20%) led, while Sidley Austin trailed at 6%. The gap is pronounced at some of the most elite firms. For example, only 10% of Latham & Watkins’ issuer-side IPO lawyers, and 7% of its underwriter-side lawyers, are women. These differences suggest that firm- and team-level norms, cultures, and hiring pipelines matter.

Fourth, female general counsel did not move the needle. Women’s participation in the general counsel offices of issuers was as high as, or higher than, among issuer’s counsel—yet we found no evidence that the presence of women general counsel predicted greater female participation on the advisory teams.

Fifth, geography matters—at least on the issuer side. IPO practice is heavily concentrated at firms on the coasts, and the proportion of women rises when deals are handled at other firms. Between the two dominant markets, New York teams advising issuers had significantly lower female representation than their California counterparts; for underwriter-side teams, we found no significant geographic difference.

Sixth, women fall behind in network resources as their careers progress. Tracking the most connected attorneys over time, we found that men’s personal connections, the connectedness of their professional “neighbors,” and the share of women in their networks all grew at more than twice the rate seen for women. Among the 50 most central attorneys in the network, women remained a small fraction of those individuals’ connections. Measured by degree centrality (a count of how many connections an attorney has), the share of women crept only from 16% in 2000 to 18% in 2021, and by eigenvector centrality (a spectral measure that captures the extent to which an attorney is linked to highly connected attorneys) it actually declined slightly. The low proportion of women in the subnetworks of highly connected attorneys reveals a key challenge for greater gender equality in transactional practice. This matters because junior lawyers typically gain entry when a highly connected attorney brings them into the circle—and highly connected lawyers simply do not have many women in their networks to bring along.

Implications

Our findings arrive amid intensifying attacks on diversity and inclusion efforts at law firms, and we argue that our study has important implications as law firms assess their strategies for creating opportunities for all lawyers. On one hand, the sheer durability of the gap—through two decades in which women neared half of all law students and associates—raises hard questions about whether familiar approaches like recruitment programs, diversity training, and affinity groups have meaningfully changed elite transactional practice. On the other hand, the slow progress that did occur counsels strongly against abandoning these efforts: Doing so risks widening, not closing, the gap.

The network perspective also points toward more structural, less identity-based reforms. The first targets what Nobel laureate Claudia Goldin calls “greedy” work—the long, inflexible, and unpredictable hours that command outsized rewards and disproportionately push out those with caregiving responsibilities. Substitutable staffing models, required paid family leave, and durable flexibility of the kind firms briefly embraced during the pandemic could ease those penalties. The second is mentorship and sponsorship that reaches women. Firms too often rely on “natural” relationships that leave women and lawyers of color behind or relegate mentoring itself to the uncompensated “office work” disproportionately shouldered by women. Because cross-gender mentoring benefits mentees, mentors, and firms alike, we urge engaging all leaders and holding them accountable, including through structured work allocation and deliberate succession planning, rather than relying on identity-based programming alone.

Above all, our study underscores the need for transparency. The gap we document has until now gone largely unmeasured and undisclosed, obscured by firms’ broad and unquantifiable commitments to diversity. Meaningful disclosure would let clients, recruits, and firm leaders themselves measure progress rather than rely on rhetoric.

Afra Afsharipour is the John D. Ayer Professor of Law at the University of California, Davis, School of Law. Kristina Bishop is a research economist at the Kem C. Gardner Policy Institute of the University of Utah. Matthew Jennejohn is the Rulon and Marion Earl Professor of Law at Brigham Young University’s J. Reuben Clark Law School. This post is based on their article, “The IPO Gender Gap,” available here.