Sky Blog

Sky Blog

I am delighted to have this opportunity to speak at West Virginia University. Thanks to Brian Cushing for inviting me here today.1

Gathered in this part of West Virginia, we are located in the Fifth Federal Reserve District, which stretches down from here to South Carolina and east to the Atlantic Ocean (figure 1). More than 100 years ago, the organizers of the Federal Reserve System divided the country into 12 of these Districts, each with its own Federal Reserve Bank. Together, the Board of Governors in Washington and the 12 Reserve Banks are the key elements of the Federal Reserve System.

Today I will discuss how the Federal Reserve came to have this unique structure. The Fed’s organization reflects a long-standing desire in American history to ensure that power over our nation’s monetary policy and financial system is not concentrated in a few hands, whether in Washington or in high finance or in any single group or constituency. Rather, Americans have long desired that decisions about these matters be influenced by a diverse set of voices from all parts of the country and the economy. The structure of the Federal Reserve was designed to achieve this broad representation and promote a stronger financial system to build resiliency against the sort of periodic financial crises that had repeatedly damaged the country in the 19th and early 20th centuries. This structure was forged from compromise; the result of that compromise was a vitally needed central bank whose decisions take into account a broad range of perspectives.

Before the Federal Reserve

The question of how to structure our nation’s financial system arose in the early years of the republic. In 1791, Congress created an institution known as the Bank of the United States, often considered a forerunner of the Federal Reserve. The Bank was created in part to assist the federal government in its financial transactions, a typical responsibility of central banks at that time. It was also designed to help America’s financial system meet the needs of a growing economy–the same purpose behind the founding of the Federal Reserve more than 100 years later. The most famous proponent of the Bank was Alexander Hamilton, who has recently achieved the central banker’s dream of being the subject of a hit Broadway musical (figure 2).

Congress gave the Bank of the United States unique powers–its notes were accepted for making payments to the federal government and it was the only bank able to branch across state lines (figure 3). The Bank could affect the ebb and flow of credit around the country.2 People in different regions of the country came to have distinct views about the Bank. Borrowers in the western areas–in those times, the West meant places like Ohio–desired cheap and abundant loans but were also wary of lenders. These borrowers grew opposed to the power of the Bank in the credit market. Northern business interests favored the Bank’s contribution to the country’s industrial development, but at times disagreed with actions taken by the Bank to constrain credit. Southern agriculturalists viewed the Bank with suspicion but supported its occasional actions to constrain credit to non-agricultural businesses.3 The Bank’s private ownership, intended to give it independence from government control, was a source of unpopularity. Ultimately, these disagreements undermined the Bank’s political support. After 20 years, Congress chose not to renew the Bank’s charter. A second Bank of the United States met a similar fate in 1836 when President Andrew Jackson vetoed a bill to extend its life (figure 4).

{kind=link}

These two short-lived experiments illustrate a theme in American history–of Americans from different regions holding distinct views about the structure and development of the financial system. People in the newer western parts of the country saw themselves as starved of access to credit and viewed higher interest rates in their areas as reflecting the scarcity of funds. Regional interest rate differentials persisted until around the time of World War I and helped shape the attitudes of Americans living in western areas toward the nation’s financial system.4

These regional differences gave rise to a major political movement in the latter part of the 19th century, as western farm borrowers increasingly demanded a reform of the U.S. monetary system. Their chief complaints included the high interest rates they faced as well as the burdens placed on them by deflation that increased the real value of their debts. Indeed, the economy experienced 1 to 2 percent deflation annually in the years leading up to the 1890s. The country’s currency was linked to gold, and deflation reflected the growing scarcity of gold relative to the amount of economic activity. The “free silver” movement grew in response to these economic forces. Its most famous advocate, William Jennings Bryan, the Democratic presidential nominee in 1896, sought an increase in the money supply–by the coining of silver in addition to gold–as a solution to reversing this deflation (figure 5).5

The Founding of the Fed

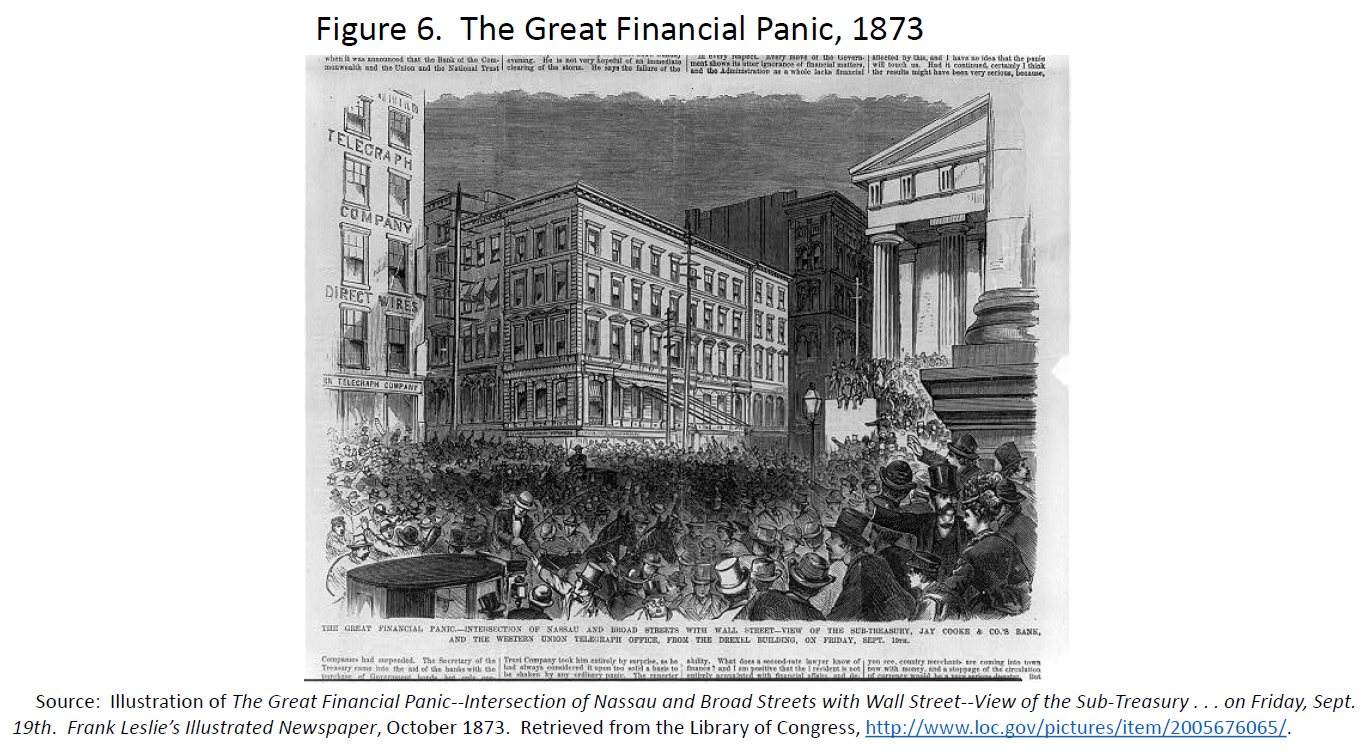

By the beginning of the 20th century, the debate about monetary policy and the nation’s financial system had been going on for over a century. Increasingly, the shortcomings of the existing system were causing too much harm to ignore. Like a drumbeat, the country experienced one serious financial crisis after another, with major crises in 1839, 1857, 1873, 1893, and finally in 1907.6These panics paralyzed the financial system and led to deep and extended contractions in the economy.

These episodes exposed the weakness of our 19th century financial system, which repeatedly failed to supply the money and credit needed to meet the economy’s demands. The financial system came under severe stress when the demand for liquidity surged.7 A financial system strained in such a manner is like dry kindling in danger of being exposed to a spark. That spark could come from losses at a well-known bank, from a disappointing harvest, or from mere rumors. In response, depositors or other investors would seek the return of their funds, which would force financial institutions to sell assets quickly to generate the necessary cash (figure 6). That liquidation could lead banks to cut credit and force borrowers to repay debt sooner than expected.

{kind=link}

Simply put, the monetary system did not meet the country’s needs. It was a system in crisis, boiling over repeatedly, harming the country.

Central banks are designed in part to help the financial system meet occasional liquidity strains. When demands for liquidity rise, central banks can respond by increasing the supply of money and thus adding liquidity to the system. Central banks have a particularly important role in avoiding or mitigating extreme demands for liquidity during financial crises. They do this by making loans to solvent financial institutions so they can meet their liquidity demands and avoid forced sales of their assets. These ideas about central banks’ lending role were developed over the course of the 19th century but not yet implemented in the United States, which at the time remained without a central bank.8 By the beginning of the 20th century, the United States was behind the game.

The final catalyst leading to the creation of the Federal Reserve was the severe Panic of 1907, which caused inflation-adjusted gross national product to decline by 12 percent, more than two times the decline recorded during the Great Recession of 2007 to 2009.9 After the panic ended, there was a broad sense that reform was needed, although consensus on the exact nature of that reform was elusive. Some called for an institution similar in structure to the Bank of England at the time, with centralized power, owned and operated by the banking system. Some wanted control to be lodged with the federal government in Washington instead. Others proposed that power be distributed to regional bodies with no central or coordinating board. Still others resisted any sort of central bank.10 This debate reflected the many and diverse interests in the United States–farmers, laborers, businessmen, small-town bankers, big-city bankers, technocrats, populists, and more–that experienced different conditions across a large geographic expanse.

The resulting institution was a compromise, created by the Federal Reserve Act in 1913. The Federal Reserve was not structured to be entirely private in its ownership and operation. It was also not structured to have a single headquarters in Washington or New York with branches across the country, a structure that was proposed but failed to attract enough political support. Instead, a more federated system was created, establishing the Federal Reserve Board in Washington and the 12 Reserve Banks located around the country.

The Board was the part of the System intended to be most directly accountable to the public (figure 7). The Board is an independent agency within the federal government, and members of the Board–now called Governors–are appointed by the President and confirmed by the Senate.11 Governors serve 14 year terms that expire at 2-year intervals and are not linked to election cycles. The Federal Reserve Board is charged with general oversight of the Reserve Banks.

The Reserve Banks combine both public and private elements in their makeup and organization (figure 8). Like the Board of Governors, the Reserve Banks operate with the public interest in mind. Commercial banks that are members of the Federal Reserve System are required to purchase stock in their District’s Reserve Bank.12 These shares are nontransferable and yield only limited powers and benefits. Dividends are set by federal law. The commercial bank shareholders elect two-thirds of the directors that oversee the Reserve Banks; the Board in Washington appoints the remaining one-third. Only three bankers can serve on a Reserve Bank’s board of directors, and only one of those can be from a large commercial bank in the District. The remaining six directors represent the interests of the public. The Federal Reserve System benefits enormously from the insights and support of the boards of directors of the Reserve Banks and their Branches. Directors include prominent private-sector leaders who represent a wide and growing diversity of backgrounds and views about the economy.13

The federated structure of the Federal Reserve System earned the endorsement of even the populist hero of the late 19th and early 20th centuries, William Jennings Bryan. The compromise created an institution that could address the shortcomings of the American financial system while assuring that control of the Federal Reserve would be shared widely.14 The structure was different from those of the first and second Banks of the United States, and from those of foreign central banks at the time. Congressman Carter Glass, who worked to win passage of the Federal Reserve Act in Congress, called the Federal Reserve’s uniquely American design “an adventure in constructive finance” (figure 9).15

{kind=link}

The Modern Federal Reserve

In the System’s early years, the decentralized structure gave the Reserve Banks considerable scope to make independent decisions that applied to their own Districts, which made it difficult to effect policy. For example, one Bank’s purchases of securities could be offset by another Bank’s sale, given that the market for securities was national in scope. As a result, the Reserve Banks created a committee to coordinate these “open market operations.” But in these years, the Reserve Banks were not bound by that committee’s decisions and could derail any attempt at coordinated action.

This decentralization was thought by some to have undermined the Federal Reserve’s response to the Great Depression.16 With that experience in mind, the 1935 Banking Act modified the distribution of power within the Federal Reserve System, giving the Board of Governors 7 of the 12 seats on the Federal Open Market Committee (FOMC) (figure 10).17 The other 5 seats are held by the Reserve Banks. The Federal Reserve Bank of New York has a permanent seat, and the other Reserve Banks share the remaining 4 seats on a rotating basis.18 While FOMC members are free to dissent from the majority decision about open market operations, the Reserve Banks are nevertheless required to adhere to that decision in conducting open market operations.

{kind=link}

The structure set out in 1935 has been essentially unchanged to this day and has served the country well. As intended by the framers, the federal nature of the system has ensured a diversity of views and promotes a healthy debate over policy. My strong view is that this institutionalized diversity of thinking is a strength of our System. In my experience, the best outcomes are reached when opposing viewpoints are clearly and strongly presented before decisions are made.

Members of the Board of Governors and Presidents of the Reserve Banks arrive at their own independent viewpoints about the economy and the appropriate path for monetary policy. Congress has assigned the FOMC the task of achieving stable prices and maximum employment; however, policymakers may disagree on the best way to achieve those goals.19 The System’s structure encourages exploration of a diverse range of views and promotes a healthy policy debate.20 In the modern Federal Reserve System, each Reserve Bank has an independent research department, with its own external publications. In addition, while the members of the Board tend to focus on developments in the nation as a whole, the Reserve Bank Presidents bring specialized information about their regional economies to the FOMC discussion. Before each FOMC meeting, Reserve Bank Presidents consult with their staff of economists as well as their boards of directors, business contacts in their Districts, and market experts to develop their independent views of appropriate monetary policy.

The FOMC works to achieve a consensus policy by blending inputs from the members of the Board of Governors and from the Reserve Bank Presidents under the leadership of its Chair. By tradition, the Chair of the Board has been chosen as the Chair of the FOMC and has had a central role in setting the agenda for the FOMC and developing consensus among the Committee’s members. In addition, the Chair is the most visible public face of the Federal Reserve System.

The Fed is accountable to Congress and the public for its activities and decisions. Historically, the activities of central banks were shrouded in mystery. Montagu Norman, the famously secretive Governor of the Bank of England from 1920 to 1944, reportedly took as his personal motto, “Never explain, never excuse” (figure 11).21

In the modern era, all that has changed, as central banks have come to see transparency both as a requirement of democratic accountability and as a way of supporting the efficacy of their policies. Over recent decades the Fed has significantly augmented its public communications, as have other major central banks. The Chair testifies before Congress twice each year about the U.S. economy and the FOMC’s monetary policy in pursuit of its statutory goals of stable prices and maximum employment (figure 12).22 The Federal Reserve Board prepares a Monetary Policy Report to accompany that testimony.23 The Chair also holds press conferences after four FOMC meetings each year. The FOMC releases statements after its meetings that explain the economic outlook and the rationale for its policy decision. Detailed minutes of the Committee’s meetings are published three weeks later.24 Since 2007, FOMC participants have submitted quarterly macroeconomic projections that are published in the Summary of Economic Projections.25 In 2012, the FOMC issued a Statement on Longer-Run Goals and Monetary Policy Strategy, which is reaffirmed every January. This statement discusses the Committee’s interpretation of its statutory goals of maximum employment and price stability; it indicates that the Committee judges inflation of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, to be most consistent over the longer run with the Federal Reserve’s statutory mandate.26 Transcripts of FOMC meetings are released to the public after a delay of about five years.

Federal Reserve Board Governors and Reserve Bank Presidents contribute to the Federal Reserve’s transparency with frequent public speeches and other communications. I believe that support for the Federal Reserve as a public institution is sustained by the public expression of our diverse views.27

These communications with Congress and the public are critical parts of the Federal Reserve’s institutional accountability and transparency, and are essential complements to its independence. It is important that Federal Reserve officials regularly demonstrate that the Fed has been appropriately pursuing its mandated goals. Transparency can also make monetary policy more effective by helping to guide the public’s expectations and clarify the Committee’s policy intentions.

Recent Changes in Federal Reserve System Governance

In recent years, the governance of the Federal Reserve System has continued to evolve. The 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act provided that directors representing financial institutions–the class A directors, of which there are three on each Reserve Bank board–may not participate in the appointment of Reserve Bank presidents and first vice presidents. The Federal Reserve Board has long had policies preventing Reserve Bank directors from participating in supervisory matters or in determining the appointment of any Reserve Bank officer whose primary duties involve supervisory matters. These directors continue to provide highly valuable information about developments in their markets, and take part fully in other roles with the other six directors.

Another aspect of governance involves the better representation of women and minorities in the Federal Reserve System. Indeed, while I have focused my remarks on the history of geographical diversity in the Federal Reserve System, we also strive to have diversity in gender and race both at the Board and at the Reserve Banks. In recent years, the Reserve Banks’ boards of directors have made significant progress along these lines. Women now account for 34 percent of the directors, up from 24 percent five years ago. In addition, minorities now account for 29 percent of directors, up from 19 percent five years ago.

Conclusion

The long history of political discourse in the United States helps explain the Federal Reserve’s unique structure, in which the Board of Governors in Washington and the 12 regional Reserve Banks share power over monetary policy (as shown in figure 1). Throughout our history, Americans have questioned the structure and even, at times, the need for a central bank. Current discussions of Fed reforms echo these past debates. But it is important to understand that history in both advanced and emerging economies across the world has consistently demonstrated the need for a central bank, and both the existence and the structure of the Federal Reserve are products of that historical experience. Our structure is fundamentally a compromise, shaped by American history stretching back to the first Bank of the United States and, later, by the lessons of the Great Depression. It is designed to deliver the United States a vitally needed central bank in a country that has had a long-standing aversion to centralized power over monetary and financial affairs. It preserves diverse regional voices while ensuring that policy can be implemented through a cooperative consensus. The balance between national and regional interests is critical to the spirit of the original compromise that created the Federal Reserve, and to its democratic legitimacy. The structure achieves a practical balance that should not be changed lightly, as it continues to serve the country well.

ENDNOTES

1. My remarks today reflect my own views and not necessarily those of the Board of Governors of the Federal Reserve System or the Federal Open Market Committee. Return to text

2. The Bank of the United States became a net creditor to state banks by holding the notes issued by those banks. When it presented those notes for redemption, it could affect the funding position of state banks and effectively constrain credit in this manner. Return to text

3. See John H. Wood (2005), A History of Central Banking in Great Britain and the United States (New York: Cambridge University Press). Return to text

4. See Lance E. Davis (1965), “The Investment Market, 1870-1914: The Evolution of a National Market,” Journal of Economic History, vol. 25 (September), pp. 355-93. Economic historians have debated the extent to which interest rate differentials reflected market segmentation and supply versus demand in each market. Other factors include higher risk premiums, reflecting higher expected default rates in some areas of the country, and varying levels of monopoly power. Return to text

5. For a sense of the regionalism of this debate, believe it or not, The Wonderful Wizard of Oz has been interpreted as an allegory for 19th century regional monetary problems, though there is little evidence about the intentions of its author, L. Frank Baum, in conveying this allegory. Dorothy was from Kansas, a farm state, but after a cyclone, she found herself in a world dominated by gold, with a yellow brick road and the Land of Oz–the abbreviation for an ounce. The story has four witches–from the West, East, North, and South. Remember that the Wicked Witch of the West ultimately met her demise when she melted on contact with water, a symbol for the end of a drought that contributed to the economic hardships of western farmers. But the most powerful change was brought about by Dorothy’s shoes, which were originally owned by the Wicked Witch of the East. Importantly, these shoes were silver in the original book, not red as in the movie, symbolizing the power of bimetallism as a solution to western problems. See Hugh Rockoff (1990), “The ‘Wizard of Oz’ as a Monetary Allegory,” Journal of Political Economy, vol. 98 (August), pp. 739-60. Return to text

6. See Andrew J. Jalil (2015), “A New History of Banking Panics in the United States, 1825-1929: Construction and Implications,” American Economic Journal: Macroeconomics, vol. 7 (July), pp. 295-330. Return to text

7. Contemporaries blamed these crises on the seasonality in demand for currency and credit related to planting and harvesting of crops in the spring and fall. Modern scholars place more weight on other sources of financial tightness. Some point to poor harvests that depressed net exports, particularly failed cotton harvests. Net exports were an important source of increases in the money supply in this period. In the context of the gold standard, poor money supply growth in the United States triggered certain expectations by international capital market participants that interest rates in the United States would rise relative to the rest of the world. As a result, interest rates on American commercial paper (a key rate affected by international financial conditions) rose following poor harvests, stock and bond prices fell, and deposits flowed out of the New York banking system. Industrial production decreased as well, with a lag. This set of effects created tight financial conditions of the sort that could lead to financial crises. (See Christopher Hanes and Paul W. Rhode (2013), “Harvests and Financial Crises in Gold Standard America,” Journal of Economic History, vol. 73 (March), pp. 201-46.) Other scholars focus on business cycle downturns as creating conditions favorable to financial crises, as depositors viewed the downturns as affecting the solvency prospects of their banks, leading to withdrawals and panics. (See Gary Gorton (1988), “Banking Panics and Business Cycles,” Oxford Economic Papers, vol. 40 (December), pp. 751-81.) Return to text

8. See Walter Bagehot ([1873] 1897), Lombard Street: A Description of the Money Market (New York: Charles Scribner’s Sons). Return to text

9. See Nathan S. Balke and Robert J. Gordon (1989), “Appendix B: Historical Data,” in Robert J. Gordon, ed., The American Business Cycle: Continuity and Change (Chicago: University of Chicago Press), pp. 781-850. See also Jon R. Moen and Ellis W. Tallman (2015), “The Panic of 1907,” Federal Reserve History. Return to text

10. See Roger Lowenstein (2015), America’s Bank: The Epic Struggle to Create the Federal Reserve (New York: Penguin Press); and Allan H. Meltzer (2003), A History of the Federal Reserve, Volume 1: 1913-1951 (Chicago: University of Chicago Press). Return to text

11. As originally enacted, Section 10 of the Federal Reserve Act required that the President, in nominating Board members, “have due regard to a fair representation of the different commercial, industrial and geographical divisions of the country” (see Federal Reserve Act, ch. 6, § 10, 38 Stat. 260 (1913), p. 12, www.federalreservehistory.org/Media/Material/Event/10-58). In 1922, this representational requirement was expanded to its current form, which provides, in Section 10(1), that the President “have due regard to a fair representation of the financial, agricultural, industrial, and commercial interests, and geographical divisions of the country” (see Federal Reserve Act, 12 U.S.C. § 241 as amended by an act of June 3, 1922 (42 Stat. 620), paragraph on appointment and qualification of members, https://www.federalreserve.gov/aboutthefed/section%2010.htm). In addition, Section 10(1) provides that no two members of the Board may be from the same Reserve Bank District. Return to text

12. All national banks chartered by the Comptroller of the Currency are required to be members of the Federal Reserve System, and state-chartered banks may choose to become members. Return to text

13. Directors are chosen, according to Sections 4(11) and 4(12) of the Federal Reserve Act, “with due but not exclusive consideration to the interests of agriculture, commerce, industry, services, labor and consumers” (see Federal Reserve Act, 12 U.S.C. § 302 as amended by an act of Nov. 16, 1977 (91 Stat. 1388), paragraphs on class B and class C directors, https://www.federalreserve.gov/aboutthefed/section4.htm). Return to text

14. Authors Jeremy Atack and Peter Passell write, “Throughout much of American history there has been a deep and abiding mistrust of bankers and a widespread fear of a ‘money monopoly’–a fear that those needing to borrow would be taken advantage of by those able to lend. Such questions had figured prominently in the debates over the fates of the First Bank and Second Bank of the United States, and they played a role in the popular support of free banking legislation. They had also led to the almost universal adoption of usury ceilings on interest rates (typically 6 percent) that were more honored in name than reality. These concerns were the subject of congressional inquiries, the most famous of which were the Pujo hearings into the Money Trust in the wake of the 1907 panic.” See Jeremy Atack and Peter Passell (1994), A New Economic View of American History: From Colonial Times to 1940, 2nd ed. (New York: Norton), p. 510. See also Milton Friedman and Anna Jacobson Schwartz (1963), A Monetary History of the United States, 1867-1960 (Princeton, N.J.: Princeton University Press), p. 48. Return to text

15. See Carter Glass (1927), An Adventure in Constructive Finance (Garden City, N.Y.: Doubleday, Page). Return to text

16. For a discussion of these issues, see David C. Wheelock (2000), “National Monetary Policy by Regional Design: The Evolving Role of the Federal Reserve Banks in Federal Reserve System Policy,” in Jürgen von Hagen and Christopher J. Waller, eds., Regional Aspects of Monetary Policy in Europe (Boston: Kluwer Academic), pp. 241‑74. Return to text

17. The FOMC was created by the Banking Act of 1933 but was restructured in 1935 to include members of the Board of Governors. Return to text

18. The Federal Reserve Bank of New York was made a permanent member of the FOMC in 1942. From 1935 to 1942, it alternated annually with the Federal Reserve Bank of Boston as a member. Return to text

19. For a discussion of the Federal Reserve’s dual mandate, see the FOMC’s Statement on Longer-Run Goals and Monetary Policy Strategy, which the Committee first issued in January 2012 and reaffirms annually, in note 26. In addition, for a discussion of how the FOMC prepares for its meetings, see Elizabeth A. Duke (2010), “Come with Me to the FOMC,” speech delivered at the Money Marketeers of New York University, New York, October 19. Return to text

20. For a discussion of these issues, see Marvin Goodfriend (1999), “The Role of a Regional Bank in a System of Central Banks,” Carnegie-Rochester Conference Series on Public Policy, vol. 51 (December), pp. 51-71. Return to text

21. Ben Bernanke, former Chairman of the Federal Reserve Board, referenced the motto in a 2007 speech. See Ben S. Bernanke (2007), “Federal Reserve Communications,” speech delivered at the Cato Institute 25th Annual Monetary Conference, Washington, November 14. Return to text

22. The statutory mandate was added in the Federal Reserve Reform Act of 1977. Return to text

23. The Monetary Policy Report is available on the Board’s website at https://www.federalreserve.gov/monetarypolicy/mpr_default.htm. Return to text

24. FOMC statements and the minutes of FOMC meetings are available on the Board’s website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

25. Since 2012, the Summary of Economic Projections (SEP) has included each individual FOMC participant’s assessment of appropriate monetary policy in the form of an interest rate “dot plot.” The SEP is available on the Board’s website at https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm. Return to text

26. The most recent statement is available on the Board’s website at https://www.federalreserve.gov/monetarypolicy/files/fomc_longerrungoals.pdf. Return to text

27. See Jon Faust (1996), “Whom Can We Trust to Run the Fed? Theoretical Support for the Founders’ Views,” Journal of Monetary Economics, vol. 37 (April), pp. 267-83; Jon Faust (2016), “Oh, What a Tangled Web We Weave: Monetary Policy Transparency in Divisive Times,” Hutchins Center Working Paper 25 (Washington: Brookings Institution, November); and Jerome H. Powell (2016), “A View from the Fed,” speech delivered at “Understanding Fedspeak,” an event cosponsored by the Hutchins Center on Fiscal and Monetary Policy at the Brookings Institution and the Center for Financial Economics at Johns Hopkins University, Washington, November 30. Return to text

The preceding remarks were delivered by Jerome H. Powell, a member of the Board of Governors of the Federal Reserve System, on March 28, 2017, in Morgantown, West Virginia, at the West Virginia University College of Business and Economics Distinguished Speaker Series, on The History and Structure of the Federal Reserve. A copy of the remarks is available here.