Sky Blog

Sky Blog

On October 23, 2020, the International Swaps and Derivatives Association, Inc. (ISDA) published its IBOR Fallbacks Protocol (Protocol) and Supplement to the 2006 ISDA Definitions (Supplement) in anticipation of the expected discontinuation of the London Interbank Offered Rate (LIBOR) at the end of 2021. ISDA has also published a related set of Frequently Asked Questions, as well as a User Guide to IBOR Fallbacks and RFRs, to assist market participants in navigating the Protocol and the Supplement.

ISDA collaborated with the Financial Stability Board’s Official Sector Steering Group to devise more robust fallbacks for LIBOR and other key interbank offered rates (IBORs) in its standard documentation for interest rate derivatives. The Protocol and the Supplement will facilitate inclusion of consistent triggers and hardwired fallbacks in new and existing non-cleared derivatives transactions that will apply if an IBOR they reference is either permanently discontinued (Cessation Event) or — with respect to LIBOR in particular — determined in a pre-cessation announcement by the UK Financial Conduct Authority (FCA) to have become non-representative of its underlying market (Pre-Cessation Event). The new fallback waterfalls include fallbacks to term- and spread-adjusted versions of the risk-free rates (RFRs) identified as alternatives to LIBOR and other IBORs in the relevant jurisdictions.

While use of the Protocol and the Supplement is voluntary, and counterparties are free to seek their own bilateral solutions, the ISDA solutions should give derivatives market participants (as well as those in related loan and bond markets) much-needed standardization and certainty in the final stages of the transition away from LIBOR. According to ISDA, 257 entities across 14 jurisdictions had already adhered to the Protocol on a binding (but previously non-public) basis in the two-week pre-launch “escrow” period, and a publicly available list of adhering parties is available on the ISDA website. As Latham & Watkins has noted, regulators and working groups in both the US and the UK have strongly encouraged market participants from all sectors to sign and adhere to the Protocol. However, the Protocol is not a one-stop solution for all market participants, and will need to be carefully considered by buy-side counterparties in close coordination with their underlying loan and financing floating rate exposures. Market participants that choose not to adhere to the Protocol will need to take robust alternative measures (including bilateral amendments or closing out of positions) to manage risk and avoid disruption.

Relevant IBORs, Cessation and Pre-Cessation Events, and the Fallback Waterfall

The Protocol and the Supplement provide new triggers and fallbacks with respect to a range of “Relevant IBORs.”

Relevant IBORs

For purposes of the Protocol and the Supplement, Relevant IBORs include LIBOR (with no reference to, or indication of, the currency of such LIBOR), US Dollar LIBOR, UK Sterling LIBOR, Swiss Franc LIBOR, Euro LIBOR, the Euro Interbank Offered Rate, the Japanese Yen LIBOR, the Japanese Yen Tokyo Interbank Offered Rate, the Euroyen Tokyo Interbank Offered Rate, the Australian Bank Bill Swap Rate, the Canadian Dollar Offered Rate, the Hong Kong Interbank Offered Rate, the Singapore Dollar Swap Offer Rate, and the Thai Baht Interest Rate Fixing.

Cessation and Pre-Cessation Events

While existing fallback provisions typically address only the temporary unavailability of a reference rate, both the Protocol and the Supplement provide further fallbacks that will apply either upon a Cessation Event (i.e., an IBOR is permanently discontinued) or with respect to LIBOR only, in the case of a Pre-Cessation Event.

For all Relevant IBORs, the fallback provisions of the Protocol and the Supplement will be triggered by the permanent cessation of such rate (i.e., a Cessation Event), which will occur upon either of the following occurrences:

- A public statement or publication of information by or on behalf of the administrator of the relevant IBOR (Relevant Administrator) announcing that such Relevant Administrator has ceased, or will cease, to provide the relevant IBOR permanently or indefinitely, provided that, at that time, there is no successor administrator that will continue to provide the relevant IBOR

- A public statement or publication of information by (i) the regulatory supervisor for the Relevant Administrator, (ii) the central bank for the currency of the relevant IBOR, (iii) an insolvency official with jurisdiction over the Relevant Administrator, (iv) a resolution authority with jurisdiction over the Relevant Administrator, or (v) a court or an entity with similar insolvency or resolution authority over the Relevant Administrator, in each case, which states that the Relevant Administrator has ceased or will cease to provide the relevant IBOR permanently or indefinitely, provided that, at that time, there is no successor administrator that will continue to provide the relevant IBOR

In addition, and with respect to LIBOR only, the Protocol and the Supplement provide for a pre-cessation trigger. Such a Pre-Cessation Event will occur upon a public statement from the FCA announcing that such rate is, or will no longer be, representative and that such statement is being made in the awareness that its effect will be to engage certain contractual triggers for fallbacks activated upon pre-cessation announcements by the FCA.

The Fallback Waterfall

Rather than provide a single fallback for each Relevant IBOR, the Protocol and the Supplement provide a waterfall of successive fallback provisions, accounting for the possibility that a single fallback rate may be discontinued in the future.

With that said, the primary fallback rates to be applied under the Protocol and the Supplement upon a Cessation or Pre-Cessation Event for a Relevant IBOR are adjusted versions of the RFRs identified by relevant supervisors and regulators as alternatives to IBORs. Each such fallback rate is made up of a term-adjusted RFR, plus a spread. With the exception of the Singapore Dollar Swap Offer Rate and the Thai Baht Interest Rate Fixing, all such fallback rates will be published by Bloomberg Index Services Limited. If such fallback rates are themselves permanently discontinued, then the Protocol and the Supplement will provide further fallback provisions.

The Supplement also provides revised fallbacks in the event that a Relevant IBOR is temporarily unavailable. Previously, fallbacks for the temporary unavailability of rates typically have relied on quotations from reference banks. Going forward, in the event of temporary unavailability of a rate on a specified price source, the fallbacks under the Supplement provide that (i) the parties shall use the rate provided by an authorized distributor or the Relevant Administrator itself and (ii) if neither an authorized distributor nor the Relevant Administrator publish a rate, then the rate formally recommended for use by the Relevant Administrator for such Relevant IBOR will apply. Again, there are then further fallbacks.

The Supplement and Fallbacks on a Go-Forward Basis

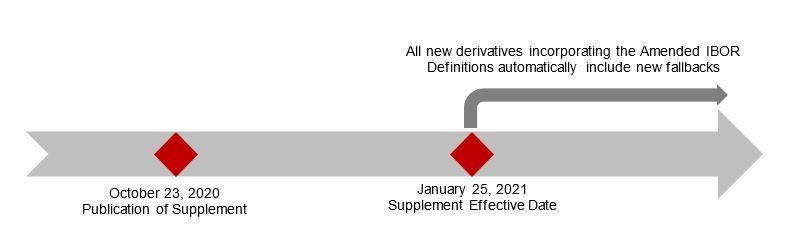

The Supplement incorporates these fallback provisions into the floating rate options that reference Relevant IBORs in the 2006 and 2000 ISDA Definitions and other relevant ISDA definitional booklets (IBOR Definitions). Although already publicly available, the Supplement is deemed to be published and effective on January 25, 2021 — i.e., the same date the Protocol becomes effective (Effective Date). Accordingly, all new derivatives transactions that incorporate IBOR Definitions and that are entered into on or after that date will automatically include the updated Cessation Events, Pre-Cessation Events, and fallbacks as part of the IBOR Definitions, as amended by the Supplement (Amended IBOR Definitions).

That is, new ISDA Master Agreements negotiated after the Effective Date and which incorporate the Amended IBOR Definitions in the Schedule will have the new Cessation Events, Pre-Cessation Events, and fallbacks included in their terms as a result of the Supplement. In addition, the Protocol will amend any ISDA Master Agreement that (i) is already in place between two adhering parties as of the Effective Date and (ii) incorporates the IBOR Definitions, to apply the Supplement to all new transactions thereunder going forward. However, if new transactions are entered into after the Effective Date under an ISDA Master Agreement that does not incorporate the Amended IBOR Definitions, transacting parties will be able to incorporate the Amended IBOR Definitions into the relevant confirmation in order to include the Supplement’s new fallback provisions.

The Protocol and Legacy Contracts

The Protocol allows market participants to amend the terms of their legacy derivatives contracts to include these new Cessation Events, Pre-Cessation Events, and fallbacks. The Protocol is open to adherence by all entities, regardless of ISDA membership or domicile. Adherence is public, and the names of adhering entities are published on the ISDA website upon adherence.

Entities may adhere either individually in their own capacity or as agents on behalf of clients. In an individual capacity, a market participant can adhere to the Protocol by executing and submitting a form adherence letter to ISDA. For entities that are not ISDA Primary Members, there is no fee for adherence letters submitted prior to the Effective Date. Thereafter, and at all times for ISDA Primary Members, there is a one-time fee of US$500 upon submission of an adherence letter. Additional steps are necessary if an agent adheres on behalf of clients.

Which Legacy Contracts Are Amended?

The Protocol operates to amend the terms of legacy contracts (Protocol Covered Documents) to include the new Cessation Events, Pre-Cessation Events, and fallbacks, if such master agreement, credit support document, or confirmation, as applicable, references a Relevant IBOR and incorporates one of the following Covered ISDA Definitions Booklets (among other specified conditions):

- 2006 ISDA Definitions

- 2000 ISDA Definitions

- 1998 ISDA Euro Definitions

- 1998 Supplement to the 1991 ISDA Definitions

- 1991 ISDA Definitions

Protocol Covered Documents comprise not only ISDA-published master agreements (e.g., the 1992 and 2002 forms of the ISDA Master Agreement) and credit support documents (i.e., an ISDA Credit Support Annex or Credit Support Deed), but also certain other forms of master agreements and credit support documents enumerated in an annex to the Protocol.

The Protocol does not apply to documentation governing centrally cleared derivatives transactions, nor does it apply to any agreement in which the parties expressly provide that the terms of the Protocol do not apply.

When Will Protocol Amendments Become Effective?

In order to understand how and when the Protocol will amend the terms of Protocol Covered Documents, it is important to distinguish two events: (i) the formation of an agreement to amend as between adhering parties and (ii) the actual amendment of legacy contracts pursuant to that agreement.

Adherence and the Formation of an Agreement

In the terminology of the Protocol, the former event — i.e., the agreement between contracting parties to make the amendments contemplated by the Protocol — is effective on the Implementation Date. If neither party acts as an agent, the Implementation Date is the date of acceptance by ISDA of the later of the parties’ respective adherence letter submissions. The Implementation Date will vary in circumstances involving adherence by an agent depending on the method of adherence employed by the agent.

Timing of Legacy Contract Amendments

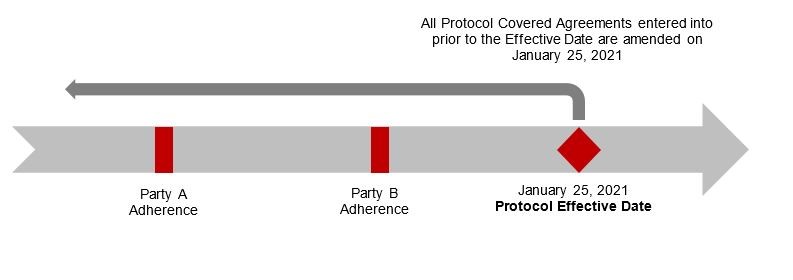

Pursuant to the terms of the Protocol, the actual amendment of the terms of those legacy contracts that constitute Protocol Covered Documents occurs on the later of (i) the Implementation Date and (ii) the Effective Date. In each case, the amendments are made to all Protocol Covered Documents entered into before the Effective Date (or, if later, the date of acceptance by ISDA of an adherence letter from the later of the two parties to adhere). This results in a number of potential scenarios.

If Party A and Party B both adhere to the Protocol before the Effective Date, amendment will occur on the Effective Date and will extend to the terms of all Protocol Covered Agreements entered into prior to such Effective Date.

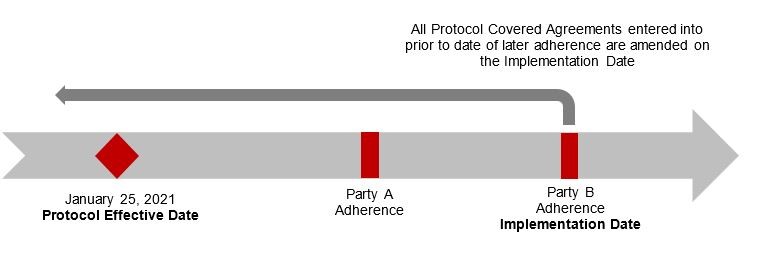

On the other hand, if Party A and Party B both adhere to the Protocol after the Effective Date, amendment will occur on the Implementation Date. As of the Implementation Date, the Protocol will operate to amend the terms of all Protocol Covered Documents entered into by Party A and Party B before the date of acceptance by ISDA of an adherence letter from the later of the two parties to adhere (i.e., the Implementation Date).

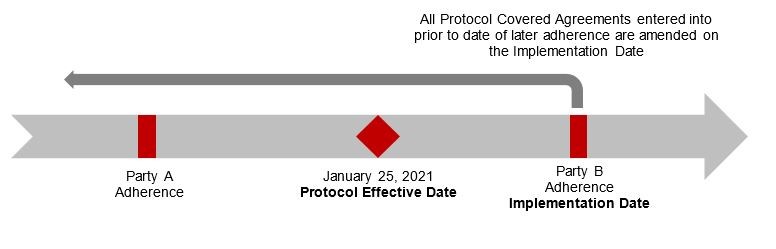

If Party A adheres to the Protocol before the Effective Date and Party B adheres after the Effective Date, amendment will occur on the Implementation Date, since it is later than the Effective Date. As of the Implementation Date, the Protocol will operate to amend all Protocol Covered Documents entered into by Party A and Party B before the date of acceptance by ISDA of the adherence letter from Party B, being the later of the two parties to adhere.

Revocation of Adherence

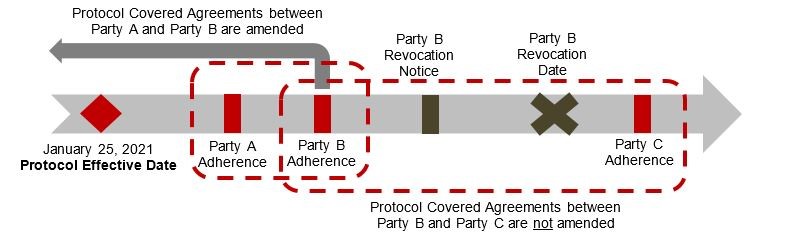

Adherence to the Protocol is irrevocable, but a party (Revoking Party) that has adhered to the Protocol may designate a “Revocation Date” by submitting a prescribed form of notice. The Revocation Date will be the last Protocol Business Day (i.e., a day following the Effective Date on which commercial banks and foreign exchange markets are generally open to settle payments in both London and New York) of the calendar month following the calendar month in which the Revoking Party delivers the requisite notice to ISDA.

Designation of a Revocation Date does not have any effect on amendments to Protocol Covered Documents in respect of which both adhering parties adhered prior to the Revocation Date. However, the Protocol will no longer operate to amend Protocol Covered Documents between the Revoking Party and a party that subsequently adheres after the relevant Revocation Date.

For example, if Party A and Party B both adhere to the Protocol after the Effective Date and Party B subsequently designates a Revocation Date, the Protocol would still operate to amend Protocol Covered Agreements between Party A and Party B. However, if Party C subsequently adheres to the Protocol after the Revocation Date designated by Party B, the Protocol would not amend Protocol Covered Agreements between Party B and Party C.

The Protocol and Partial Forward-Looking Effects

As a matter of generality, it is tempting to conclude that the Protocol retroactively addresses “legacy contracts” and the Supplement prospectively addresses new derivatives transactions entered into after the Effective Date. However, this is an oversimplification. Notably, the Protocol also has some forward-looking effects. For example, because the Protocol will operate to amend a legacy ISDA Master Agreement and the Schedule thereto (as a Protocol Covered Document), the triggers and amendments incorporated therein by doing so may extend to subsequent transactions entered into under that overall agreement, depending on the drafting of the Confirmations.

What the Protocol Doesn’t Do: Key Considerations for the Buy-Side in Understanding the Impact on Underlying Exposures

The Protocol does not ensure that a borrower’s underlying floating rate exposures from a financing align or transition at the same time as the terms of transition set forth in the Protocol for interest rate derivatives entered into to hedge such underlying floating rate exposure. That is, the Protocol is not a one-stop shop for borrowers and other buy-side participants that have hedged their underlying floating rate exposures with interest rate derivatives. Market participants should work closely with counsel and financial advisors to ensure that they fully appreciate and consider both the legal and economic consequences of adherence and the effect of adherence on any underlying or offsetting exposures and, when relevant, have considered IBOR transition strategies with their counterparties.

This post comes to us from Latham & Watkins. It is based on the firm’s memorandum, “Understanding the ISDA IBOR Fallbacks Protocol and Supplement: Summary and Takeaways for the Market,” dated November 6, 2020, and available here.