Sky Blog

Sky Blog

On December 22, 2017, President Trump signed Public Law No. 115-97, formerly known as the “Tax Cuts and Jobs Act” (the “Act”), into law. The Act makes a number of major changes to the U.S. federal income taxation of both individual taxpayers and businesses, generally effective for taxable years beginning after December 31, 2017. A number of key considerations for private equity transactions arise as a result of the Act, including:

- Whether pass-through structures, including UP-C structures, continue to be advantageous,

- The new 30% limitation on deductibility of business interest expense,

- Potential changes to financing collateral packages,

- The value of transaction tax deductions and bonus depreciation, and

- The potential impact of the mandatory transition tax and GILTI.

In this, the first of a two-part article on these changes, we will discuss the first three topics.

Corporations vs. Pass-throughs; UP-C Structures

Choice of Entity

Historically, it was generally economically beneficial to hold portfolio companies in pass-through entities wherever possible. Portfolio companies structured as corporations for tax purposes were subject to taxation at the corporate level on any earnings of the corporation and again at the individual shareholder level on any dividends distributed by the corporation. In contrast, pass-through businesses were subject to only one layer of tax and often created significant value for equityholders at exit through delivery of a basis step-up to a buyer which resulted in increased purchase price. In addition, structures such as the UP-C, which enable a business held in an entity taxable as a partnership (the “operating partnership”) to use a C corporation to issue shares to the public in an initial public offering (“pubco”) while allowing the pre-IPO owners to continue to hold their interests in the business in pass-through form, were a common method to preserve pass-through treatment and provide additional payments to sponsors for corporate tax savings resulting from a tax basis step-up realized by pubco via tax receivable agreements (“TRAs”) discussed in more detail below. For these reasons, before the Act, pass-throughs were preferable to C corporations in nearly all cases. Based on significant changes in prevailing tax rates, however, sponsors must revisit this conventional wisdom and determine whether a C corporation structure is preferable to a pass-through structure for a particular investment.

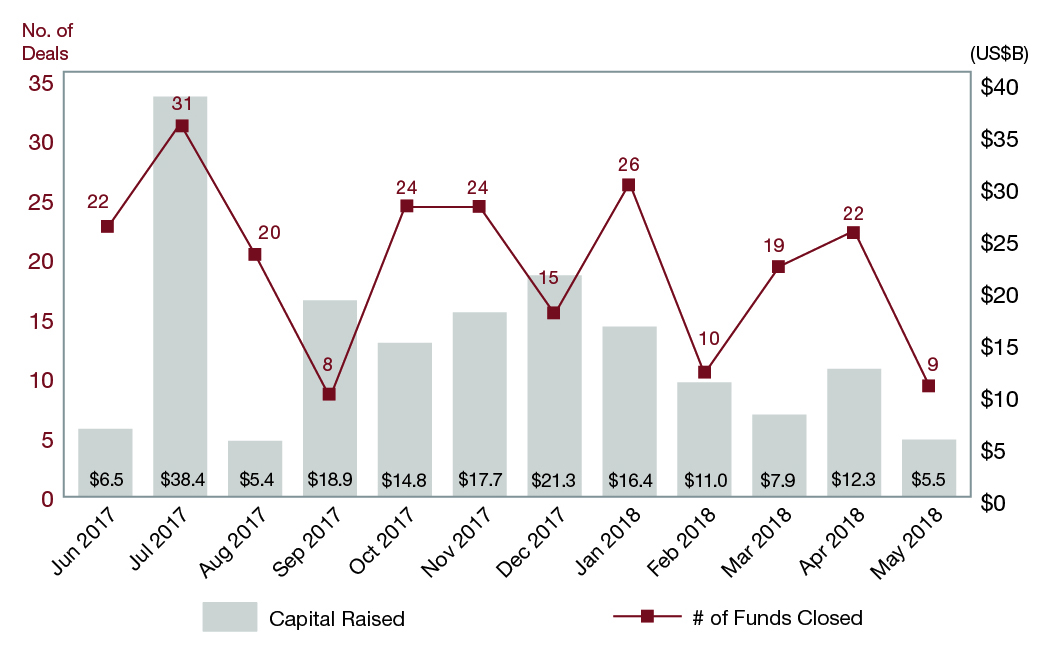

U.S Private Equity Fundraising:

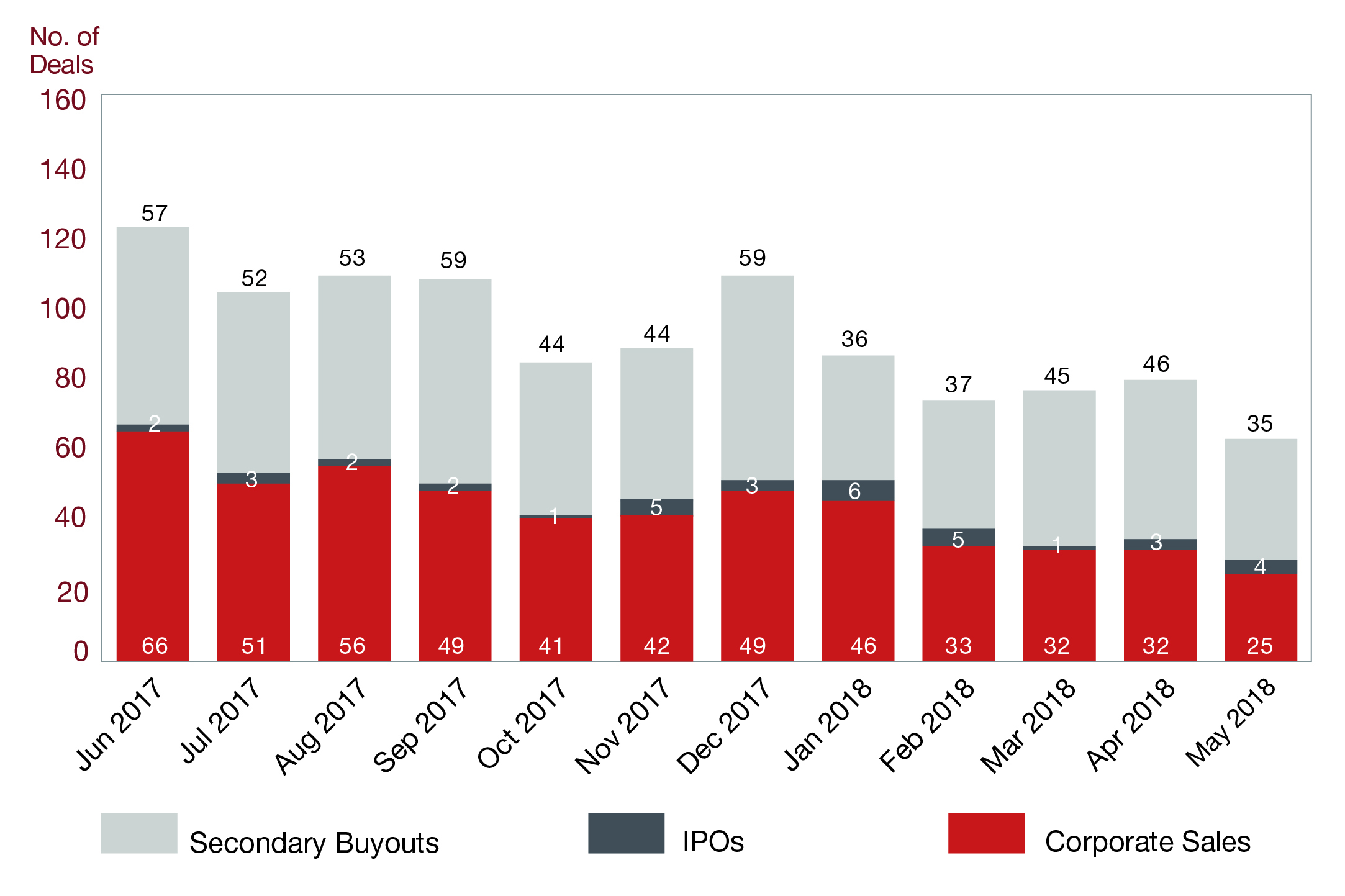

U.S. Sponsor Backed Exits by Number:

Before the Act, partnership income was taxed to individual partners at a top rate of 39.6%, and C corporations were taxed on their earnings at a top rate of 35%. Individual shareholders of a C corporation were then taxed again on dividends, generally at 23.8% (including the Medicare tax). Therefore, for a business that made cash distributions, an individual partner of a partnership was taxed at a rate of 39.6% instead of a ~50.5% rate as a shareholder of a C corporation.[1]

Under the Act, the top individual rate fell to 37%, though certain individuals may be able to take the pass-through deduction with respect to certain income described in further detail below. C corporations are taxed under the Act at a rate of 21%. Individual shareholders of a C corporation are taxed again on dividends, generally at a 23.8% rate. If the full pass-through deduction applies, for a business that makes current cash distributions of its earnings, an individual partner of a partnership is effectively taxed on partnership income at a rate of 29.6% instead of ~39.8% as a shareholder of a C corporation.[2] Therefore, for a business that makes current cash distributions of its earnings and that is owned by individuals eligible for the full pass-through deduction, pass-through structures continue to provide similar tax rate benefits to those under prior law. If the pass-through deduction does not apply, the difference between the rate of an individual partner of a partnership and an individual shareholder of a C corporation shrinks to 37% vs. ~39.8%.

Although the basis step-up delivered in a pass-through structure is less valuable to potential purchasers as a result of the lower corporate rate under the Act (but see discussion regarding immediate expensing for qualified property, which we will discuss next time), the ability to deliver a basis step-up on exit, including monetization of such step-up through the use of TRAs, will continue to be an advantage of pass-through structures. For example, in UP-C structures, the pre-IPO owners’ interests in the operating partnerships are typically exchangeable for pubco shares. Upon such an exchange, the pubco obtains a step-up in the tax basis of its proportionate share of the assets of the operating partnership the depreciation and amortization of which reduces future tax liability of the pubco. It is typical for the pubco to enter into TRAs with exchanging pre-IPO owners to share the tax savings generated from the basis step-up resulting from an exchange, and we expect TRAs to remain a common arrangement.

Deal Implications: The potential purchase price or TRA benefit at exit available in a pass-through structure must now be weighed against the increased ability to generate additional post-tax cash flow on a current basis in a corporate structure, based on the spread in corporate and individual rates. A corporate structure could be particularly appealing for businesses that do not currently distribute cash. For example, if excess cash is intended to be reinvested in the business or used to pay down debt for the foreseeable future, the benefits of incorporation may outweigh the double layer of tax and inability to monetize a basis step-up at exit.

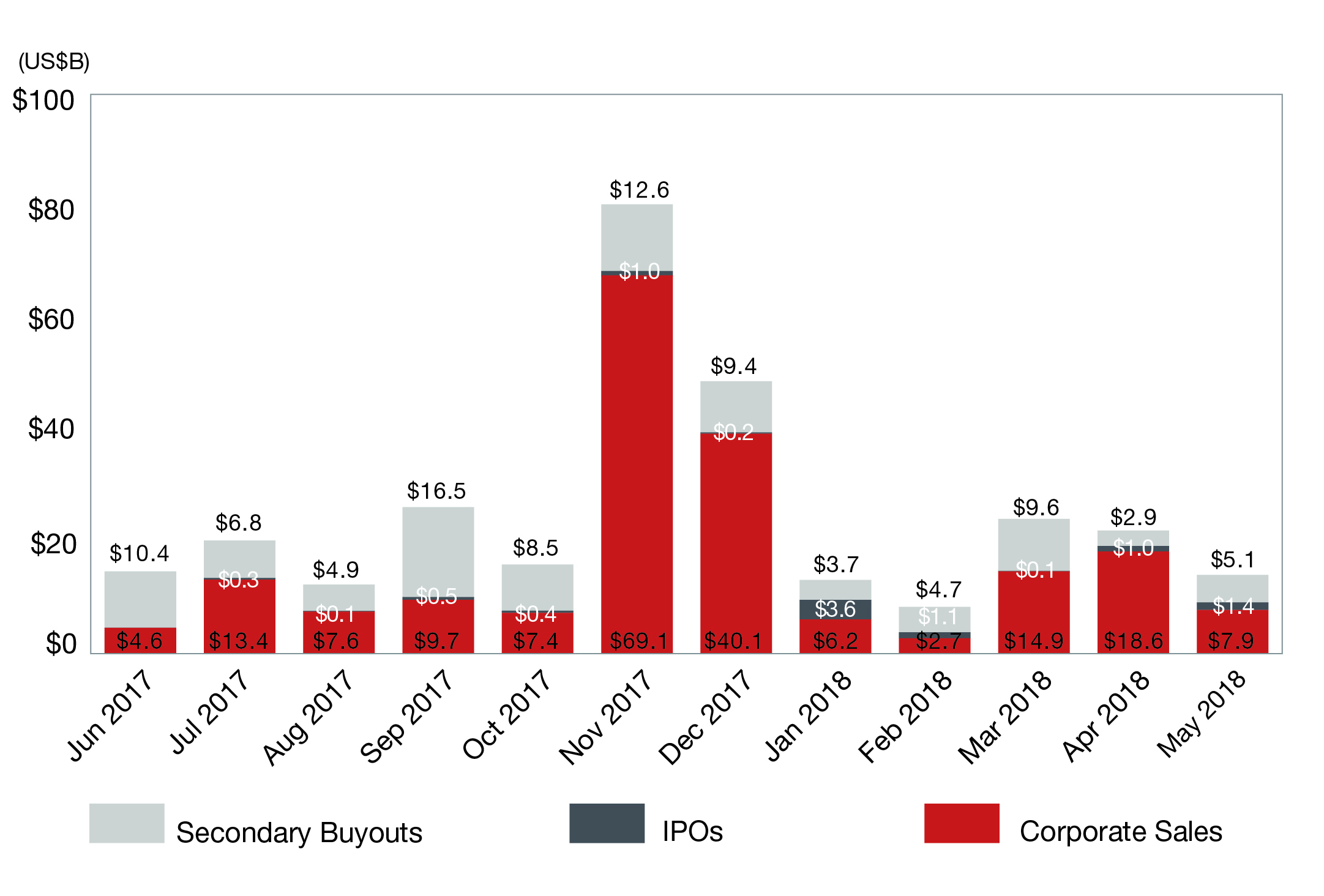

U.S. Sponsor Backed Exits by Dollar Volume:

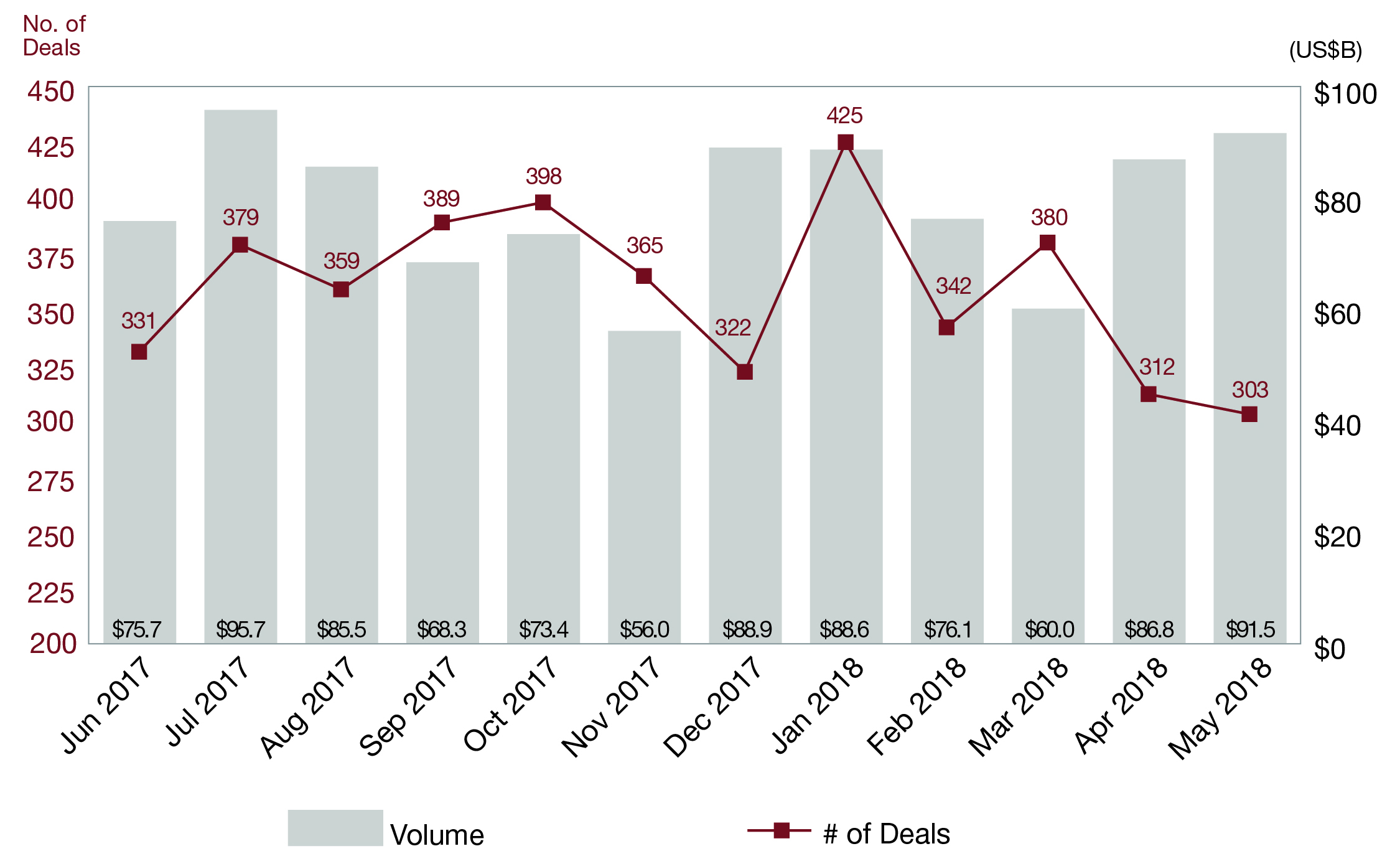

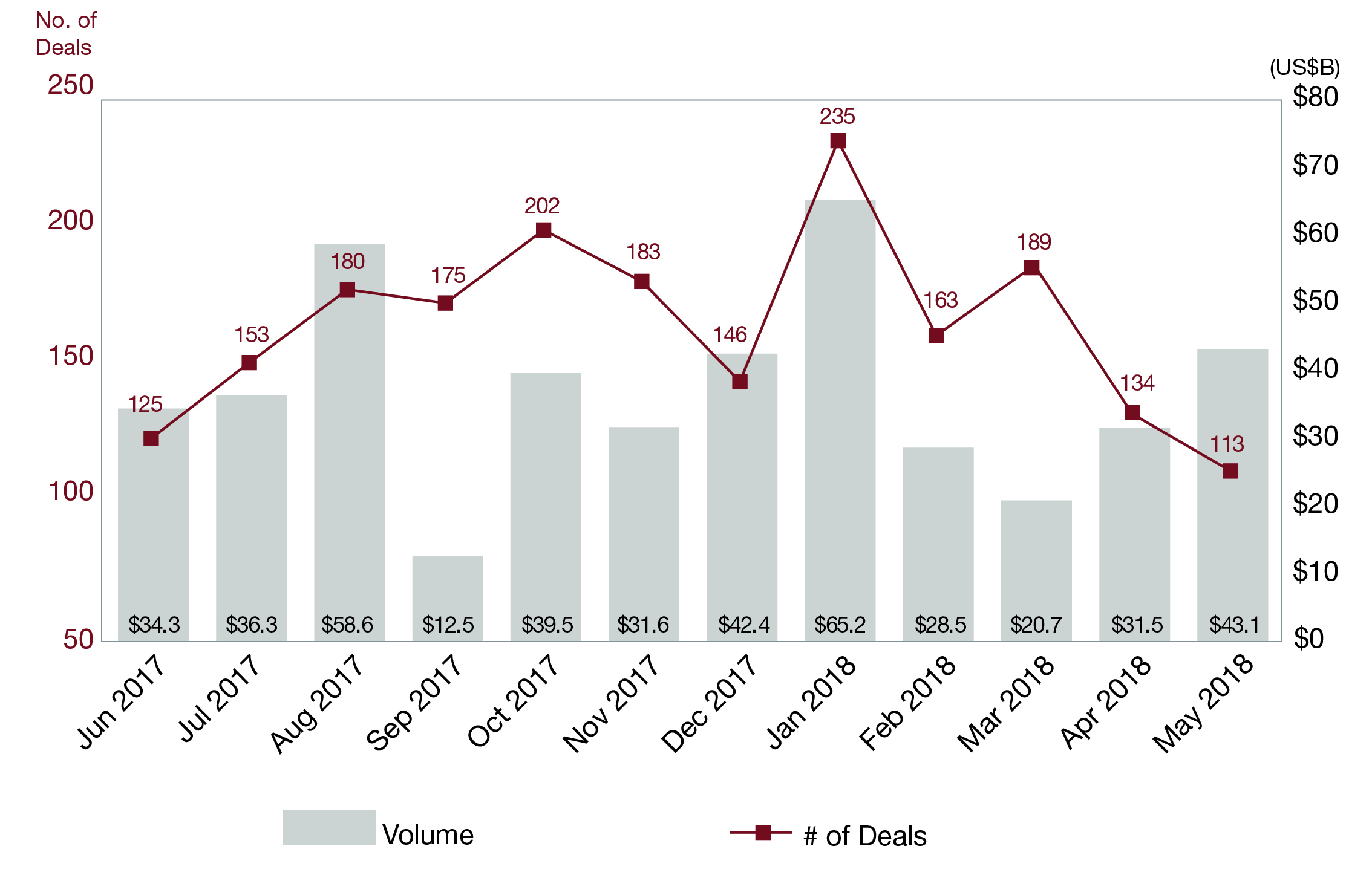

Global Sponsor-Related M&A Activity:

U.S. Sponsor-Related M&A Activity:

Pass-Through Deduction

Determining the right form of entity now requires significant and detailed modeling, taking into account the availability of the new pass-through deduction for pass-through businesses. Under the Act, individuals, trusts and estates may now deduct up to 20% of domestic “qualified business income” received from partnerships and other pass-through entities. The federal income tax rate for a pass-through business that is eligible for the maximum deduction would be 29.6%, which more closely aligns with the corporate rate. However, significant uncertainty surrounds the application and availability of this deduction.

“Qualified business income” generally includes items of income, gain, deduction and loss with respect to a business operated in the United States in pass-through form, but does not include amounts received as reasonable compensation, amounts received as guaranteed payments for services or investment income. Other limitations on the pass-through deduction apply, including limitations based on wages paid and property owned by the business, and the deduction is not available for income realized from “specified service trades or businesses” such as health, law, accounting, consulting, financial services firms and other businesses where the principal asset of such trade or business is the reputation or skill of one or more of its employees. The availability of this deduction is tested on a business-by-business basis, which could result in different tax rates for different portions of a portfolio company’s operations.

Deal Implications: Significant open issues remain which may be addressed in future guidance, but, in the meantime, it is difficult for sponsors to model the appropriate tax rate for new pass-through deals and to determine appropriate tax distribution rates for existing investments.

Financing

Limitations on Interest Deductibility

The Act generally limits a business’s net interest deductions to 30% of the business’s “adjusted taxable income,” and there are no transition rules or grandfathering of existing debt. “Adjusted taxable income” is similar to EBITDA for taxable years beginning before January 1, 2022, and similar to EBIT thereafter. Disallowed interest expense can be carried forward indefinitely, subject to the ownership change limitations applicable to NOLs under Section 382.

Deal Implications: Borrowers may have to model more extensively than they are accustomed in order to take into account the new interest limitation. Leveraged companies that historically have paid very little U.S. federal income tax need to determine whether their tax liability will increase significantly as a result of the new limitation. In particular, any modeling will need to take into account the further limitation to 30% of EBIT beginning in 2022.

Any excess carryforward is carried forward as a separate asset. Similar to a net operating loss, this asset can be acquired by a potential buyer (subject to similar change of control rules that apply to NOLs). Sponsors could consider taking into account the value of the carryforward of disallowed interest expense on exit.

In Part II of this article, we will discuss the value of transaction tax deductions and bonus depreciation post-Act and the potential impact of the mandatory transition tax and GILTI.

Foreign Subsidiary Credit Support for U.S. Parent Debt

Current law, like the law prior to the Act, continues to treat collateral support by a “controlled foreign corporation” (a “CFC”) to debt of a related U.S. borrower as a “deemed dividend” includable in income of a 10% U.S. shareholder. However, the Act does move towards a partial “territorial” regime, providing a 100% dividends received deduction for actual dividends from foreign corporations to 10% U.S. corporate shareholders. As a result, from a U.S. tax perspective, a foreign corporation could pay dividends to its U.S. parent tax-free, but may not be able to make a loan to the U.S. parent or guarantee the U.S. parent’s obligations in a tax-efficient manner.

Deal Implications: Sponsors could explore, or lenders could push, to add foreign subsidiaries to collateral packages as guarantors or offering pledges of 100% of the stock of such entities. Such an expansion could be beneficial to U.S. borrowers, if interest would be deductible in the U.S., and the additional collateral would improve the pricing of the borrowing and could be accommodated from a U.S. tax perspective, if the foreign subsidiary is able to make current year distributions to its U.S. parent to eliminate potential phantom income issues. However, non-U.S. withholding taxes, non-U.S. limitations on the declaration of dividends or practical issues around securing foreign pledges and guarantees may limit the usefulness of this approach. In addition, given the 30% interest deductibility limitation discussed above, it may be more beneficial to borrow directly in non-U.S. jurisdictions with higher tax rates than to increase borrowing in the U.S. which may not be deductible.

ENDNOTES

[1] The C corporation was first taxed on its earnings at a 35% rate, and the individual shareholder was taxed on cash distributions of the 65% post-tax amount at a 23.8% rate (65% x 23.8% = ~15.5%).

[2] Under current law, the C corporation is first taxed on its earnings at a 21% rate, and the individual shareholder is taxed on cash distributions of the 79% post-tax amount at a 23.8% rate (79% x 23.8% = ~18.8%).

This post comes to us from Paul, Weiss, Rifkind, Wharton & Garrison LLP. It is based on the firm’s memorandum, “Key Considerations for Private Equity Transactions Resulting from New Tax Law – Part I,” dated June 2018 and available here.