Sky Blog

Sky Blog

Entrepreneurship—a process of organizing, managing, and assuming the risks of a business or enterprise—has long been viewed as important for sustained economic activity. But the state of the economy, especially booms and downturns referred to business cycles, can itself affect entrepreneurship. A better understanding of the nexus between the two can, therefore, help improve public policy towards entrepreneurship and generate benefits for society.

A key challenge for the analysis is that entrepreneurship cannot be easily captured by a single measure. One could, for example, use business ownership as a measure but it does not distinguish between growth-oriented highly innovative activity that typically generates little revenues initially from those that are based on existing products and services. Another possibility is to use self-employment as the measure. Again, a limitation here is that it may not adequately include innovative entrepreneurs.

We consider a novel alternative measure of entrepreneurship, venture capital (VC) invested, which has several advantages and sheds new light on the nexus between entrepreneurship and economic activity. VC funds are an important financial intermediary, since VC supports risky entrepreneurial activity that otherwise could not have been financed by traditional financial institutions, such as banks. Moreover, because it encourages high risk high return entrepreneurial activity, it can be considered to have a disproportional impact on technology and innovation, as well as employment and economic growth. Venture capital is provided by both financial firms (most prominently, venture capital funds) and non-financial firms seeking relationships with emerging businesses in their industry for strategic purposes. Notable examples of strategic (as opposed to financial) sources of VC exist in almost every industry; Google, Medtronic and Home Depot are some of the major companies that have a venture capital arm.

We measure entrepreneurship using quarterly VC data for the U.S. from 1990 to 2014. Specifically, there are two key components to the data: first, the number of new VC-funded business formations representing entrepreneurial entry (the seed and start-up stage), and second, the number of successful exits from the VC stage in the form of IPOs and acquisitions. VC exit represents the late and mature stage of entrepreneurial activity.

Our entrepreneurship measure covers the entire population of VC funded companies (more than 100,000 data observations) in the U.S. over the past 25 years. This period includes three National Bureau of Economic Research (NBER)-dated recessions. Due to some distinct characteristics and barriers in the VC industry, these VC-funded companies are generally engaged in innovation, and are less likely to include small businesses engaged in providing well established products or services. Finally, our measure applies to both the aggregate U.S. economy, and important VC-funded sectors. Despite the well-known volatility due to the high risk-high return nature of VC activity, venture capital remains an important source of funding for entrepreneurs engaging in innovative activity in the information technology, medical/health and life sciences sectors.

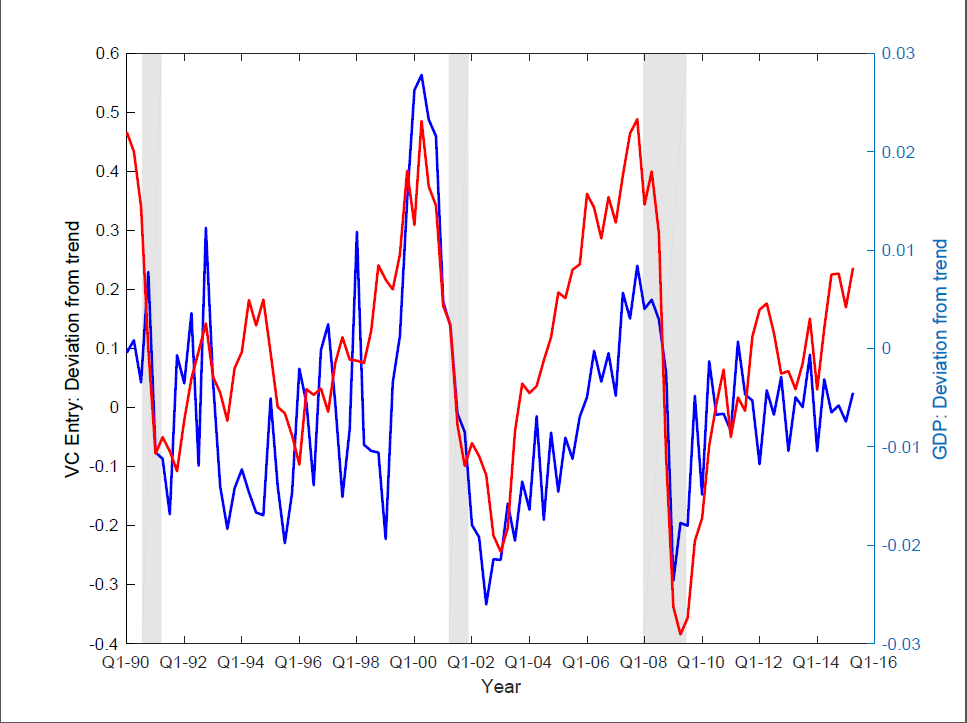

We find that entrepreneurship, as captured by VC entry and exit, is procyclical. That is, both VC entry and exit tend to increase during an economic expansion when output is above its long-run trend and decrease during a recession when output is below the trend. Output is measured as real Gross Domestic Product (GDP). VC entry has a strong contemporaneous correlation of 0.6 with cyclical GDP. Figure 1 shows the cyclical pattern between the VC entry and cyclical GDP, with the grey-shaded columns representing the last three NBER-dated recessions in the U.S. economy. During recessions, both VC-entry and economic activity decline sharply, and then bounce back together. We confirm using statistical tools that VC entry helps predict future GDP, and vice versa. The interpretation is that there is strong interaction between entrepreneurship as measured by VC entry and economic activity.

Figure 1: VC Entry (blue line) and the U.S. Business Cycle (red line)

Figure 1: VC Entry (blue line) and the U.S. Business Cycle (red line)

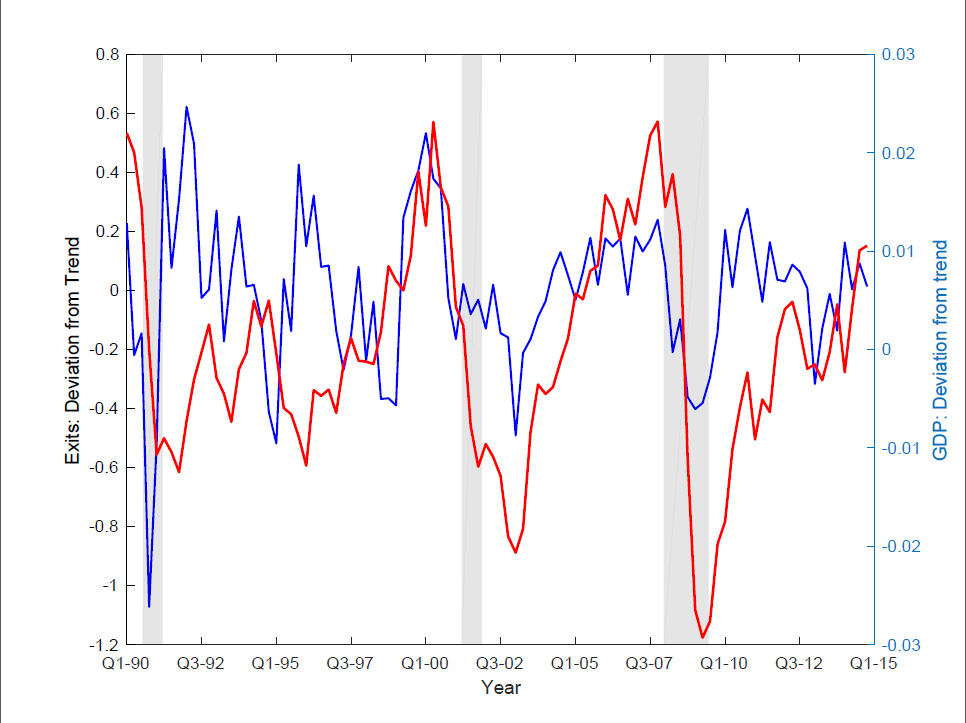

VC exit, however, is less procyclical with a correlation of 0.26. Figure 2 shows the pattern between VC exit and cyclical GDP. Although both VC exit and economic activity decline sharply around recessions, the patterns differ during the recovery phase. Another important point is that VC exit lags the U.S. business cycle by two quarters. That is, when GDP is above trend, it takes two quarters for VC exit to rise above its trend.

Another aspect revealed in the both figures is that VC activity appears to be quite variable compared to cyclical GDP. This is evident from the choppier blue lines relative to the red lines in Figures 1 and 2. To put in perspective, business investment in the U.S. is more volatile than GDP, and VC activity is three to five times more volatile than business investment.

Figure 2: VC Exit (blue line) and the U.S. Business Cycle (red line)

Given the importance of VC activity in the creation of major enterprises and innovation, there is much attention paid to it from a public policy perspective. One concern is that recessions may lead to a decrease in innovation oriented entrepreneurial activity that may have detrimental effects on the economy, and could potentially delay the subsequent recovery. The role of public policy can be helpful in this context. For example, government policies such as as tax credits and government-sponsored VC can provide liquidity and augment private VC during recessions, and possibly (dampen the volatility) reduce financial distress and bankruptcies in VC (activity). Our findings suggest that taking into account the cyclicality of VC activity in designing policies aimed at supporting entrepreneurship could be beneficial for the society.

The post comes to us from Hashmat Khan, Full Professor in the Department of Economics at Carleton University and Pythagoras Petratos, Lecturer in Finance at Saïd Business School, Oxford University. The post is based on their paper, which is entitled “Entrepreneurship and the Business Cycle: Stylized Facts from U.S. Venture Capital Activity” and available here.