Sky Blog

Sky Blog

Beyond the extraordinary human toll it continues to exact, the coronavirus has thrown a pall of uncertainty over hundreds of corporate transactions that were signed and waiting to close at the pandemic’s onset. As we noted in our previous Blue Sky Blog post, an important factor for understanding the fate of these deals is the structure and scope of their force majeure provisions, known in transactional jargon as MAC/MAEs (henceforth ‘MAEs’). Our analysis utilized text analysis tools to evaluate historical data of MAEs in a population of M&A deals spanning more than a decade and a half (January 2003 – March 2018). Readers interested in reviewing our initial results or additional background information should refer to that original post.

Because our prior analysis made use of historical data from an unrelated project, it did not permit us to look directly into the estimated half-trillion dollars’ worth of pending transactions that are currently waiting to close. Fortuitously, however, multiple shelter-in-place mandates have materially shocked our own opportunity costs of time; and we made use of the current lull to update our data set (reluctantly forgoing other worthy pursuits). In this follow-up post, we present results from an extended data set, now spanning 2003 through March 20, 2020 (and consisting of 1702 announced transactions).

We focused our instant data collection efforts on transactions announced after the end point of our original sample (March 2018), limiting our query (as before) to deals with transaction values exceeding $100 million. Our primary source for candidate deals (FactSet) rendered 745 such transactions over that time span, including several for which transaction documents were not publicly available. From this group, we located the definitive agreements and MAE terms for 574 announced deals. In turn, this subgroup includes just under 80 pending deals signed since October 1, 2019 and representing over $250 billion in value. (There are also well over 200 more pending transactions with no filed deal documentation as of this writing).

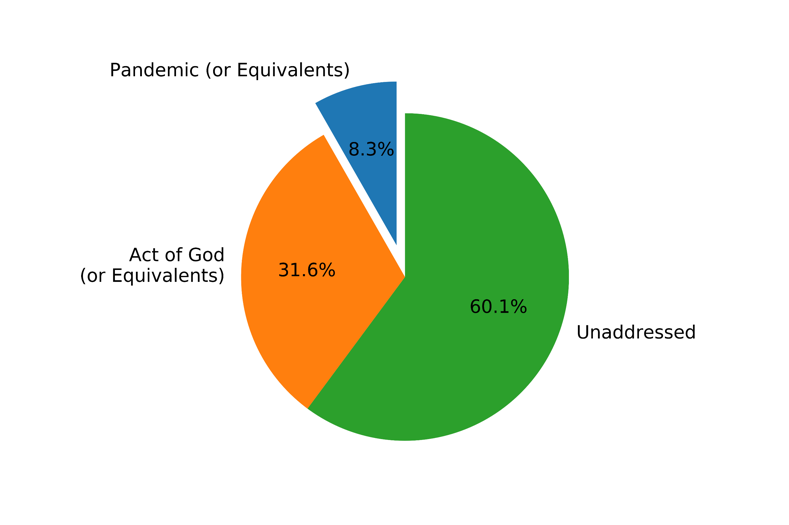

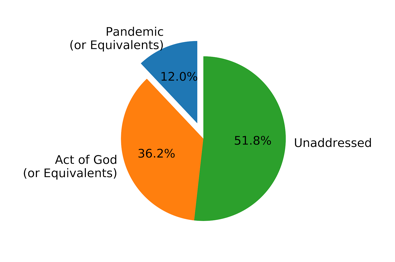

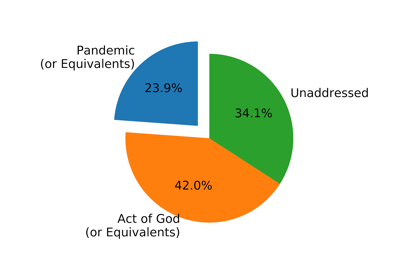

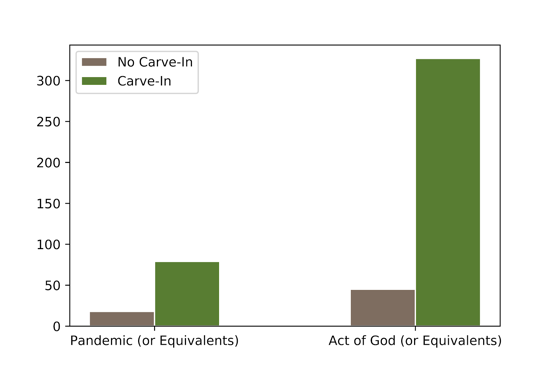

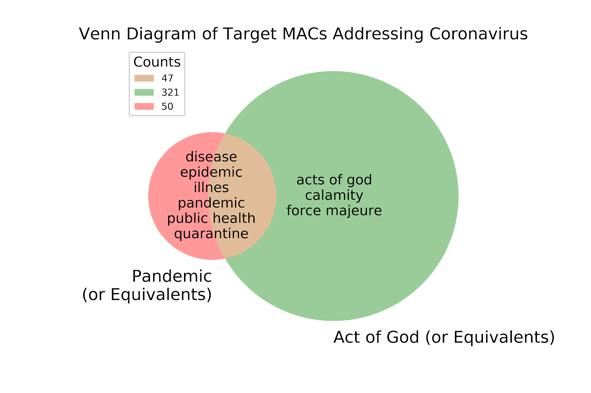

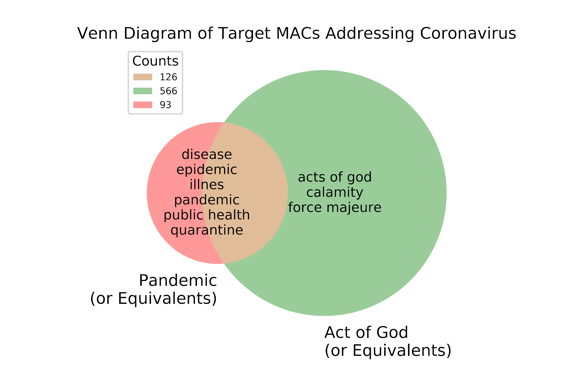

A key area of inquiry in our prior post was the fraction of MAE provisions that either (a) explicitly carve out “pandemics” (and semantic equivalents) or (b) arguably do so using general language (such as “act of god”). Our original post’s breakdown is reproduced in the left panel of the figure below; the center panel reflects our full updated data set in its totality; and the right panel reflects currently-pending deals.

|

|

|

| A. Original Data Set (2003-18) | B. Updated Data Set (2003-Pres.) | C. Currently Pending Deals |

As the sequence of panels illustrates, both explicit and general carve-outs have grown to comprise a larger share of MAEs in our updated data set: Fully 12% of deals overall carve out pandemic (or pandemic-like) contingencies explicitly, and just over 36% provide general carve-outs (compared with 8% and 32%, respectively, in our original analysis). The burgeoning role of carve-outs is even more pronounced in pending deals, where explicit and general carve-outs account for 24% and 42% of the MAEs, respectively. Significantly, and in stark contrast to our original post, fewer than 40% of provisions have neither type of carve-out.

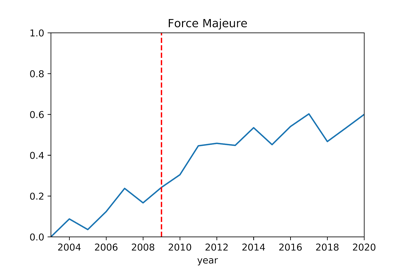

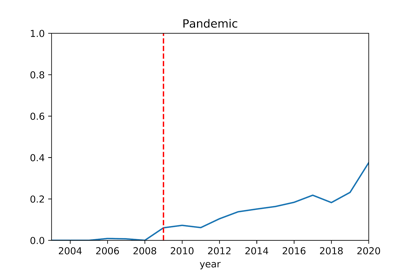

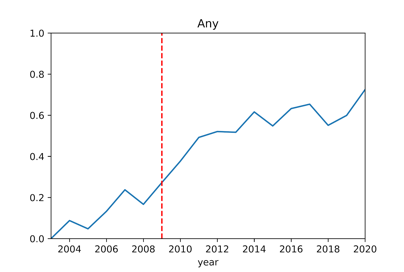

Digging a little deeper, it becomes evident that the shift in carve-outs betrays a longer trend whose seeds were sown over a decade ago. The time series charts below track the year-by-year prevalence of general carve-outs (left panel), pandemic-specific carve-outs (center panel), and their union (right panel) since 2003. General force majeure carve-outs became significantly more prevalent around 2009 − coinciding with the emergence from the great recession (well, at least the last one). But note that pandemic-specific carve-outs also started to go viral at around the same time (having been virtually non-existent prior to 2009). Although global economic conditions had much to do with the rapid adoption of general force majeure language, the pandemic-specific trend was more likely a byproduct of the contemporaneous H1N1 crisis that unfolded during the spring of 2009. And this fraction continued to rise through the two waves of the MERS crisis (first in 2012 and then again in 2015). By 2019, fully 23% of deals specifically carved out pandemics from coverage in the MAE.

|

|

|

| A. General Carve-Outs | B. Pandemic-Explicit Carve-Outs | C. General or Explicit Carve-Outs |

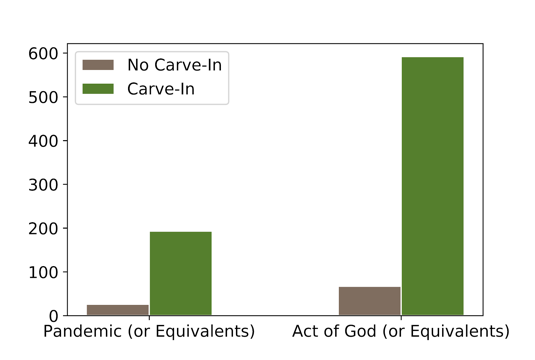

As we noted in our previous post, carve-outs (both general and pandemic-specific) come with a sizable grain of lawyerly salt: for even as they purportedly exempt a laundry list of enumerated risks, most carve-outs proceed to carve back in aspects of those same risks through “disproportional effects” language − whereby an excluded contingency still counts as a force majeure if the target suffers hardships that are disproportionate to those of its industry peers. Although we are still in the process of identifying all such carve-ins in the new data (whilst continuing to shelter in place), preliminary analysis suggests that carve-in patterns have largely remained stable. The figure below measures the prevalence with which MAE terms invoke a “disproportional effects” modifier after an enumerated carve-out. The left panel represents our original data, while the right panel illustrates our full data set of deals from 2003-present. The relationships appear highly comparable; if anything, disproportional effects carve-ins appear to be mildly more prevalent in the updated data set than in our original data set. Thus, while carve-outs have no doubt become more prevalent over time, a portion of their impact has been blunted mechanically by carve-ins that are typically riding shotgun.

|

|

| A. Disproportional Effects Carve-In Original Data Set (2003-18) | B. Disproportional Effects Carve-In Updated Data Set (2003-Pres.) |

On a related front, our prior post documented that when a pandemic-specific carve-out is invoked in an MAE, it is accompanied about 50% of the time by a general provision (such as “act of god;” see left panel below). The overlap between specific and general carve-outs has also mutated somewhat in recent years. Of the MAE definitions in the deals of our updated data set that have a pandemic-specific carve out, 57% are also chaperoned by more general force-majeure language. This observation suggests that when pandemic-specific language is invoked, it is increasingly being used to exemplify a general carve-out rather than as an independent, stand-alone risk.

|

|

| A. Original Data Set (2003-18) | B. Updated Data Set (2003-Pres.) |

Although it is easy to get caught up in the semantic structure of MAE provisions (and the three of us are admittedly hip deep), it is important not to lose sight of the broader institutional setting that frames these disputes. Some relevant considerations include the following:

- Judicial Reticence. By any account, common-law courts aren’t pushovers when it comes to nullifying contractual obligations. Contract law has long resisted the temptation to rescue a regretful party once foundational risk allocation decisions seem locked in. This canonical attribute of contract law carries over to M&A, too: for at least two decades, Delaware courts have consistently held that buyers wishing to bail out of a deal “ought to have to make a strong showing to invoke a Material Adverse Effect”.

- Burdens of Proof. Consistent with the foregoing view, MAEs are generally interpreted by courts to constitute conditions subsequent to the obligation to close (rather than as conditions precedent, as many often mis-label them). The key upshot of this designation is that the initial burden of proof to invoke an MAE rests squarely on the shoulders of the party alleging excuse (almost always the buyer). And if the underlying evidentiary case is unclear, or if competing arguments produce an approximate stalemate on the merits, then the case is resolved in favor of the party seeking enforcement of the contract (usually the seller).

- Durational Significance. One of the few consistent lodestars in existing MAE jurisprudence is that the target’s unanticipated hardship must be durationally significant, and not merely a hiccup in revenues or earnings over a quarter or two. But the economic dislocation caused by COVID-19 is so fresh and unfamiliar that reliable forecasts of long-term implications are largely impossible. (The historic and careening volatility in the financial markets of late ably attests to this fact.) And thus, as of this writing at least, most buyers are likely to find themselves unable to scare up the evidence needed to carry their burden of proving a durationally significant adverse effect in the post-COVID world.

- Precedential Tea Leaves. Finally, as we noted in our prior post, the time span of our original data set also coincided with an era in which no Delaware opinion had ever found an MAE to have been triggered. Like many other hot streaks, however, this one eventually came to an end in the fall of 2018, with the Chancery Court’s Akorn v. Fresenius opinion. The precedent has no doubt bolstered the confidence of rueful buyers in pending deals who are now contemplating invoking their MAEs. (And we note in passing that the MAE in Akorn specifically carved out pandemics, subjecting the exclusion to a “disproportionate effects” carve-in.) Nevertheless, it is important to understand that while Akorn no doubt sent a message that the “MAC is Back” as a front-line issue for M&A doctrine, the underlying facts of the case diverge considerably from current circumstances (involving highly target-specific issues pertaining to regulatory clearance and outright regulatory fraud).

In the light of above points, we conjecture that the average buyer will face a heavy slog in asserting that COVID-19 represents a deal-killing force majeure, even when the MAE contains no carve outs for pandemics (general or specific). The odds grow longer still, of course, in the presence of such carve-outs.

So this must imply that savvy acquirors need to abandon all plans to declare an MAE, right? Not so fast: notwithstanding the uphill battle (and long odds) faced by buyers asserting MAEs, we can think of several reasons why rational and sophisticated parties might still pursue this strategy:

- First, pressing the MAE issue can buy precious time for the acquiror. Although MAE litigation moves substantially faster in Delaware Chancery Court than does commercial litigation in other venues, the process is still far from instantaneous. Moreover, the temporary closure of courthouses in Delaware and potential delays in litigation schedules due to the outbreak may well lead to unusually protracted timelines. That, in turn, could afford buyers an opportunity to amass additional evidence about the durational significance of the COVID-19 crisis (while preserving the option to abandon the strategy down the road).

- Second, even if the current saga proves to be short-lived, it is already raising fears of a medium-term liquidity crunch. The potential delaying effect of an MAE kerfuffle can also be a hidden source of liquidity for cash buyers, at least until the current market tumult resolves and a greater sense of order returns to capital markets.

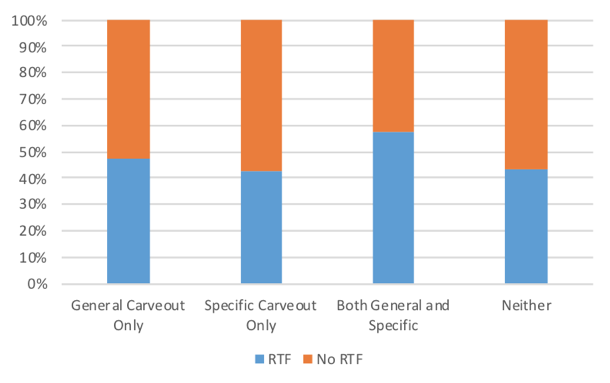

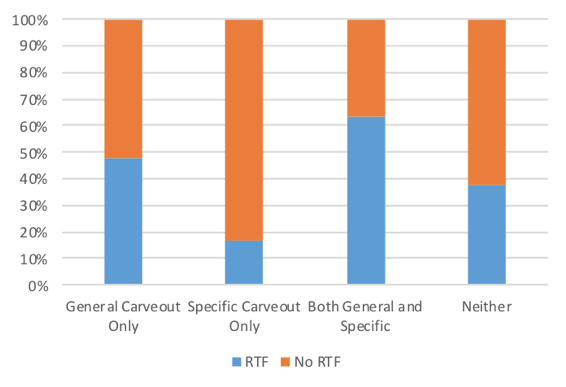

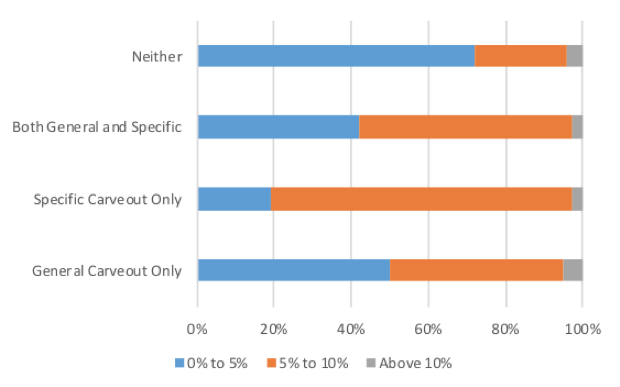

- Finally, invoking the MAE may be part of a larger portfolio of strategies that buyers might deploy in attempting to walk from − or potentially restructure − a signed deal. Several other strategies suggest themselves too, including asserting the failure of other closing conditions (related to, inter alia, financing, regulatory clearance, solvency, and tax status). Moreover, in many deals acquirors could conceivably threaten a backup strategy of using a “reverse termination fee” (“RTF”) to permit them to exit a deal in exchange for paying what amounts to liquidated damages to break away. The figures below plot the prevalence of reverse termination fees as a function of each type of MAE carve-out, concentrating on both all deals in our data set (left panel) and pending deals (right panel). As illustrated in the figures, RTFs appear to be most common in deals where there are both general and specific carve-outs − i.e., those deals that would (all else held constant) be least amenable to granting force majeure walking rights. Moreover, the deals that have neither general nor specific carve-outs for pandemic risks tend on the whole to be less likely to offer RTFs to compensate.

|

|

| A. Prevalence of RTFs by Carve-Out Type (2003-Pres) | B. Prevalence of RTFs by Carve-Out Type (Pending Deals; 3/2020) |

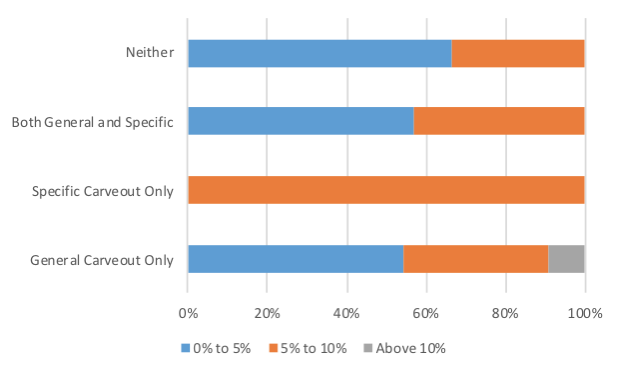

For the deals that include RTFs, one can drill further to assess the relative size of the RTF (as a percentage of the transaction value) by carve-out type. As the figures below demonstrate, RTFs tend to be the lowest when there is neither a general nor a specific carve out. Recall that this same group as a whole was relatively less likely to have an RTF to begin with. On the whole, then, RTFs and MAEs tend to operate as weak substitutes for one another; but there is still ample room for many buyers to use them together as part of a multi-pronged approach to busting up a deal (or, more likely, to get it restructured).

|

|

| A. Size of RTF by Carve-Out Type (2003-Pres.) | B. Size of RTF by Carve-Out Type (Pending Deals, 3/2020) |

We close by reminding readers that notwithstanding the seductive allure of hard statistics to describe MAE provisions, this area of law remains − much like force majeure terms themselves − relatively opaque and open to competing arguments. We doubt that this core feature (or is it a bug?) will resolve itself any time soon. Unless and until that happens, practitioners and observers should continue to pay close attention not only to the internal coherence of their own MAEs, but also to how they compare with the overall landscape of rapidly mutating contractual practices.

This post comes to us from professors Matthew Jennejohn at Brigham Young University Law School, Julian Nyarko at Stanford Law School, and Eric Talley at Columbia Law School.