Sky Blog

Sky Blog

When does a shareholder become powerful enough to control a corporate vote?

That question has taken on unusual importance in Delaware. Unlike ordinary shareholders, controlling shareholders are subject to fiduciary duties. And after litigation over Elon Musk’s compensation package, in which Musk was deemed a controlling shareholder of Tesla despite holding only 22% of the company’s voting stock, Delaware lawmakers adopted a bright-line rule: A shareholder with less than one-third of the voting stock cannot be deemed controlling based on stock ownership alone.

In a new paper, I provide the first quantitative analysis of shareholder voting power—the ability to determine corporate outcomes through voting alone. (Here, I use “voting power” in the sense common in the political science literature, the ability to influence outcomes through voting, rather than a shareholder’s percentage ownership of voting stock.) Although controlling-shareholder doctrine also turns on relationships with management, contractual rights, and practical influence, a shareholder’s influence ultimately depends on her past or future ability to shape the outcome of shareholder votes. The recent turn to numerical ownership thresholds highlights a basic gap in our understanding: At what level of ownership does a shareholder, by virtue of her votes alone, become essentially able to dictate the outcome of a contested election?

The paper begins with a descriptive look at the largest shareholders of U.S. public companies. Corporate governance scholarship often focuses on the giant mutual-fund families, and in fact, at many public companies, one of BlackRock, Vanguard, State Street, or Fidelity is the largest shareholder. But these fund families rarely hold the kinds of stakes associated with near-dominant voting power. In U.S. public companies, mutual fund ownership rarely exceeds 20%. Above that level, the largest shareholders are typically individuals or other blockholders such as hedge funds, private investment vehicles, family offices, or corporate parents.

Ownership stakes in the 20s to low 30s tend to have tremendous influence over the vote. A simple way to see why is to compare the largest shareholder with the next few largest holders. Among firms with a largest shareholder holding 25 to 30% of the vote, the median largest owner holds more shares than the next four shareholders combined. Among firms with a 30 to 35% owner as the largest shareholder, the median largest shareholder exceeds the combined holdings of the next nine shareholders.

To assess voting power more systematically, the paper develops a quantitative measure of shareholders’ ability to change the outcome of a vote by casting their shares. The metric comes from the voting-power literature in political science, but it has not been applied empirically to U.S. corporate ownership data.

One of the paper’s central findings is that once a shareholder reaches a block in the mid-20s, assembling an opposing coalition often becomes extremely difficult for the remaining shareholders.

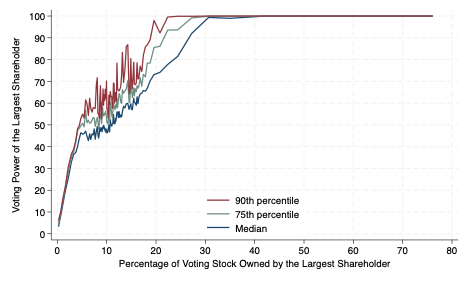

That pattern shows up clearly in the data. The figure below illustrates how voting power rises with ownership, showing the median, 75th percentile, and 90th percentile levels of voting power for a given level of ownership by the largest shareholder.

Among firms where the largest shareholder owns between 25 and 30% of the stock, roughly two-thirds have voting power above 80%, and nearly one-third have voting power above 99%. Even some shareholders with only about 20% ownership have voting power above 99%, meaning that the 20% shareholder is decisive in over 99% of possible coalitions. There are thus many public companies in which a shareholder who owns an amount of stock well below Delaware’s one-third threshold can, as a practical matter, dominate the vote.

Ownership percentages alone are a poor proxy for influence. The largest shareholder’s stake explains only about half of the differences in voting power across firms. Once one also accounts for how concentrated ownership is among the other large shareholders, the model’s explanatory power rises substantially, explaining 84% of those differences. To understand voting power, then, one must know not only how much the largest shareholder owns, but also how much is held by other large shareholders.

The gap between ownership and voting power is especially large in firms with substantial retail ownership. Retail investors vote at lower rates than institutions and, when they do vote, are less likely to shift their votes in contested situations. As a result, a large blockholder’s effective weight among votes actually cast can exceed her share of outstanding stock.

These results have implications for common ownership and other corporate-governance issues, but their immediate relevance is to controlling-shareholder doctrine. Most obviously, they suggest that Delaware’s one-third rule captures only a subset of shareholders who may be capable of dominating votes. That does not by itself resolve whether a bright-line rule is preferable to the older, more qualitative approach, but it does show that one-third ownership is not a reliable proxy for voting control.

The findings also suggest that courts and commentators should pay closer attention to a firm’s broader ownership structure in controller cases. In such cases, courts often begin by referencing the largest shareholder’s percentage ownership before turning to qualitative factors. But ownership alone may miss important variation in voting power. A 22% shareholder facing a fragmented field may be far more powerful than a 35% shareholder facing several other large, cohesive holders.

None of this means that voting power is determinative of control. The paper measures only one facet of power: the ability to dictate voting outcomes through the vote. But it is an important component, and one that the law has recently tried to translate into a simple ownership threshold. The evidence suggests that translation is simplistic. If we want to know when a shareholder can truly control a corporate vote, we should start asking how difficult it would be to defeat her.

Jonathon Zytnick is an associate professor at Georgetown Law Center. This post is based on his recent article, “Shareholder Voting Power,” available here.