Sky Blog

Sky Blog

Executives, directors and other corporate insiders have privileged access to material non-public information. Previous research shows that trades by insiders are informed, on average. For example, insider purchases tend to precede positive stock returns. In addition, like other investors, corporate insiders may have different investment horizons (i.e., anticipated stock-holding periods) when they trade their company’s stock, depending on their personal investment objectives and styles; desire for liquidity, diversification, or corporate control;, compensation contracts; or understanding and attitude toward insider trading laws.

In our recent paper, “Insider Investment Horizon,” we examine the relation between the investment horizon of corporate insiders and the information content of their trading activity regarding future stock returns. We develop an empirical measure of an insider’s investment horizon as the average annual turnover in his or her company’s stock in the past. Higher turnover involves switching more frequently between buying and selling, which indicates that an insider updates his or her positions to realize profits in a more timely manner, and thus signals a shorter investment horizon. In contrast, lower turnover means that an insider tends to either buy or sell over time (not both), which suggests less of an inclination to realize profits in a timely fashion, and thus a longer investment horizon.

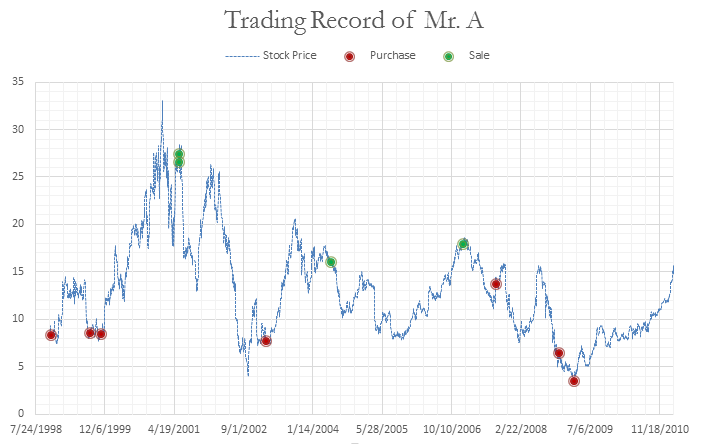

For example, Frank Laukien (chairman, president, and CEO of Bruker Corporation) made multiple purchases of Bruker stock each year from 2003 to 2013, while never selling a single share. Bill Gates made hundreds of sales and no purchases of Microsoft stock from 1996 to 2013. In contrast, consider the insider trading activity of Mr. A over time, plotted in the figure below. Mr. A was a director of company B, a multinational corporation with a market capitalization of $2.5 billion at the end of 2014 (the insider and his firm are real, but their names are disguised to protect his identity). He switched between buying and selling his company’s shares frequently during his 10 years as an insider. We argue that Laukien and Gates focus on long term trading goals and can be considered long horizon insiders. On the other hand, Mr. A is more likely to be interested in short term personal investment objectives and therefore should be classified as a short horizon insider.

We note that the “short-swing rule” (SEC Rule Section 16) requires corporate insiders to return any profits made from purchases and sales (i.e., “round-trip transactions”) of company stocks, if both transactions occur within a six-month period. However, even under this law, insiders will still reveal different inclinations to realize profits by both buying and selling company shares over time, and thus will display different investment horizons that range from slightly more than six months to many years.

Why would investment horizons matter in interpreting the information conveyed by insider trades? There are many reasons. Short horizon insiders, for example, might both buy and sell the company’s shares because they’re familiar with their firm’s operations and want to make short term profits. In this case, we may expect their trading activity to contain more predictive information about short term stock returns. On the other hand, it is possible that short horizon insiders turn over their insider holdings more frequently due to psychological biases, such as overconfidence, and their trades might reflect these biases rather than information. In this case, the trades of short horizon insiders may be less informative about future returns compared with the trades of long horizon insiders. Alternatively, long horizon insiders might purchase or sell due to similar overconfidence or hubris. These psychological biases may make long horizon insiders reluctant to update their personal beliefs about the firm’s prospects, leading to trades that are less informed. Finally, it is also possible that insiders with different horizons focus on different types of information with a varying shelf life.

We begin our analysis by examining the extent to which our measure of insider investment horizon varies across individuals. Surprisingly, we find that there are many long horizon insiders who, like Laukien and Gates, exclusively buy or sell over long periods. We also find that both the sales and purchases of short horizon insiders are more informative with regard to returns a month later, when compared with the activity of long horizon insiders. In particular, a long-short tradable strategy that replicates the recent purchases and sales of short horizon insiders earns an average risk adjusted return of 2.04 percent per month. In contrast, a similar strategy that mimics the recent trades of long horizon insiders earns just 0.77 percent per month.

We also study the longer term performance of trades by insiders with different horizons. We find that the trades of short horizon insiders continue to outperform those of long horizon insiders for up to one year later. However, there is no such evidence of differential trading performance in the longer run (beyond one year).

We further investigate the potential reasons for the superior trading performance of short horizon insiders. We show that the trades of short horizon insiders better predict earnings surprises and large stock price changes. This finding suggests that the superior trading performance of short horizon insiders is related to material non-public information that is about to become public. Since insider trading activity is regulated by law and is under intense scrutiny by regulators and other market participants, we further study whether SEC enforcement activity deters such exploitation of private information by short horizon insiders. We find that short horizon insiders tend to reduce their trading activity following periods of intensified SEC enforcement activity regarding insider trading cases.

Finally, we compare the personal attributes of short horizon with those of long horizon insiders. We find that short horizon insiders tend to come from smaller firms and firms with weaker corporate governance. They also tend to be male, hold MBA or non-PhD degrees, and hold prominent offices within the firm, such as CEO, CFO, or chairman of the board, and thus have better access to material private information.

In conclusion, we show that an insider’s investment horizon represents an important determinant of the information content of insider trades. This attribute of insiders may be useful in helping investors and regulators strip away less valuable information from the large volume of insider trading activity, allowing them to focus on the subset of insiders whose trades are more informative.

This post comes to us from Professor Ferhat Akbas at the University of Kansas, Professor Chao Jiang at the University of South Carolina, and Professor Paul D. Koch at the University of Kansas. It is based on their recent paper, “Insider Investment Horizon,” available here.