Sky Blog

Sky Blog

My first few weeks at the Securities and Exchange Commission have been a whirlwind—and just to be clear, I am not talking about the markets.[1] In a few short weeks, I have gotten a crash course on SEC policymaking—and enough reading to empathize with my former law students, who used to tell me, to my puzzlement, that my Corporate Law syllabus was not exactly beach material.

But in between the policy memos that come across my desk, I’ve also had the pleasure of working with my new colleagues on the SEC’s Staff. They’ve taught me a lot in a short time, and I’m grateful for their insights and assistance. The hard work and dedication of these folks gives me confidence that we are up to the challenge of making sure our financial markets are the safest, strongest, and most efficient in the world.

So the first few months of 2018 have been quite a blur. Fortunately, they have not been as stressful for me as the last few months of 2017.

You see, last fall, I took part in two of the most nerve-wracking Q&A sessions of my life. In late October, I had the ultimate job interview: a two-hour, televised confirmation hearing in front of the Senate Banking Committee.[2] Then, two months later, I found myself the one posing the life-changing questions. I asked my girlfriend Bryana to marry me.

I’m happy to report that, to my surprise, both Bryana and the Senate offered a resounding yes—literally within 24 hours of each other. But, let me just say, I now have newfound respect for the staff and Senators on the Committee. I only had to ask one question, and it nearly gave me a heart attack.

Now, as a newly engaged guy, I fully embrace the notion that a strong marriage must be built on a foundation of eternal trust. But today, I would like to ask whether it is wise to apply that standard to corporate governance. Should our public investors have to place eternal trust in corporate insiders? That is, should so-called perpetual dual-class stock ownership structures, which grant corporate executives control of our public companies literally forever, be acceptable?

Before I get started, let me just note that the views I express here are my own and do not reflect the views of the Commission. (Although, I’ll confess, I hope someday that they do.)

The Law and Legacy of Dual-Class Stock

As you know, “dual class” voting typically involves capitalization structures that contain two or more classes of shares—one of which has significantly more voting power than the other. That’s distinct from the more common single-class structure, which gives shareholders equal equity and voting power. In a dual-class structure, public shareholders receive shares with one vote per share, while insiders receive shares that empower them with multiple votes. And some firms have recently issued shares that give ordinary public investors no vote at all.[3]

For most of the modern history of American equity markets, the New York Stock Exchange did not list companies with dual-class voting. That’s because the Exchange’s commitment to corporate democracy and accountability dates back to before the Great Depression.[4] But in the midst of the takeover battles of the 1980s, corporate insiders “who saw their firms as being vulnerable to takeovers began lobbying [the exchanges] to liberalize their rules on shareholder voting rights.”[5] Facing pressure from corporate management and fellow exchanges, the NYSE reversed course, and today permits firms to go public with structures that were once prohibited.[6]

As you all know well, more and more companies choose today to go public with dual-class. Public companies using dual-class are today worth more than $5 trillion, and more than 14% of the 133 companies that listed on U.S. exchanges in 2015 have dual-class voting.[7] That compares with 12% of firms that listed on U.S. exchanges in 2014, and just 1% in 2005. [8]

There’s a long-running debate on dual-class. On one hand, you have visionary founders who want to retain control while gaining access to our public markets. On the other, you have a structure that undermines accountability: management can outvote ordinary investors on virtually anything.

There is reason to think that, at least for a defined period of time early in a company’s life, dual-class can be beneficial. The structure can allow entrepreneurs to build for the long term—and even transform entire industries—without being subject to short-term pressure.[9] When many managers are at the mercy of daily stock-market pressure, dual-class can help America’s most innovative companies create the sustainable long-term value we need to grow our economy.[10]

Many have argued forcefully, however, that one-share, one-vote should be the rule for all public corporations.[11] Whatever the benefits may be of permitting dual-class in a few well-known cases, these advocates argue, the costs for investors—who are left with no way to hold management’s feet to the fire while dual-class is in place—outweigh those benefits.

But the question I want to ask today is not whether dual-class ownership is always good or bad. It’s whether dual-class structures, once adopted, should last forever. Do Main Street investors in our public markets benefit when corporate insiders maintain outsized control in perpetuity?

This is not an academic exercise. You see, nearly half of the companies who went public with dual-class over the last 15 years gave corporate insiders outsized voting rights in perpetuity. Those companies are asking shareholders to trust management’s business judgment—not just for five years, or 10 years, or even 50 years. Forever.

Corporate Royalty and Our Values

So perpetual dual-class ownership—forever shares—don’t just ask investors to trust a visionary founder. It asks them to trust that founder’s kids. And their kids’ kids. And their grandkid’s kids. (Some of whom may, or may not, be visionaries.) It raises the prospect that control over our public companies, and ultimately of Main Street’s retirement savings, will be forever held by a small, elite group of corporate insiders—who will pass that power down to their heirs.

I cannot see how to square that with our nation’s foundational ideas.[12] In America, we don’t inherit power, and we don’t hold power forever. We fought a war against that system, and the good guys won. That’s why, following Thomas Jefferson’s lead in Virginia, after Independence, state governments “laid axe to the root of pseudo-aristocracy,” as Jefferson put it, by abolishing the laws of entail and primogeniture.[13] It’s why our Constitution gives our legislature the broad authority to promote the general welfare, but carefully enumerated what Congress cannot do: grant titles of nobility.[14] It’s why our founders rejected a permanent dual-class legislature: a House of Lords for the royalty and a House of Commons for Main Street.[15]

Now, our public markets aren’t our government, but our country’s spirit of democratic accountability has long animated how we think about economics. That’s why Adam Smith worried in his early writings about how economic models could account for the possibility that power could be wielded by royalty from beyond the grave.[16] And that’s why today we require companies to give investors regular updates on their performance. If you run a public company in America, you’re supposed to be held accountable for your work—maybe not today, maybe not tomorrow, but someday.[17]

So one problem with perpetual dual-class is it removes entrenched managers—and their kids, and their kids’ kids—from the discipline of the market forever. Simply put: asking investors to put eternal trust in corporate royalty is antithetical to our values as Americans.[18]

Perpetual Dual-Class Stock and Corporate Performance

It’s not just that perpetual dual-class stock ownership is disconcerting in principle. The data suggest that it is troubling in practice. And I know this because my staff and I ran the numbers. More on that in a moment.

But let’s start with what existing research in this area can already tell us. One recent study shows that the costs and benefits of dual-class structures evolve over a company’s lifetime.[19] Shortly after the IPO, dual-class firms trade at a premium—but, as the company matures, this premium eventually disappears. Early in a company’s life, then, giving control to the firm’s visionary founders makes sense—but at some point that structure is no longer beneficial.

For that reason, some argue that dual-class firms should include some limit on the amount of time before ordinary shareholders can weigh in on whether dual-class still makes sense for the company.[20] Whether a fixed term of years or upon a founder’s passing, at that point, sometimes called a “sunset,” shareholders get to have their say.

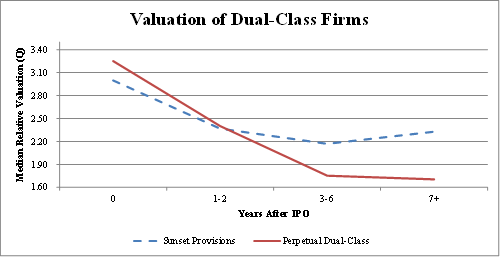

To explore these questions, my staff and I took a close look at 157 dual-class IPOs that have occurred over the past 15 years. We immediately noticed some pretty significant differences between the 71 dual-class companies with sunset provisions and the 86 who gave insiders control forever. Our regression models predicted relatively similar valuations at their IPO dates, a trend that continued for two years after the IPO. But over time, their predicted valuations diverged:

Seven or more years out from their IPOs, firms with perpetual dual-class stock trade at a significant discount[21] to those with sunset provisions.[22] We also found that, among the small subset of firms that decided to drop their dual-class structures later in their life cycles, those decisions were associated with a significant increase in valuations.[23] To be sure, our analysis is preliminary, and this is a subject that deserves much further study. In the spirit of a robust debate, I am making public the results of our analysis as well as our underlying data and assumptions.[24]

The Path Ahead

I’m not the only one concerned about dual-class stock and its effects on our markets. Investors have loudly and clearly registered their objections to this structure, both through the SEC’s Investor Advisory Committee and the Council of Institutional Investors.[25]

As a result of that engagement, three major providers have moved to exclude dual-class companies from significant stock indexes. FTSE Russell will exclude all companies whose free float constitutes less than 5% of total voting power;[26] S&P Dow Jones will, going forward, exclude all dual-class firms;[27] and MSCI will reduce the weight that dual-class firms occupy in its indexes.[28]

Investors, facing a wave of companies using dual-class to insulate their managers from accountability, have every right to bring those complaints to index providers. And there’s no doubt about it: the indices’ decisions sent a loud message to the markets.[29] But excluding all dual-class firms from our major market indices is a blunt tool. And it’s one I’m deeply worried about.

Let me explain why. We face a growing gap in this country between our markets and Main Street investors. The middle class watches our markets rise and increasingly—and correctly—senses that they are left out, that the benefits of that growth are accruing to someone else. And middle class investors often own stock in American public companies through an index. Though their holdings may be small, those holdings reflect their participation in our economic future.[30]

If we ban all dual-class companies from our major indices, Main Street investors may lose out on the chance to be a part of the growth of our most innovative companies. The next Google or the next Facebook will deliver spectacular returns, but average Americans will, quite literally, not be invested in their growth. No one here in Silicon Valley should want to leave average Americans out of their growth story. And investors should not be forced to choose being long American innovation and signing up for corporate royalty.

That’s why I hope that our national securities exchanges will soon consider proposed listing standards addressing the use of perpetual dual-class stock. Such standards would allow Main Street investors to share in our economy’s growth—but avoid asking them to trust corporate management forever. Companies would still be able to IPO with dual-class voting arrangements—but only if management is willing to someday give shareholders their say.[31] And while cynics may say that companies will flee abroad to list, I think it’s pretty unlikely that we’ll see a mass exodus of listings away from the deepest, most liquid capital markets in the world just so founders’ children can inherit and run America’s public companies.

* * * * *

While it is fair to ask people to place their eternal trust in their partner, our country’s founding principles and our corporate law counsel against the creation of corporate royalty. The solution to that problem is not to leave ordinary Americans out of the growth that all of you here in Silicon Valley are creating. The solution is to return to the tradition of accountability that has served our nation and our markets so well.

As a Commissioner, my job is to pursue a three-part mission at the SEC: protect investors, maintain fair and efficient markets, and facilitate capital formation. All three would be advanced if the exchanges promptly pursue this issue. By giving investors more say in the governance of their companies, we can help protect them from managers who would misuse dual-class to extract value rather than build it. By providing clear rules of the game for both shareholders and management, we help them understand and price the risks they’re taking. And by giving visionary founders the space to control their companies soon after their IPO, we encourage them to use our public markets—and share their growth with Main Street investors.

The exact form that exchange standards might take—and the best way to “sunset,” or limit, dual-class structures—is beyond the scope of my talk today. And besides, I have no doubt that the folks in this room can come up with innovative ways to solve that problem.[32] I know that all of you share my goal of finding a way to allow today’s visionaries to access our public markets in a way consistent with our values. And I urge you all to get to work, alongside our exchanges, to make sure that Main Street investors share in the future you’re shaping here every day.

ENDNOTES

[1] I am deeply grateful to my colleagues Matthew Cain, Caroline Crenshaw, Marc Francis, Satyam Khanna, and Prashant Yerramalli, whose invaluable insights have deepened my thinking on these matters a great deal. Responsibility for any errors or omissions is mine alone.

[2] To be fair, I’m using the phrase “televised” a little loosely here. Because my Mom and Dad were present at my confirmation hearing, I’m pretty sure viewership was close to zero.

[3] Snap Inc., Form S-1 (February 2, 2017) (“Holders of our Class A common stock—the only class being sold in this offering—are entitled to no vote on matters submitted to our stockholders.”).

[4] In 1926, the NYSE’s famous decision to list nonvoting shares in Dodge Motor Company resulted in a public outcry. In response, the Exchange announced that it would consider voting control when making listing decisions, and in 1940 the NYSE announced a flat policy against nonvoting common stock. Prior to these events, restrictions on shareholder voting rights were more common. See Stephen Bainbridge, ProfessorBainbridge.com, Understanding Dual Class Stock Part I: An Historical Perspective (September 9, 2017). Then again, prior to these events, the Securities and Exchange Commission did not exist.

[5] Stephen M. Bainbridge, Comments to the Securities and Exchange Commission on No. 4-537: The Scope of the SEC’s Authority Over Shareholder Voting Rights (May 7, 2007).

[6] The SEC, led at the time by Chairman Arthur Levitt, attempted to intervene—but was thwarted by a controversial ruling of the D.C. Circuit. Business Roundtable v. SEC, 905 F.2d 406 (D.C. Cir. 1990).

[7] Wall Street Journal Business Blog: The Big Number, Wall. St. J. (Aug. 17, 2015).

[8] These trends are consistent with those noted by an insightful preliminary report by the Investor as Owner Subcommittee of the SEC’s Investor Advisory Committee. See SEC, Investor Advisory Committee, Discussion Draft: Dual Class and Other Entrenching Governance Structures in Public Companies (December 17, 2017).

[9] See, e.g., Alphabet Investor Relations, 2011 Founders’ Letter (“In our experience, success is more likely if you concentrate on the long term. . . . For example, it took over three years just to ship our first Android handset, and then another three years on top of that before the operating system truly reached critical mass.”).

[10] See, e.g., Sens. Elizabeth Warren & Joe Donnelly, Trump’s SEC Chairman Must Look Out for American Families, Not Big Corporations, Wash. Post. (March 22, 2017) (“[S]hortsighted corporations [are] chasing quick profits at the expense of their workers and the long-term health of their companies.”

[11] See, e.g., Council of Institutional Investors: Dual-Class Stock (Jan. 2018), at http://www.cii.org /dualclass_stock (“CII continues to view one-share equal voting rights upon IPO as the optimal approach.”).

[12] Many prominent dual-class companies and their managers seem to understand this problem and have begun to consider alternatives that would address the concern. See, e.g., Sujeet Indap, Dual-Class Shares Should Build in Expiration Plan, Fin. Times (October 26, 2017) (noting that, in connection with a proposed recent recapitalization of Facebook’s dual-class stock, Mark Zuckerberg “offered to add a provision that would reduce his existing super shares to ordinary shares if he died, resigned as chief executive or was terminated for cause.”).

[13] The Elusive Thomas Jefferson: The Man Behind the Myths 38 (M. Andrew Holowchak & Brian W. Dotts eds., 2012) (quoting an early letter from Jefferson to John Adams).

[14] U.S. Const. art. I § 9, cl. 8 (“No Title of Nobility shall be granted by the United States: And no Person holding any Office or Profit of Public Trust under them, shall, without the Consent of the Congress, accept any present, Emolument, Office, or Title, of any kind whatever, from any King, Prince, or foreign State.”).

[15] Publius, The Federalist No. 63 (B. Wright ed., 1961) (arguing, by dint of comparison between the proposed Senate and the British House of Lords, that the former was not, and was unlikely to become, “[]confined to particular families and fortunes[ or] an hereditary assembly of opulent nobles.”).

[16] Samuel Fleischacker, On Adam Smith’s “Wealth of Nations”: A Philosophical Companion (2014) (quoting Smith’s lectures on jurisprudence).

[17] Casablanca, Dir. Michael Curtiz (Warner Bros. 1942).

[18] The idea that concentrated corporate power is held in just a few individuals’ hands and will be passed down to their heirs is made all the more troubling by the fact that so few corporations today wield so much influence over so many American lives. I wonder how many of the problems plaguing our securities markets today can and should be treated by that old, familiar, and uniquely American medicine: competition.

[19] Martijn Cremers, Beni Lauterbach, and Anete Pajuste, The Life-Cycle of Dual-Class Firms (Jan. 1, 2018), at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3062895.

[20] Lucian Bebchuk & Kobi Kastiel, The Untenable Case for Dual-Class Stock, 103 Va. L. Rev. 585 (2017).

[21] For our principal analysis we assess value with a much-maligned measure of corporate performance: Tobin’s Q. Important recent work, however, has shown the danger in relying exclusively on Tobin’s Q for purposes like these. See Robert P. Bartlett & Frank Partnoy, The Misuse of Tobin’s Q (February 4, 2018); see also Emiliano Catan & Michael Klausner, Board Declassifications and Firm Value: Have Shareholders Really Destroyed Billions in Value? (October 10, 2017). So we re-ran our analysis using monthly equal-weighted portfolio returns for the perpetual sample versus the sunset sample. We did this in both calendar time and then, separately, in event time, with each firm’s life cycle starting at zero and proceeding for 48 months. We then constructed a long-short cumulative return for the difference between the two portfolios, and the results are very consistent with those described above.

[22] One might ask why we compare firms with perpetual dual-class to those with dual-class sunset provisions rather than firms with a single class of stock. We do this because we, like scholars in the area, worry that any attempt to match perpetual dual-class firms with single-class firms will omit important differences that cannot be adequately controlled for. See Cremers, Lauterbach, and Pajuste, supra. Since our sample includes only dual-class firms, we avoid the possibility that underlying differences between single-class and dual-class firms drive our results.

[23] This evidence does not, of course, establish that perpetual dual-class structures cause firms to suffer lower valuations. It may be, for example, that the causal arrow runs the other way: that firms anticipating that they will be worth less later in their life cycle select perpetual dual class structures. Either way, the evidence suggests that this governance structure is associated with lower firm value. These data make it unsurprising that investors have expressed such significant concern about the use of dual class.

[24] I could bore you with the details of our regressions, fixed effects, and clustered standard errors, but I know that’s not what you came to hear about. Instead, I’ll point the interested listener to the data appendix to this speech, where you can learn more about our methodology and analysis. I hope that this first step will help bring increased academic interest to dual-class stock—and the ongoing debate about its costs and benefits for investors.

[25] See Investor Advisory Committee, supra; Council of Institutional Investors, supra.

[26] FTSE Russell, FTSE Russell Voting Rights Consultation: Next Steps (July 2017), available at http://www.ftse.com/products/downloads/FTSE_Russell_Voting_Rights_Consultation_Next_Steps.pdf.

[27] S&P Dow Jones Indices, Decision on Multi-Class Shares and Voting Rights (July 2017), available at https://www.spice-indices.com/idpfiles/spice-assets/resources/public/documents/561162_spdjimulti-classshares andvotingrulesannouncement7.31.17.pdf?force_download=true.

[28] MSCI, Consultation on the Treatment of Unequal Voting Structures in the MSCI Equity Indexes (January 2018), at https://www.msci.com/documents/1296102/8328554/Consultation_ Voting+Rights.pdf.

[29] See, e.g., Matt Levine, Listing Standards and Dividend Shares, Bloomberg View: Money Stuff (April 13, 2017) (arguing that excluding firms on the basis of governance characteristics is a “weird role” for stock indices, and pointing to the “long tradition of corporate governance standards being imposed by stock exchanges as ‘listing standards,’ a sort of seal of approval . . .”).

[30] Edward N. Wolff, Household Wealth Trends in the United States, 1962 to 2016: Has Middle Class Wealth Recovered? (November 2017, NBER Working Paper No. 24085).

[31] Some may argue that, since investors can price the effects of perpetual dual-class at the IPO stage, there is no need for such standards. I am unconvinced that the IPO markets we have today reflect the kind of efficiency that argument demands. In any event, exchange standards need not require dual-class to end—just that shareholders get to vote on the structure. If managers can convince the markets of their merits, they’ll be free to retain dual-class.

[32] For innovative proposals in this respect, see Bebchuk & Kastiel, supra, at 619-628.

This post is based on remarks delivered on February 15, 2018, by Robert J. Jackson, Jr., a commissioner of the U.S. Securities and Exchange Commission, at the University of California at Berkeley. The original version of the remarks are available here.

I have a solution: Put all companies with multiple classes of shares back on the Amex–like in the old days.

There was one exception, Dow Jones had two classes and was listed on the NYSE.

I am not convinced that having a single class of stock would have led to better governance of The New York Times, The Washington Post or Viacom.

A counter-example is Wang Computer–the family should have surrendered control.