Assurance providers, a type of green gatekeeper, certify the accuracy of sustainability information. In a new paper, we analyze the market for assurance services, asking whether they should be regulated and, if so, how.

Assurance providers do with sustainability-related claims what public accounting firms have long done with financial statements: certify the accuracy of claims by public companies. Assurance providers promise to reduce the information asymmetry between issuers of claims and their recipients. For our purposes, these recipients are investors in companies making sustainability claims.

Sustainability Disclosures

Public companies in the United States and the European Union are increasingly providing sustainability disclosures, whether to meet legal requirements or voluntarily. While both U.S. and EU legal systems mandate sustainability disclosures, they take markedly different approaches. Under U.S. securities laws, public companies may be required to disclose sustainability information when necessary to comply with broader disclosure requirements, even though these requirements do not specifically mention sustainability, or to prevent their other statements from being misleading. Beyond these general requirements, and given the stay of the SEC Climate Rule, public companies face few sustainability disclosure mandates.

In contrast, EU law mandates itemized sustainability disclosures. Under EU directives, including the recently adopted Corporate Sustainability Reporting Directive, disclosures are subject to the double materiality test: Undertakings must disclose not only sustainability matters material to themselves financially (financial materiality), but also those that have a material impact on people, the environment, and third parties (impact materiality). In insisting on both notions of materiality, the EU goes beyond SEC mandates, which focus on financial materiality.

Accordingly, investors are likely to see different sustainability information from U.S. and EU companies, hampering comparability. Even within each of the two systems, disclosures are often hard to compare. Heterogeneity of sustainability information is of particular concern in the United States, which has nothing equivalent to the European Sustainability Reporting Standards.

Assurance

Assurance is a familiar topic in legal scholarship because it is critical to the work of public accountants. In particular, auditing financial statements is a form of assurance. Strictly speaking, assurance is a form of third-party verification, but verification need not result in assurance.

A strong parallel can be drawn between sustainability assurance and financial auditing, but key differences remain. Most importantly, the sustainability assurance industry is in its nascent stages, whereas financial-audit services have existed since the 1800s. While financial audits follow established protocols, recent scholarship observes that sustainability assurance practices are heterogeneous and in flux. In the United States at least, sustainability assurance practices vary widely, including as to what sustainability information is assured, assurance standards used, and the level of assurance provided—a contrast to the homogeneous practices of financial statement auditing. This variation in practices may stem from the absence of generally accepted assurance standards—uniform procedures that assurance providers are meant to follow before certifying sustainability disclosures—and from heterogeneity in the very nature of assurance providers. Whereas financial auditing is uniformly provided by public accounting firms, in the United States, engineering, consulting, and non-public accounting firms perform roughly 80% of sustainability assurance for S&P 500 companies. It may come as no surprise, then, that sustainability assurance has yielded less reliable assurance than has financial auditing.

The EU Corporate Sustainability Reporting Directive, in contrast, mandates uniform standards. All mandatory sustainability reporting by EU-based undertakings must be accompanied by an assurance opinion from a statutory auditor, an audit firm, or, if permitted by a member state, an independent assurance services provider. And that opinion is subject to detailed standards. In turn, assurance providers are subject to various conduct regulations meant to ensure their comportment with the uniform standards.

The Role of Reputation and Regulation

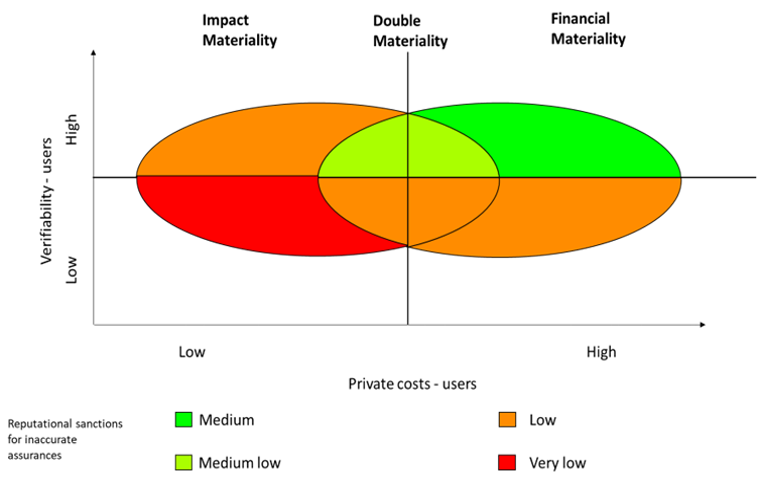

Assurance providers’ reputation constraints might ensure the accuracy of their assurance. Yet, these constraints are likely weaker than those facing traditional gatekeepers. Drawing on our earlier work, Green Gatekeepers, we provide three reasons. First, assurance providers’ assurances may “work” even when they are inaccurate. Assurances enable environmentally conscious investors to feel virtuous from having made a sustainable investment decision, so long as they do not learn that an assurance is inaccurate. Second, even environmentally conscious investors are often unable to identify inaccurate sustainability assurances due to the complexity of the issues underlying them. Third, even investors who genuinely care about the accuracy of green claims often face limited or no private costs when they accept inaccurate assurance. That is, when a disclosure is impact material but not financially material, investors incur no private costs where assurances are inaccurate.

Taking account of both the private costs borne by investors and their incentives/ability to verify sustainability claims, we map how the effects of reputation constraint will vary, as shown in the figure below. We suggest that, where verification by users is difficult or users incur minimal private costs from unknowingly relying on inaccurate assurances, the reputational sanctions faced by assurers are likely to be low. By contrast, reputational mechanisms are likely to operate more intensely where assurances that are financially material and can easily be verified by users.

We conclude that, for the three reasons indicated above, reputation constraints may fail to induce sustainability providers to issue accurate assurances.

We next consider the force of direct or primary regulation on firms, which complements reputational constraints. Under U.S. law, claims under federal securities law for false sustainability disclosures face impediments, such as both scienter and materiality requirements. In short, we suggest that these forces are likely ineffective in deterring inaccurate sustainability information.

Against this background, we consider the shape that regulatory intervention might take. We argue that, other things being equal, the appropriate policy mix should depend on two factors: first, the significance of private costs for users relying on inaccurate gatekeeper assurances and second, the extent to which policymakers and courts can verify these assurances, a factor in turn depending on the complexity of the methodologies underlying the assurances.Applying this framework, we comment on the merits of several policy interventions, including ex ante regulation, ex post liability, regulatory licenses, incentives for assurance providers that operate as non-profits, and transparency requirements.

Luca Enriques is a professor of business law at Bocconi University, Alessandro Romano is an associate professor of business law at Bocconi University, and Andrew Tuch is a professor of law at Washington University in Saint Louis. This post is based on their recent article, “Sustainability Assurance,” published in a symposium issue of Law and Contemporary Problems and available here. A version of this post appeared in the Oxford Business Law Blog.