Sky Blog

Sky Blog

On April 23, 2024, the U.S. Department of Labor (“DOL” or “Department”) released its final fiduciary rule, marking the completion of its third attempt since 2010 to update the definition of what it means to be an investment advice fiduciary to IRAs and ERISA Plans. Entitled the “Retirement Security Rule,” the release revises regulation the DOL first adopted in 1975 defining what it means to be a fiduciary in the context of providing advice to retirement investors (the “Final Rule”) and amends various class prohibited transaction exemptions applicable to investment advice fiduciaries (including, PTE 2020-02, PTE 84-24 and others). The Final Rule focuses on whether advice is being provided to retirement accounts in the context of a trusted advice relationship. The Final Rule is considerably narrower in scope from the rule the DOL adopted in 2016 (which the Fifth Circuit vacated in its entirety two years later)1 since it limits fiduciary status to recommendations made by persons who effectively hold themselves out as occupying a position of trust and confidence with respect to a retirement investor. This should make the Final Rule less disruptive for managers of private funds such as private equity, credit, real estate and hedge funds than the 2016 rule, but there are certain important points for managers to focus on. This alert focuses on the practical impacts of the Final Rule on such private fund managers.

This narrower scope results from a number of critical changes from what the DOL proposed in the fall of 2023 (the “Proposal),2 and these changes limit the primary impact of the Final Rule to service providers in the retail investment space who recommend rollover transactions from an ERISA plan to an IRA or provide investment advice to IRAs, as well as to independent insurance producers who recommend non-securities-based annuities. A legal challenge to the Final Rule has already been filed by an insurance industry trade group in the U.S. District Court for the Eastern District of Texas on May 2, 2024 that seeks to vacate the Final Rule and exemption amendments and enjoin the Department from enforcing, implementing, or otherwise giving them effect in any manner.3 In addition, on May 15, 2024, members of the House and Senate introduced a resolution to overturn the Final Rule pursuant to the Congressional Review Act (“CRA”).4

Nonetheless, participants in the financial services industry, including, asset managers of open- and closed-end funds, broker-dealers, and financial advisers, must consider whether the Final Rule could cause current marketing practices and communications to be considered potential fiduciary advice. The stakes are high, because affected institutions and individuals that are deemed to render fiduciary advice will be subject to the highest duties of loyalty and care under U.S. law and strict prohibitions against specified transactions that present conflict of interest potential when dealing with ERISA-covered plans and IRAs.

Relationships’ and Expectations’ Control over the Content of the Advice

The Final Rule is most focused on the relationship between an advice provider and the recipient of that advice. If a person or entity represents or acknowledges that they are acting as a fiduciary to ERISA Plans and IRAs with respect to an investment recommendation, that clearly defined relationship will make those recommendations fiduciary in nature.

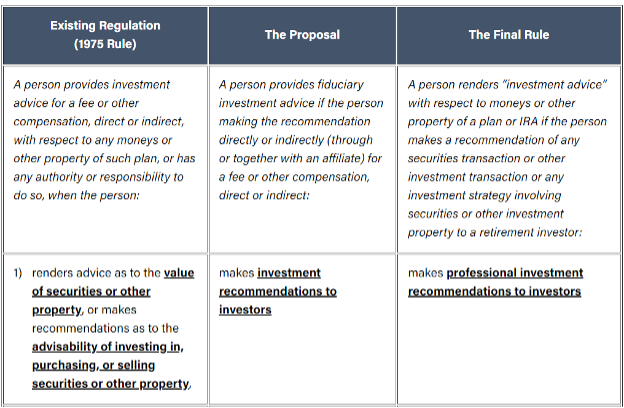

As the chart below depicts, under the 1975 rule, the focus has always been placed on the advice itself and whether that advice met all five criteria necessary to be categorized as fiduciary in nature. If one or more of these elements was not satisfied, then the recommendation or communication would not be considered fiduciary advice. Under the Final Rule, the DOL has established an objective facts-and-circumstances inquiry that looks at the nature of the relationship between the advice provider and the advice recipient, and what the reasonable expectations of the recipient may be. This means that it is possible to render advice to a retirement investor without being a fiduciary, so long as the relationship between the advice provider and the retirement investor is clearly defined and understood by all parties.

The DOL makes clear in the preamble that the new standard is not intended to pick up all interactions between financial professionals and retirement investors nor is it intended to impose fiduciary status on considerations beyond the nature of the relationship (as evaluated pursuant to each of the specific components laid out in the Final Rule). As the DOL explains, there are no “talismanic phrases” that the advice provider must utter before triggering fiduciary status. Instead, rather than focusing on whether a particular interaction could be considered fiduciary investment advice, the Final Rule says it is the circumstances under which the advice is given, and whether those facts and circumstances would objectively be viewed as given in the context of a trusted relationship that will be determinative.

Key Takeaway

Asset managers should evaluate disclosures to make sure the relationship between the manager and the recipients of PPMs and other marketing documents is correctly defined. While there are no “magic words” to define a relationship, clear language about advice not being individualized or given in the context of a trusted relationship can be helpful.

Retirement Investors

For purposes of the new test, the Final Rule has added a new definition for the recipients of investment advice:

| Term | Definition |

| Retirement Investor |

a plan, plan participant or beneficiary, IRA, IRA owner or beneficiary, plan fiduciary within the meaning of ERISA section (3)(21)(A)(i) or (iii) Code section 4975(e)(3)(A) or (C) with respect to the plan, or an IRA fiduciary within the meaning of Code section 4975(e)(3)(A) or (C) with respect to the IRA. |

Notably, the definition only applies to plan and IRA fiduciaries to the extent they exercise authority or control over plan assets, or discretionary authority or discretionary control with respect to the plan’s management, or the possession of discretionary authority or discretionary responsibility in the plan’s administration. Plan and IRA fiduciaries that are themselves investment advice fiduciaries are not picked up by this definition because the recipient of the communication does not have the authority or control necessary to invest the plans’ assets.

Key Takeaway

Unlike the 2016 rules, the Final Rule does not contain a specific, representation-based exception from fiduciary advice for interactions with sophisticated counterparties like other advice fiduciaries. That said, the risk of providing inadvertent fiduciary advice can be lowered by making it clear that advice is being addressed to a counterparty in its general capacity, and not in its capacity as a retirement investor with respect to a particular plan or IRA.

Recommendations

The kinds of recommendations that are the subject of the Final Rule’s test track the three categories the DOL had included in its Proposal:

- Post-Rollover Investments – Recommendations as to the advisability of acquiring, holding, disposing of, or exchanging, securities or other investment property, as to investment strategy, or as to how securities or other investment property should be invested after the securities or other investment property are rolled over, transferred, or distributed from the plan or IRA;

- In-Plan Investments – Recommendations as to the management of securities or other investment property, including, among other things, recommendations on investment policies or strategies, portfolio composition, selection of other persons to provide investment advice or investment management services, selection of investment account arrangements (e.g., account types such as brokerage versus advisory) or voting of proxies appurtenant to securities; and

- Whether to Roll Over – Recommendations as to rolling over, transferring, or distributing assets from a plan or IRA, including recommendations as to whether to engage in the transaction, the amount, the form, and the destination of such a rollover, transfer, or distribution.

Furthermore, as the DOL explains in the preamble, for determining whether a communication amounts to a recommendation, it needs to amount to a “call to action” and the more individually tailored the communication is to a specific retirement investor about a security, investment property or strategy, the more likely the communication may be viewed as a recommendation. This determination is an objective standard, and it is intended to be construed in a manner consistent with the SEC’s framework in Regulation Best Interest for assessing whether a broker-dealer has made a recommendation to a retail investor.

Key Takeaway

While most private fund managers are unlikely to make rollover recommendations, caution should be exercised in discussing potential changes in IRA custodian or similar account changes as part of facilitating an investment into a private fund.

Exceptions to Fiduciary Advice: Sales Pitches and Investment Education

As noted above, unlike its 2016 predecessor, the Final Rule does not provide a specific carveout for recommendations to sophisticated, independent advice recipients on the basis that the DOL believes it is preferable to utilize a facts-and-circumstances test for recommendations to plan sponsor fiduciaries absent an acknowledgment of fiduciary status with respect to the recommendation. Without this carveout, it raises the possibility that various interactions between retirement plans and financial institutions may potentially be considered fiduciary in nature. However, in a welcome change, the Final Rule has added two important exceptions to the regulatory text for situations where the DOL believes fiduciary advice status should not apply: sales pitches that fall short of meeting the test described above, and investment information or education without an investment recommendation.

The sales exception should provide some reassurance that marketing materials that get prepared (i.e., PPMs, pitchbooks and publicly facing websites) as well as the communications that occur during normal course fundraising should likely not be categorized as fiduciary advice.

Key Takeaway

Managers of private funds may need to have different approaches to communicating with different types of investors—i.e., if a manager is marketing its funds or investment products to individual IRA owners, that will likely require more explicit written and oral statements of intent than communications between the fund manager and a plan fiduciary, placement agent or consultant regarding the addition of funds to an investment lineup.

Amendments to Prohibited Transaction Exemptions

In addition to the Final Rule, the Department has also adopted amendments to several existing exemptions that provide relief from the prohibited transaction rules applicable to fiduciaries under Title I of ERISA and the Code. There are two exemptions available for the management of conflicts of interest that arise in connection with providing fiduciary investment advice:

- PTE 2020-02 – Provides exemptive relief when an investment advice fiduciary, its affiliate or a related party receives compensation (such as commissions, trailing fees or revenue-sharing) in connection with providing fiduciary investment advice to retirement investors or engaging in principal transactions with retirement investors; and

- PTE 84-24 – Provides exemptive relief for compensation received for investment advice provided by independent insurance producers that recommend annuities from multiple unaffiliated insurance companies to retirement investors.

The DOL also amended PTEs 75-1 Parts III and IV, 77-4, 80-83, 83-1, and 86-128 to eliminate relief for the receipt of compensation resulting from fiduciary investment advice, as defined under ERISA. From an asset manager’s perspective (and consistent with the DOL’s stated rationale in the preamble), rather than looking to an assortment of different exemptions with varying conditions for a variety of transactions, investment advice fiduciaries will generally be expected to rely solely on the amended PTE 2020-02 for relief for covered investment advice transactions.

PTE 2020-02: Background and Noteworthy Changes

PTE 2020-02 conditions relief on the investment professional and financial institution providing advice in accordance with the following “impartial conduct standards”:

- committing to provide advice in retirement investors’ best interest,

- charging no more than reasonable compensation for such advice, and

- not making misleading statements about investment transactions and other relevant matters.5

In addition, the exemption requires financial institutions to acknowledge in writing the financial institution’s and their investment professionals’ fiduciary status under Title I of ERISA and the Code, as applicable, when providing investment advice to the retirement investor, and to describe in writing the services to be provided and the financial institutions’ and investment professionals’ material conflicts of interest.

Financial institutions are required to adopt policies and procedures prudently designed to ensure compliance with the impartial conduct standards and conduct a retrospective review of compliance. In order to ensure that financial institutions provide reasonable oversight of investment professionals and adopt a culture of compliance, PTE 2020-02 provides that financial institutions and investment professionals will be ineligible to rely on the exemption for 10 years if they are convicted of certain crimes arising out of their provision of investment advice to retirement investors. They can also become ineligible if they engage in a systematic or intentional violation of the exemption’s conditions or they provided materially misleading information to the DOL in relation to their conduct under the exemption.

In addition to the changes for advice in general, the amendments to PTE 2020-02 expand exemptive relief for certain principal transactions. Prior to the amendments, the only types of principal transactions that the exemption covered were riskless principal transactions and Covered Principal Transactions.6 Any principal transactions that did not fall into either of these categories was not eligible for relief under PTE 2020-02. The DOL has expanded the types of transactions that are covered by the exemption in order to ensure that financial institutions and investment professionals can recommend a wide variety of products to retirement investors, provided, they comply with PTE 2020-02’s stringent standards of care and adhere to the policies and procedures, conflict mitigation and retrospective review requirements of the exemption.

Key Takeaway

For an asset manager that has already implemented a compliance program for PTE 2020-02, this expansion is a welcome change as it may enable the manager to rely on the exemption for certain fund rebalancing transactions or providing investors with enhanced liquidity for their interests, including at the end of life for a fund or mandate. For managers that chose not to utilize PTE 2020-02 due to the limited relief it offered in the principal transaction context, it may be time to reconsider whether it would be commercially beneficial and/or feasible to do so going forward.

Outlook

The Final Rule and amended exemptions are set to take effect on September 23, 2024. Separately, the DOL included a one-year transition period after the effective date for certain transactions relying on the amended exemptions.

Besides the possibility of this regulatory initiative being invalidated in the courts similar to what happened to the 2016 rule, there is also political uncertainty given the upcoming presidential election. Moreover, members of Congress have expressed their strong disapproval of what the DOL has done. For example, immediately after the Final Rule was released, House Education and the Workforce Committee Chairwoman Virginia Foxx (R-NC) stated, “[The] DOL failed to learn from its own past blunders. This final fiduciary rule mirrors its shameful predecessor that was vacated by the 5th U.S. Circuit Court of Appeals in 2016. The final rule once again encroaches on the regulatory jurisdictions of the Securities and Exchange Commission and state insurance regulators. This regulatory overreach runs counter to the will of Congress and court decisions…”7 Also, as noted above, several high-profile senators and representatives introduced a resolution of disapproval under the CRA on May 15, 2024 that seeks to overturn what they claim is “a flawed rule from the DOL that would endanger financial choice and access.” Under the CRA, Congress generally has a 60-day window to act on a joint resolution of disapproval to take advantage of the CRA’s special “fast track” procedures. If both the House and Senate pass the resolution and it is signed by the President, the CRA states that the disapproved rule shall not take effect (or continue).8

For these reasons, we believe managers of private funds should continue to evaluate the potential impacts on their businesses under the Final Rule, in preparation for the effective date.

ENDNOTES

- Chamber of Commerce v. United States Department of Labor, 885 F.3d 360 (5th Cir. 2018). For background information about the 2016 rule and its subsequent history, please view the following selection of our prior alerts:

- “DOL Issues “Conflict of Interest” Rule on Investment Advice: Fiduciary Net Will Widen on April 10, 2017” (April 13, 2016).

- “Department of Labor Provides Guidance on Fiduciary Rule Transition Period” (May 23, 2017).

- “Key Considerations for Asset Managers under the DOL’s Fiduciary Rule” (June 13, 2017).

- “Fifth Circuit Raises New Questions by Ruling that the Fiduciary Rule Is Invalid” (March 21, 2018).

- “Fifth Circuit Issues Mandate Vacating the DOL’s Fiduciary Rule” (June 25, 2018).

- For a summary of the Proposal, please refer to our alert, “DOL’s Latest Attempt to Define Who Is an Investment Advice Fiduciary under ERISA: Initial Considerations for Asset Managers” (November 8, 2023).

- Federation of Americans for Consumer Choice Inc. v. United States Department of Labor, E.D. Tex., No. 6:24-cv-00163, complaint filed May 2, 2024.

- “Rep. Allen and Senator Buss Introduce Resolution to Protect America’s Retirees and Savers: Resolution Would Nullify President Biden’s Overreaching Fiduciary Rule,” May 15, 2024, available at https://allen.house.gov/news/documentsingle.aspx?DocumentID=6283. See also, “Ranking Member Cassidy, Budd, Manchin, Colleagues Introduce Bipartisan CRA to Overturn Biden’s Fiduciary Rule,” May 15, 2024, available at https://www.help.senate.gov/ranking/newsroom/press/ranking-member-cassidy-budd-manchin-colleagues-introduce-bipartisan-cra-to-overturn-bidens-fiduciary-rule.

- Please refer to our alerts below, which summarize PTE 2020-02 and the subsequent interpretive guidance the DOL issued in 2021:

- “The DOL Releases Final Investment Advice Prohibited Transaction Exemption” (December 21, 2020).

- “DOL Issues Interpretative Guidance on Investment Advice Prohibited Transaction Exemption (PTE 2020-02)” (April 21, 2021).

- As amended, PTE 2020-02 no longer includes the term, “Covered Principal Transaction,” which had been defined as principal transactions involving the following types of investments:

- For purchases by the financial institution from a retirement plan or IRA– The term was broadly defined to include any securities or other investment property.

- For sales from the financial institution to a retirement plan or IRA– The term only applied to transactions involving corporate debt securities offered pursuant to a registration statement under the Securities Act of 1933; U.S. Treasury securities; debt securities issued or guaranteed by a U.S. federal government agency other than the Department of Treasury; debt securities issued or guaranteed by a government-sponsored enterprise; municipal bonds; certificates of deposit; and interests in Unit Investment Trusts.

- “Chair Foxx Statement on Final Fiduciary Rule”, April 23, 2024, available at https://edworkforce.house.gov/news/documentsingle.aspx?DocumentID=410481.

- John Sullivan, “Fiduciary Rule Opponents Use Congressional Review Act to Thwart DOL,” National Association of Plan Advisors, May 16, 2024, available at https://www.napa-net.org/news-info/daily-news/fiduciary-rule-opponents-use-congressional-review-act-thwart-dol.

This post comes to us from Ropes & Gray LLP. It is based on the firm’s memorandum, “The DOL’s Final Fiduciary Rule: What Private Fund Managers Need to Know,” dated ay 20, 2024, and available here.